…While most people understand that their credit score is the key to getting approved for a loan, not all realize that having a high credit score also improves their finances…because…it can save you money. The higher your credit score, the lower the interest rate you will qualify for, thus saving you money over the life of your loans…This post guides you through your credit score, from everything that determines it, what helps and hurts a score, what leads to bad credit, how to check your score, and most importantly, how to improve your credit score fast.

realize that having a high credit score also improves their finances…because…it can save you money. The higher your credit score, the lower the interest rate you will qualify for, thus saving you money over the life of your loans…This post guides you through your credit score, from everything that determines it, what helps and hurts a score, what leads to bad credit, how to check your score, and most importantly, how to improve your credit score fast.

The original article has been edited here for length (…) and clarity ([ ]) by munKNEE.com – A Site For Sore Eyes & Inquisitive Minds – to provide a fast & easy read.

Why Your Credit Score Is Important

Your credit score is vital in helping you get approved for a loan. This allows you to buy a house, a car or even get approved for a credit card but your credit score goes beyond just helping you with borrowing money.

In many cases, your auto insurer takes into account your credit score. Why? Through their number crunching, they have determined that credit scores and driving habits are related. They have found that the highest credit scores are associated with more responsible drivers. The more responsible the drive, the less likely they are to get into an accident. This relationship is a sliding scale. This means if you have a high credit score, you will tend to get less expensive auto insurance rates. If you have bad credit, then you will have a more expensive insurance rate.

Your credit score even comes into play in landing a job! As with auto insurers, employers have done their own number crunching. They have found a relationship between good employees and a high credit score as well.

As you can see, making sure you have the highest credit score is vital not only to getting approved for a loan, but also with saving you money on insurance and even in landing a job.

What Makes Up Your Credit Score

Now that we know how important a credit score is, let’s begin to dive into the details so we can fully understand what makes up your score.

When talking about a credit score, the possible scores you can have range from 300 to 850 when talking about a FICO Score. The higher your credit score falls in this range, the better…

There are 5 areas that make up your credit score:

- Account Mix: the greater the mix of credit you have, the better so having an auto loan, a credit card and student loans is good.

- Credit Inquiries: this is how many times you have recently applied for new credit. When you apply for too many new credit accounts in a short period of time, you raise your credit risk and potentially lower your score.

- Payment History: this shows how often you pay on time and how frequently you pay late. If you pay late, expect it to have a negative impact on your credit score.

- Credit Utilization: this is a ratio between the amount of credit you have available and how much debt you have. The higher the amount of debt you have, the lower your score.

- Age of Credit: creditors look at how old your credit is because the longer the history, the more comfortable they are in extending you credit as you have a track record.

Each of these categories accounts for a different percent of your score. The people over at Credit Sesame have kindly provided this infographic for you to see just how much weight each of these categories holds in making up your credit score.

Monitoring Your Credit Report

…Your credit report contains a lot of personal information about you, where you have lived, the types of credit you have had, any bankruptcies you may have declared and more. There are 3 main credit reporting companies out there, TransUnion, Equifax and Experian. Each reporting agency maintains your credit report and credit score rating. As a result of this, credit reports and credit scores can vary between agencies because creditors and utilities may report your credit history to one agency or all agencies. For example, your electric company may only report your payment history to Transunion so if you are late with your electric payments, your credit score with Transunion could be lower than your score with Experian.

Because your credit score is derived from a combination of information on your credit report, it is important that you check your credit report at all three agencies yearly. You can do this for free through AnnualCreditReport.com. Additionally, I show you how I get my report for free 3 times a year here. If you haven’t done so lately, it is important to check your report with all of the hacking going on and stealing of identities.

Checking Your Credit Score

How exactly do you check your credit score? Back in the day, it was difficult to do. You had to reach out to the credit reporting agencies and pay them to get your score. Typically you were looking at $30 every time you did this. Luckily technology and the government have changed things. Now you can get your credit score for free from various sources. One nice place to get your score is your credit card company. Discover offers a free score with their credit card and many other credit card issuers are jumping on board as well. You can also get a free credit score from third party companies. Credit Sesame is a great option for this. What is nice about many of these is that while your score is free, you can sign up for credit monitoring as well.

There is no requirement to sign up for the credit monitoring. You can just get your score for free but note, however, that if you try to get your credit score for free from one of the credit reporting agencies, they require you to sign up for their monthly monitoring service in exchange for getting your credit score for free so the bottom line is this:

- If you go with one of the credit reporting agencies, pay for your score so you aren’t duped into paying for monthly monitoring.

- If you want your credit score for free whenever you want, get it from Credit Sesame.

You can also get your score for free after applying for credit. Lenders are now required to send you your credit score after you apply for a loan. While nice, it doesn’t help you in the sense that you don’t know what your score is until after you have already applied for credit.

Lastly, pay attention whenever you see an offer for a free credit score that asks you for your credit card. In most cases, these are scams that are offering you a free 30 days and then will start billing you each month. The government has started to crack down on these offers but they are still out there, so pay attention when looking for ways to get your credit score for free. Again, I can’t stress this enough, to be safe, just get your free score from Credit Sesame and be done with it.

Things That Hurt Your Credit Score And Lead To Bad Credit

- …Opening up credit accounts so that you can achieve a higher score: Don’t do this. Even though a good variety of credit is ideal, opening too many accounts hurts your score so opening a bunch of accounts will do more harm than good…

- Having too much debt: When you have a lot of debt, you become risky to creditors because it is easier and more likely that you will start missing payments. Be sure to take the steps necessary to live within your means.

