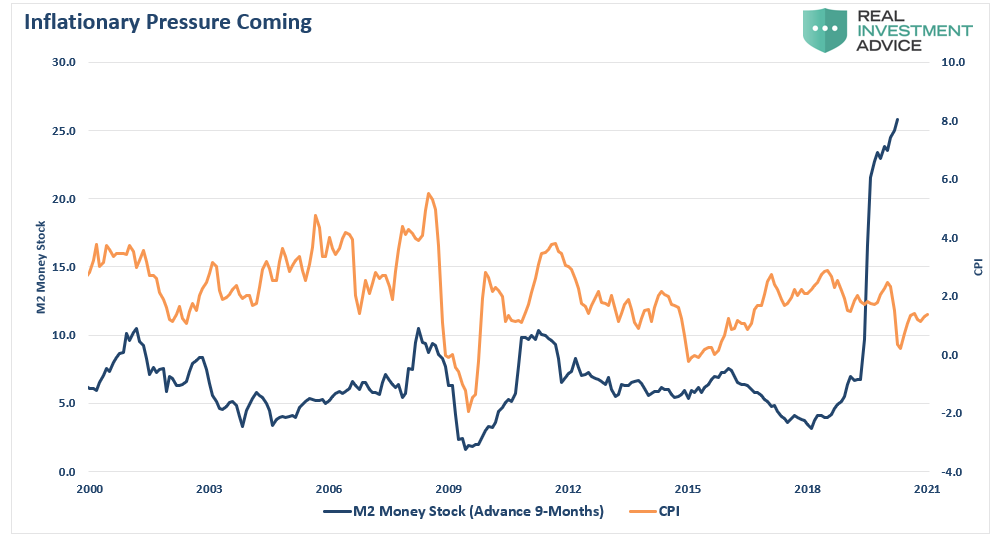

The measure of money in the system, known as M2, is skyrocketing…with the Biden administration adding another $1.9 trillion into the economy…Should we worry about a hyperinflationary surge like we saw in the late 70s or, are the deflationary pressures on the economy still present?

…The Difference Between An Inflationary Increase and Hyperinflation

Could repeated stimulus into the economy that exceeds the current output gap lead to a rise in inflationary pressures? Absolutely, but hyperinflation is not a threat – at least not yet. Why? Because hyperinflation comes from a complete loss of faith in a currency from the threat of losing a war (e.g. Weimer Republic), an economic collapse, or some other catastrophic event. The U.S., even with all of our economic ills and woes, is still the safest place, in terms of liquidity, depth, and strength, to store excess reserves. The near historic low yield on government treasuries tells the story here.

What is important, is whether or not inflationary pressures, regardless of where they come from, have reached levels that could impact economic growth. While we see commodity-based inflation, primarily in food and energy, is that alone enough to offset the deflationary pressures we see economically from wages, debts, deficits, and rising dependency on social welfare?

Inflation is a function of three primary components:

- The velocity of money,

- Wages, and

- Commodity prices.

