A financial tsunami is…scheduled to hit the U.S. economy and taxpayers over the next several years  and being fully aware of what will be happening…should be one of the foundations of any retirement or financial planning process. Hopefully, this analysis proves helpful for you in that regard.

and being fully aware of what will be happening…should be one of the foundations of any retirement or financial planning process. Hopefully, this analysis proves helpful for you in that regard.

The comments above and below are excerpts from an article by Daniel Amerman (DanielAmerman.com) which may have been edited ([ ]) and abridged (…) to provide a faster & easier read.

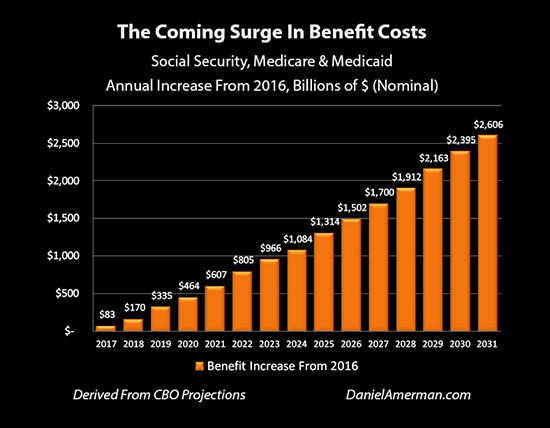

The Coming Surge In Benefit Costs

Paying for Social Security and Medicare benefits is about to get much, much more expensive….[as] the costs soar each and every year in comparison to the year before, as shown in the graph below.

This is not a dire forecast or disaster scenario, but rather something that has been widely anticipated and talked about for decades. What is different today is that we are no longer talking about the distant future – but the near future. The long expected storm is finally upon us….

Future Benefit Costs vs the Proposed Trillion Dollar Infrastructure Stimulus Program

To add some perspective, let’s compare this to the massive, trillion dollar infrastructure stimulus program that is currently being proposed.

- The proposed program is vast, with the idea being to rebuild roads, bridges and airports across the entire nation over ten years, pumping $100 billion a year into the economy in an attempt to stimulate growth.

- The stimulus program is so expensive that it may never get past Congress, at least not in whole yet, as demonstrated below, the increases in costs associated with the trillion dollar stimulus are effectively trivial in comparison to the increases in the scheduled costs of paying retirees their promised benefits.

- Indeed, with benefit spending alone reaching an annual rate of almost $10 trillion a year, the almost $900 billion in increased costs would pay for nine nationwide infrastructure programs simultaneously ($100 billion per year for nine programs, compared to 2016 spending).

Rapid Increase In Social Security and Medicare Benefit Spending

…The speed with which Social Security and Medicare benefit spending will come to dominate overall government spending to an unprecedented degree can be seen in the graph below.

[Before reading further check out this site]

Adjusting For Inflation For A Clearer Picture

Even using the historically quite low rates of inflation projected by the CBO, much of the increases in benefit payments in the 2030s and 2040s are there because of a lower purchasing power of the dollar. When we adjust for inflation, the dollar amounts fall somewhat – but the costs are still extraordinary.

When we look at the situation graphically – we can see a miracle of sorts. All other government spending stays flat in inflation-adjusted terms. With the exception of benefits, the government stops growing for about ten years, and is even shrinking as a percentage of the economy. Other government spending is shown as falling from 9.2% of GDP in 2016 down to 7.7% by 2026 – and the reason for this “miracle” of a shrinking government (relative to GDP) within the CBO projections is that it has to be assumed because, if a way is not found to slash all other types of government spending, then there is no possible way to meet the soaring benefit costs without creating an even more impossible financial situation for the government…

When we adjust for inflation over 30 years, then the yellow line shows us a ceaseless progression, where the real cost of paying Social Security, Medicare and Medicaid benefits leaps every single year, without ever slowing down.

We’ve never seen this before, not on this scale. Our government has never done this, the economy has never handled this, taxpayers and bond markets have never seen it either – but it’s here – and will be growing fast – and soon.

What Wasn’t Expected

Again – that this day was coming, and that it would be very financially challenging, has been known for decades. However, what was not foreseen in the long-term models was the slowdown in economic growth that would occur in the aftermath of the financial crisis of 2008 which means the current economy is smaller than what had been expected – and tax collections are smaller than expected – so less money available means it is going to be still harder to afford what was already expected to be almost unaffordable.

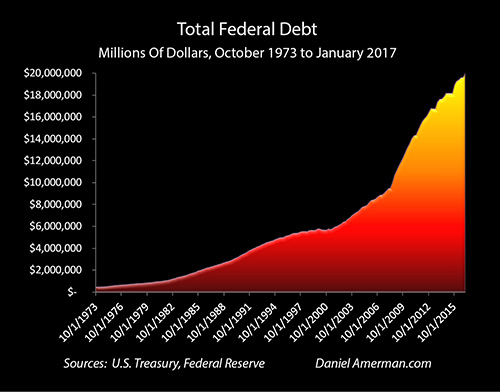

Also of great importance is that while the national debt was expected to rise, it was expected to happen in the process of paying for benefit promises. The debt was not supposed to double before the most expensive part of paying Boomer retirement promises even really got going but that is exactly what happened, as shown below.