- Making late payments: when you start to miss payments, creditors get nervous about lending you more money. They lend you money because they expect to get it back and hope to earn some interest.

- You stop paying back your debt: When that happens they stop offering you credit as your history has shown you won’t pay your debt. Thus your good credit becomes bad credit.

In some cases, they may keep offering you credit with the caveat of a sky high interest rate. You can keep borrowing money, but they are making a mountain of money off you and you are destroying your finances.

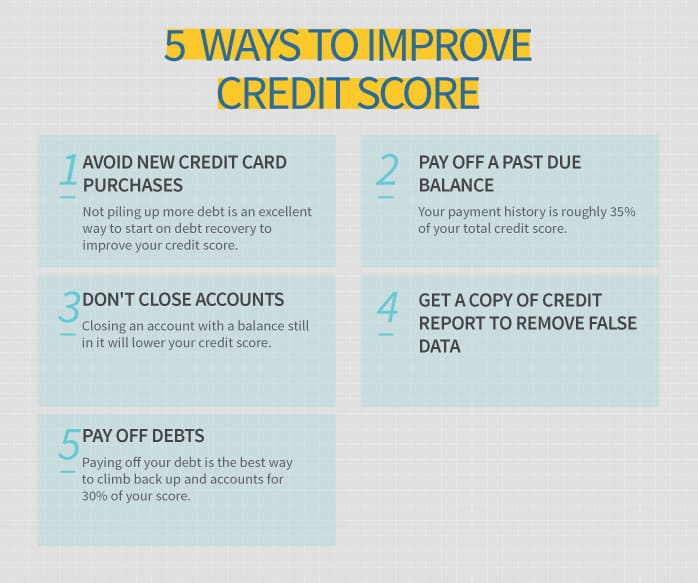

Improving Your Credit Score Quickly

Now that you see what hurts your credit score, we can see how we can improve our credit score quickly.

The easiest ways to improve your score are within your control.

- Keep new accounts to a minimum.

- Pay on time.

- Don’t carry too much debt – but how much debt is too much?

It is easy to calculate your debt to credit ratio yourself, there is only 1 trick you have to be aware of. Here are your steps:

- Get all of your loans and credit card statements together

- Create 2 piles: one for revolving credit (credit cards) and one for installment loans (auto loan, mortgage, student loans, etc)

- With the revolving credit pile (credit cards), add up your current balances and divide by your credit line

- With the installment loan pile (all other debts), add up your current balances and divide by the original loan amount

With regards to your credit card debt, you want this ratio to be low. For example, after analyzing the people with the highest credit score, their debt to credit ratio on revolving accounts averaged 7%.

Let’s look at a quick example so you can be sure you are doing this step correctly.

- Let’s say you have 2 credit cards, with balances of $500 and $2,500. The credit limits on the cards are $5,000 and $4,000. If you add up your debt ($500 + $2,500) and divide by your credit limit ($5,000 + $4,000) you have a debt to credit ratio of 33% ($3,000 / $9,000). Work to get and keep this number under 10%.

- An easy way to lower your debt to credit ratio quickly is to pay off your credit cards strategically. Which ones are closest to being maxed out? Focus on paying these down quickly so you can improve your score.

- Additionally, if you have a card with a very small balance that you can pay off in a month or two, pay it off quickly to get a small boost in your score.

- As a last resort, you could reach out to the credit card companies and ask them to raise your credit line. Doing this will automatically improve your debt to credit ratio but you have to make sure this higher limit doesn’t tempt you to start spending more.

- When it comes to installment loans, those with the highest credit score had a credit ratio of 65% on installment loans so, after following the steps above, you can see how much your debt to credit ratio is on installment loans and how you compare.

To recap on how to improve your credit score fast:

- Make all your rent, mortgage, credit cards, loans and utility payments on time. Paying all your bills by the due date over time strengthens your credit report and leads to a higher credit score.

- Monitor your credit card balances carefully. Keeping your credit balance to 10% or less of your available credit limit for revolving accounts and 65% or less for installment accounts helps to ensure good credit worthiness. Allowing balances to creep over this limit lowers credit scores. You can easily keep your credit card balances low and thus keep your credit score high by using the free service Debitize.

- Refrain from applying for new credit too often in a six-month period. Opening up too many accounts in a short amount of time signals you might go on a spending spree and won’t have the income to pay back the debt you incur.

- Lastly, if you are turned down after applying for a loan or credit card, it may have a negative impact on your credit score. Luckily, you are allowed by law to request the reason why you were turned down. This can help you to improve your credit score for the future.

Final Thoughts

Overall, it is important to monitor your credit report and your credit score.

- By reviewing your credit report, you can spot and fraud or identity theft issues before they become a major headache for you.

- Making sure you have a high credit score is important, too, so that when you do take out a loan you can get the lowest interest rate possible, which saves you money both now in terms of the monthly payment and over the long term in regards to interest.

Take your credit seriously and you will ensure you end up with a higher credit score than you have now and, if your credit score is lower than where you want it to be, follow the tips I outlined so you can improve your credit score quickly.

Related Article From the munKNEE Vault:

1. 3 Tricks to Repair Your Credit (FICO) Score

Anyone who has bad credit will want to find some tips to improve credit score problems so they can get approved for loans, get good insurance rates. This article provides some simple but effective tips that can help you repair your credit yourself. Words: 442

For all the latest – and best – financial articles sign up (in the top right corner) for your free bi-weekly Market Intelligence Report newsletter (see sample here) or visit our Facebook page.