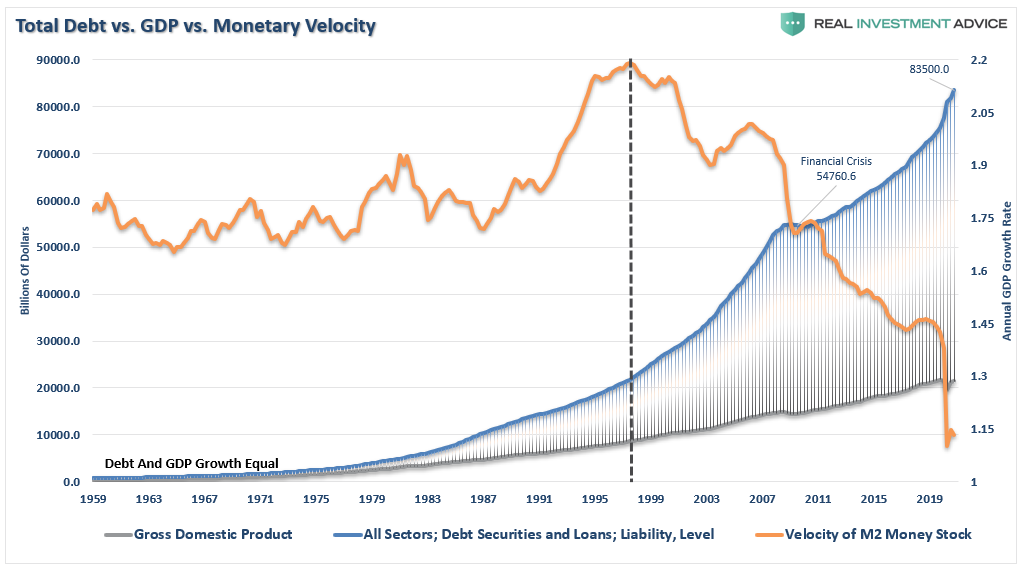

1. The Velocity of Money

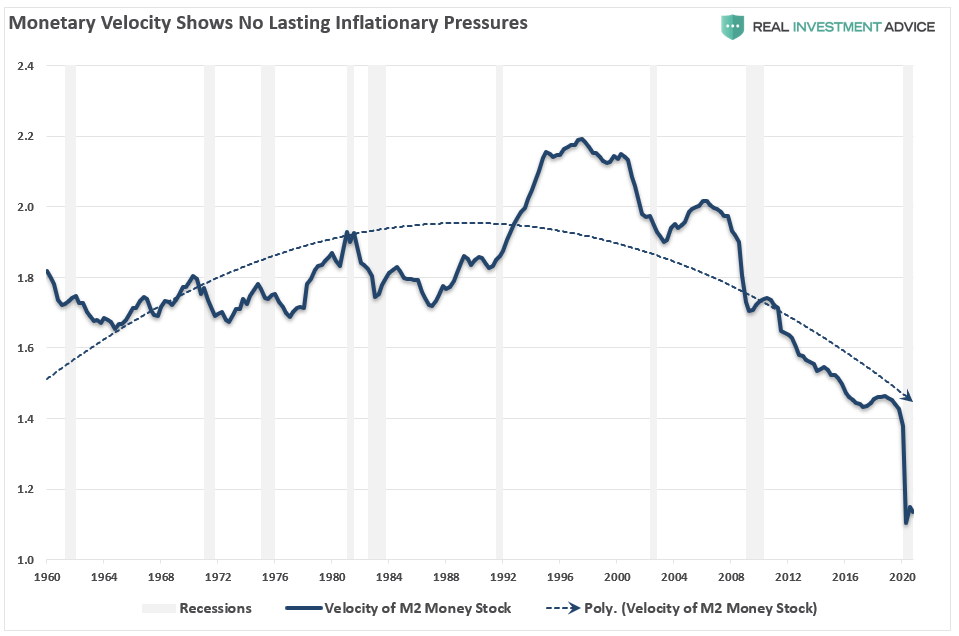

…Monetary velocity is defined as the rate at which money in circulation is used for purchasing goods and services. Velocity is useful in gauging the health and vitality of the economy.

- High money velocity is usually associated with a healthy, expanding economy.

- Low money velocity is usually associated with recessions and contractions and the chart above shows what we have known for quite some time: money is not flowing through the system.

Monetary velocity…is a simplistic representation of demand. For prices across the entire spectrum to rise, there has to be more demand than supply. If the velocity of money is increasing, then “demand” in the system is growing. That increase in demand allows producers to raise prices and pass on costs to consumers but, currently, companies are absorbing those costs, which eats into profit margins. To offset that increase, we have seen companies continuing to scale back employment, increase automation, and reduce CapEx. The decline in “activity” has worsened post-pandemic.