The national debt doubled in the aftermath of 2008, and is now over 100% of GDP…

Future Interest Payments to Soar

The coming rapid increases in required benefit payments are not at all compatible with efforts to reduce debts, but lead to something quite the reverse. When we start with a debt that has already doubled, and then stack endlessly increasing benefit costs on top of that, we get something that is much worse than either by itself. Even current government projections (including some quite optimistic assumptions) are that the national debt will soar far past current levels, as money is borrowed:

- to make benefit payments that would otherwise be unaffordable

- and sets off a massive increase in interest expenses…

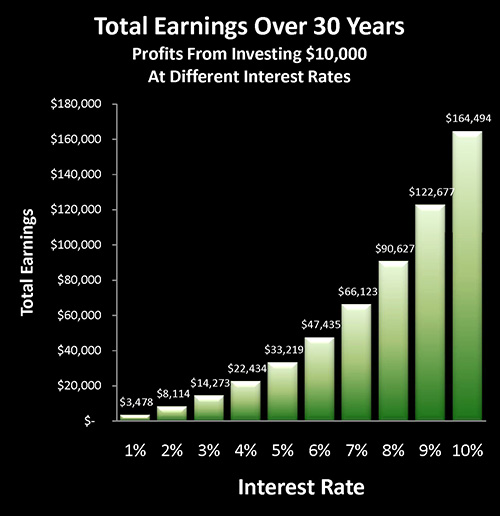

Generally speaking, if the debt is soaring, then interest payments on that debt are soaring and we then have two rapidly growing governmental expense categories, each of which are consuming ever more cash while pushing annual deficits – and future interest expenses – still higher and this creates an acute conflict of interest between governments and savers.

Savers need higher rates to build wealth, as shown above, but governments need very low interest rates to keep interest payments on the national debt at manageable levels. When rising benefit costs further increase that debt load – and the potential extreme expense of higher interest rates – this situation may force still lower interest rates for savers, and still lower investment earnings that could last for decades into the future.

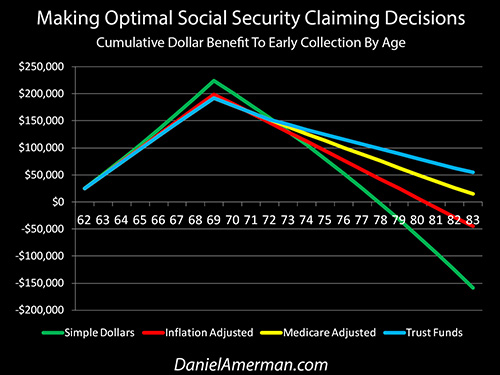

Will Future Social Security Benefit Payments Get Paid Out?

There are also major implications when it comes to the widespread advice that the best financial choice is to delay claiming Social Security benefits for as long as possible in order to increase the size of the eventual payments. The assumption is that we can absolutely rely on our benefits being paid in full and exactly on schedule yet, in looking at those decades of so many trillions of dollars of rapidly rising expenses, I think that it probably crossed most people’s minds that maybe, just maybe those benefits might not all get paid.

Indeed, as shown above… even if we take the very “gentle” approach of assuming that the government doesn’t change the law – but does take full advantage of the ability to lower benefits in accordance with current law – then all of our decisions could change. The best choice may be to claim as soon as possible rather than as late as possible.

Accepting Reality

This analysis is not intended to be gloomy or pessimistic, but rather to simply present the numbers as they are. Reality just is what it is, and the reality is that the big changes are finally here – and they will be accelerating in the near future. There will be no wishing it away. Refusing to think about it will not be particularly helpful either….Pretending this isn’t happening is a luxury that only works when the changes are in the distant future. What the numbers herein quite plainly show is that we will be rapidly losing that luxury over the coming years, and plans that do not take a new and dominant reality into account – may not perform as desired.

Let me suggest that being fully aware of what will be happening in the next several years – and also over the next ten years and beyond – should be one of the foundations of any retirement or financial planning process. Hopefully, this analysis has been helpful for you in that regard.

Disclosure: The above article has been edited ([ ]) and abridged (…) by the editorial team at  munKNEE.com (Your Key to Making Money!) to provide a fast and easy read.

munKNEE.com (Your Key to Making Money!) to provide a fast and easy read.

“Follow the munKNEE” on Facebook, on Twitter or via our FREE bi-weekly Market Intelligence Report newsletter (see sample here , sign up in top right hand corner)