2. Wage Inflation

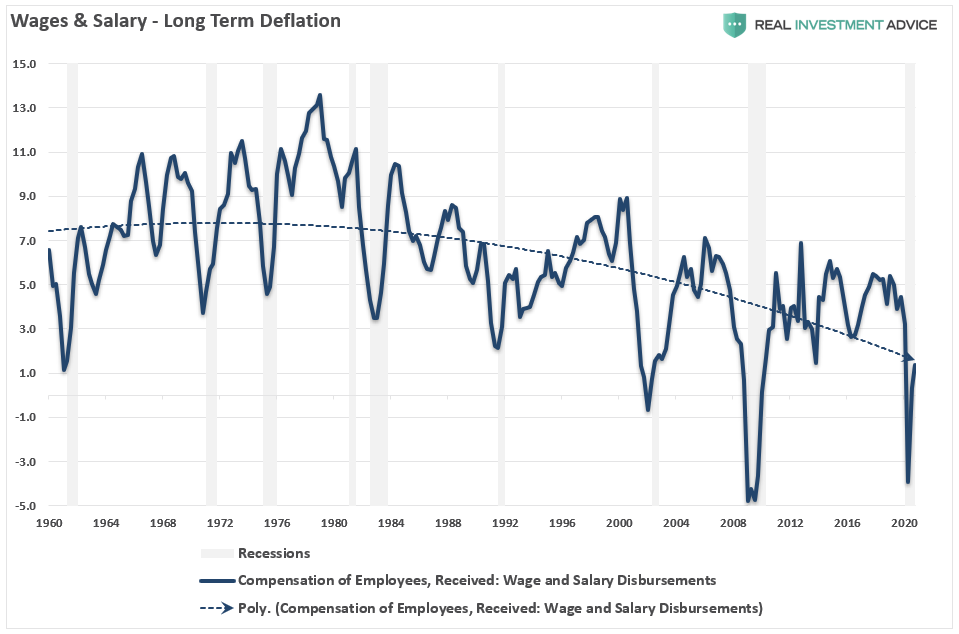

Secondly, to have “sustainable” levels of inflation, wages must be increasing.

As wages rise, individuals can consume more, increasing aggregate demand, which, as noted above, leads to higher prices. Unfortunately, wage and salary disbursements, on a year over year basis, have been on the decline since 1980. Such remains commensurate with the weaker economic growth and declining monetary velocity.

As wages rise, individuals can consume more, increasing aggregate demand, which, as noted above, leads to higher prices. Unfortunately, wage and salary disbursements, on a year over year basis, have been on the decline since 1980. Such remains commensurate with the weaker economic growth and declining monetary velocity. While wages have turned up post the recessionary lows, they are still sharply lower than at the turn of the century. That deterioration in wages, combined with credit constraints, has continued to put pressure on producers’ ability to raise prices. As a consequence, we continue to see more reliance on discounting to move inventories.

While wages have turned up post the recessionary lows, they are still sharply lower than at the turn of the century. That deterioration in wages, combined with credit constraints, has continued to put pressure on producers’ ability to raise prices. As a consequence, we continue to see more reliance on discounting to move inventories.

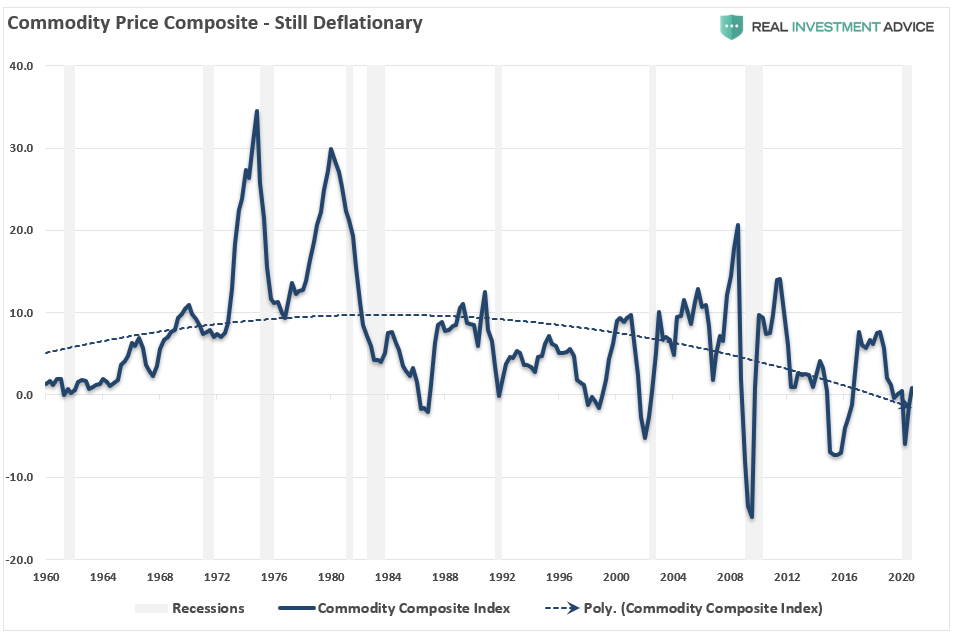

3. Commodity Prices

…Commodity prices are essential in consideration of inflation due to the effect on personal incomes. Since consumption is roughly 70% of the economic calculation, higher commodity prices, particularly food and energy costs, can have a “psychological” impact on consumers. Such is especially an issue if it occurs quickly. Consumers can adjust to higher prices over time as long as wages rise at a proportional rate; however, that is not the case currently…

…Commodity prices are essential in consideration of inflation due to the effect on personal incomes. Since consumption is roughly 70% of the economic calculation, higher commodity prices, particularly food and energy costs, can have a “psychological” impact on consumers. Such is especially an issue if it occurs quickly. Consumers can adjust to higher prices over time as long as wages rise at a proportional rate; however, that is not the case currently…

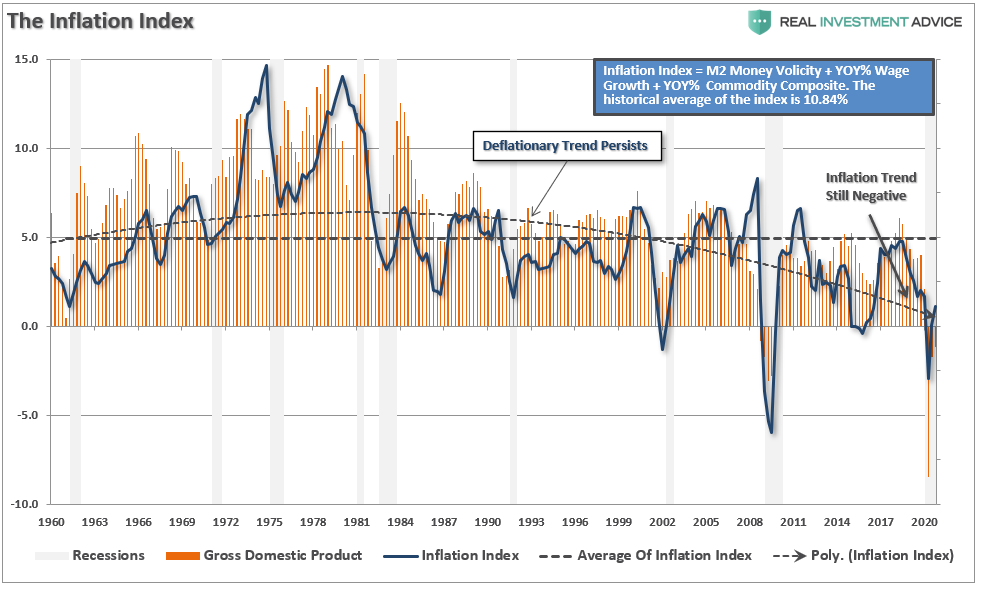

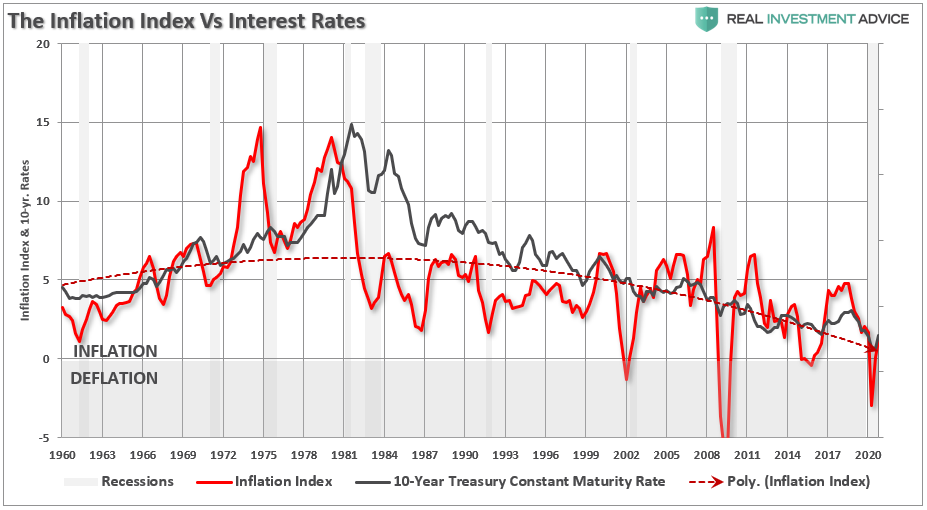

The High-Inflation Index

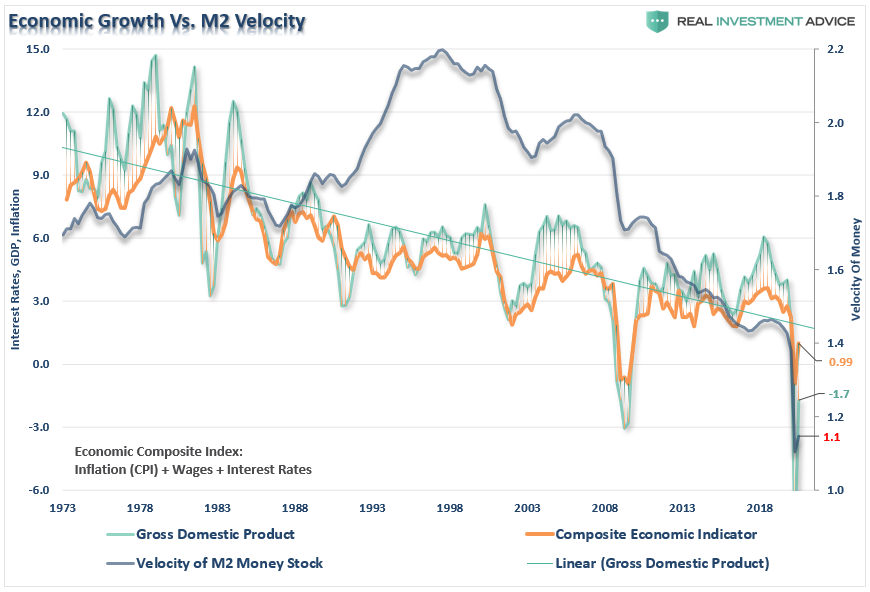

None of the above items, individually or collectively, point to hyper-inflation. However, to measure these components’ impact on the overall economy, I created a composite index of wages, commodity prices, and velocity. The index clearly shows the inflationary pressures of the late ’70s, which gives us a confidence level in the assumptions’ validity. The dashed line is the average level of the index since 1959.

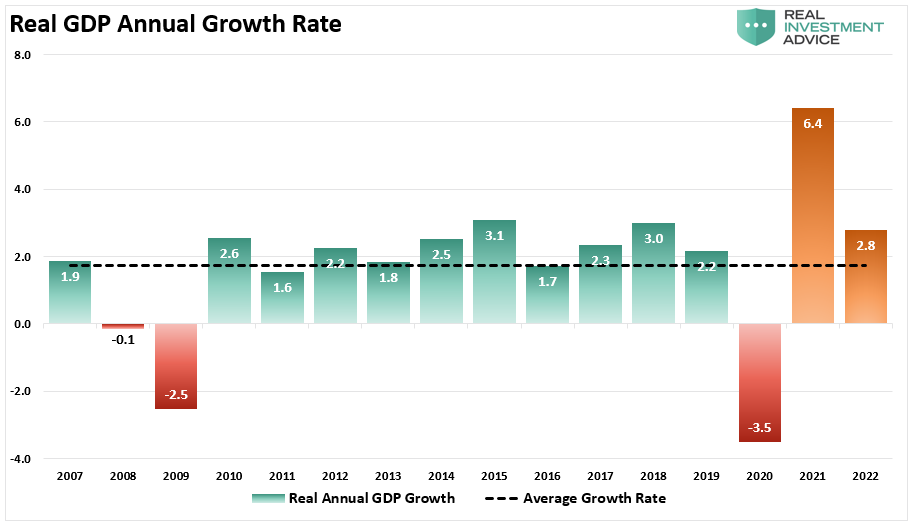

…When the index has risen above its average level, the economy has begun to weaken or receded into recession. Currently, the inflation index is at 1.12, which well below the long-term average of 4.94. The reading suggests what we already know, that since 2007, the average economic growth rate has been feeble at just 1.3%, or 1.7%, if we use estimates for 2021.

Secondly, while inflationary pressures are indeed rising short-term, we tend to agree with Jerome Powell’s assessment they could be “transient.” There are three reasons for that statement:

- Current inflationary pressures are a function of the stimulus flooding into the system, which is “transient.”

- The economy is dependent on zero interest rates and $120 billion in monthly bond purchases, which suggests there is little if any, organic economic growth; and,

- The enormous burden of debt continuing to depress economic growth, and notably, monetary velocity.

Conclusion

The threat of hyperinflation remains an outlier due to the economic detractors mounting over the last 40-years, namely:

- A decline in organic savings that depletes productive investments

- An aging demographic that is top-heavy and drawing on social benefits at an advancing rate.

- A heavily indebted economy with debt/GDP ratios above 100%.

- The decline in exports continues due to a weak global economic environment.

- Slowing domestic economic growth rates.

- An underemployed younger demographic.

- An inelastic supply-demand curve

- Weak industrial production

- Dependence on productivity increases to offset reduced employment

While the U.S. economy certainly has its share of problems, the U.S. is still the “cleanest shirt in a pile of filthy laundry.”

- With the Treasury still the safest source to store foreign currency reserves, at the moment, the likelihood of a complete economic meltdown is minimal.

- Furthermore, due to the deflationary pressures that currently exist due to weak wage growth, automation, and mounting debts, it is unlikely that inflation can rise much before it triggers an economic contraction. Since interest rates adjust for inflation, a rise in inflationary pressures is a “double whammy” on consumption…

Editor’s Note: The original article by Lance Roberts, has been edited ([ ]) and abridged (…) above for the sake of clarity and brevity to ensure a fast and easy read. The authors’ views and conclusions are unaltered and no personal comments have been included to maintain the integrity of the original article. Furthermore, the views, conclusions and any recommendations offered in this article are not to be construed as an endorsement of such by the editor. Also note that this complete paragraph must be included in any re-posting to avoid copyright infringement.

Related Articles from the munKNEE Vault:

1. Hyperinflation Isn’t In the Cards – Here’s Why

There are two specific reasons why runaway inflation did not happen a decade ago, and why it won’t likely happen now, either:

2. Hyperinflation Insights: What You Need To Know! (+6K Views)

To wind up with true hyperinflation, some very bad things have to happen. The government has to completely lose control and the populace has to completely lose faith in the system – or both at the same time. Will the U.S. go down that path? Let’s review the situation.

3. What Would It Take For Hyperinflation To Occur in the U.S.? (+28K Views)

There is a difference between inflation and hyperinflation…and there is no gradual path from one to the other. To wind up with true hyperinflation, some very bad things have to happen. The government has to completely lose control… the populace has to completely lose faith in the system… or both at the same time. [Are we there yet? Let’s take a look.]

4. The Road to Eventual Hyperinflation & Financial/Political Collapse

What I outline below is not a forecast but a potential scenario which I sincerely hope won’t come to pass but the risk of going down the road to political and financial system collapse, social unrest and even civil war, and eventual hyperinflation, is certainly there.

5. Will Hyperinflation Occur As Result Of Gov’t Response To COVID-19 Plague?

The longer the economy stays shutdown, the more money we will print; increasing the risk of hyperinflation so we are starting to…

6. Hyperinflation Highly Unlikely In U.S. & U.K. – Here’s Why (+4K Views)

Without pricing power or a large fiscal deficit and large foreign currency demands, it simply isn’t credible to claim that hyperinflation in the U.S. or the U.K. is in the offing now or anytime in the immediate future.

7. Current Excessive Money Printing Will Lead To Hyperinflation – Got Gold?

Hyper-inflation will spread from country to country just as the coronavirus has starting most likely in the U.S. and within the EU quickly be followed by Japan and most other developing countries. Got gold?

8. 28 Countries Have Experienced Hyperinflation In the Last 25 Years (+118K Views)

Hyperinflation is not an unusual phenomenon. 33 countries have experienced hyperinflation over the last 100 years of which no less than 22 have experienced it in the past 25 years and 4 in the past 10 years. The United States is one of the few countries to have experienced two currency collapses during its history (1812-1814 and 1861-1865). Could it happen again?

9. Hyperinflation Is Coming To The U.S. But…(+3K Views)

I think that the U.S. has a roughly 0% probability of experiencing hyperinflation within the next 2 years. I also think, however, that the U.S. has a 100% probability of eventually experiencing hyperinflation. Below I explain why I think that is the case.

I have been reading a lot lately about the coming hyperinflation in America… [and while] I respect many of the writers [who express that opinion] I think they are jumping the gun. At this point none of the economic or political factors required to set off hyperinflation are present – and a careful analysis of theory, fact, and history leads me to conclude that inflation/stagflation is our future. It is quite a leap of fancy to say we are certain to have hyperinflation. Words: 2780

A Few Last Words:

- Click the “Like” button at the top of the page if you found this article a worthwhile read as this will help us provide more articles of interest to you.

- Comment below to share your opinion or perspective with other readers and possibly exchange views with them.

- Register to receive our free Market Intelligence Report newsletter (sample here) in the top right hand corner of this page.

- Join us on Facebook to be automatically advised of the latest articles posted and to comment on any of them.

munKNEE should be in everybody’s inbox and MONEY in everybody’s wallet!

Sudden inflation happens occasionally and it’s scary…panicky when it does, but the gradual inflation that comes over decades is just as scary, but never appears as an enemy on people’s radar. Today we don’t raise an eyebrow for paying ten times more for a McDonald’s burger than we did in the 1950s whether our income has

risen tenfold or not. We can be assured that in 2090 McDonald’s diners will be paying multiples of the present price for a burger, but all the factors mentioned in this article may preclude income rising to keep pace with inflation over the next seventy years. Maybe we’d better invest heavily in pharmaceutical grade pot.