The benefits of being able to detect a bubble, when you are in its midst, rather than after it bursts, is that you  may be able to protect yourself from its consequences. [Below are possible] mechanisms to detect bubbles, how well they work and what to do when you think a particular asset is in one.

may be able to protect yourself from its consequences. [Below are possible] mechanisms to detect bubbles, how well they work and what to do when you think a particular asset is in one.

Click on Facebook for latest articles on gold/silver & economic/financial matters from munKNEE.com

Click on Twitter for latest tweets from munKNEE.com

Subscribe to the FREE Market Intelligence Report newsletter (sample here)

Dasmodaran goes on to say in further edited excerpts:

If you believe that the stock market is in a bubble, you have lots of company. You have long-time market watchers, the New York Times and even a Nobel Prize winner in your camp. [That being said:]

- What is a bubble, exactly?

- How can you tell if you are in one?

- If you do believe you are in a bubble, what is your best course of action?

Not only are these questions difficult to answer, but the answers can vary across markets, investors and time.

The Bubble Machine

Every market has a bubble machine, though it is less active in some periods than others, and that machine creates an ecosystem of metrics and experts, as well as warnings about bubbles about to burst, corrections to come and actions to take to protect yourself against the consequences.

In periods like the current one, when the bubble machine is in over drive and you are confronted by “bubblers” with varying credibility, motives and methods, you may find it useful to first categorize them into the following groups.

- Doomsday Bubblers have been warning us that the stock market is in a bubble for as long as you have known them, and either want you to keep your entire portfolio in cash or in gold (or bitcoins)…

- Knee Jerk Bubblers go into hibernation in bear markets but become active as stocks start to rise and become increasingly agitated, the more they go up. They are the Bobblehead dolls of the bubble universe, convinced that if stocks have gone up a lot or for a long period, they are poised for a correction.

- Armchair Psychiatrist Bubblers use subtle or not-so-subtle psychological clues from their surroundings to make judgments about bubbles forming and bursting. Freudian in their thinking, they are convinced that any mention of stocks by shoeshine boys, cab drivers or mothers-in-law is a sure sign of a bubble.

- Conspiratorial Bubblers believe that bubbles are created by small group of evil people who plan to profit from them, with the Illuminati, hedge funds, Goldman Sachs and the Federal Reserve as prime suspects. Paranoid and ever-watchful, they are convinced that stocks are manipulated by larger and more powerful forces and that we are all helpless in the face of this darkness.

- Righteous Bubblers draw on a puritanical streak to argue that if investors are having too much fun (because stocks are going up), they have to be punished with a market crash. As the Flagellants in the bubble world, they whip themselves into a frenzy, especially during market booms.

- Rational Bubblers uses market metrics that are both intuitive and widely used, note their divergence from historical norms and argue for a correction back to the average. Viewing themselves as smarter than the rest of us and also as the voices of reason, they view their metrics as infallible and mean reversion in markets as immutable.

There are three things to keep in mind about bubblers:

- They will receive disproportionate attention in the media, for the same reasons that a reality show about a dysfunctional family will have higher ratings than one about a more normal family.

- Even the most misguided bubblers will be right at some point in time, just as a broken clock is right twice every day.

- Being right is often the worst thing that can happen to bubblers, because it seems to feed into the conviction that they are always right and leads to increasingly bizarre predictions. It is no coincidence that every market correction in history has created its gurus (who called that correction right) and those gurus have almost always found a way to discredit themselves ahead of the next one.

Defining a Bubble

…The lazy definition is that any time you see a large market correction, it is the result of a bubble bursting, but that is neither a useful definition, nor is it true.

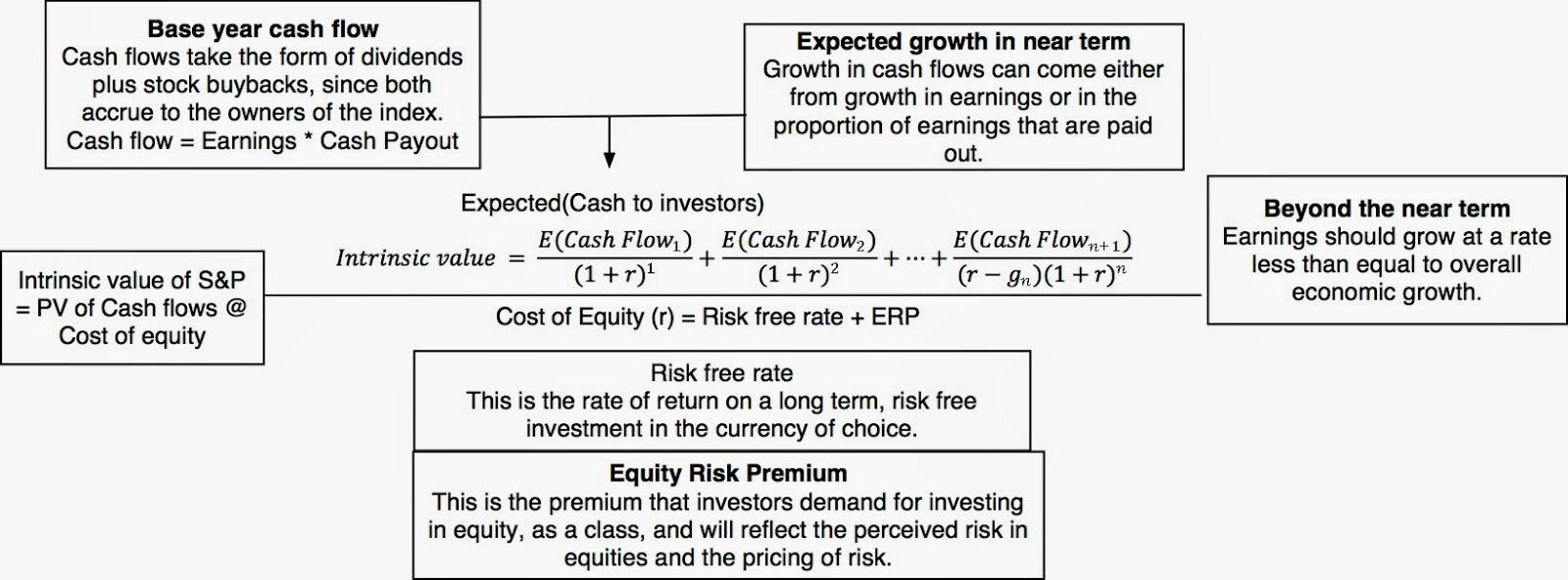

To me, a bubble reflects a market disconnect from fundamentals, where prices go up steeply, with no help from the fundamentals.

The best way of illustrating this is to go back to an intrinsic value model, where the value of stocks can be written as a function of three fundamentals:

- the base year cash flows that investors are receiving,

- the expected growth in these cash flows and

- the risk in the cash flows:

(click to enlarge)

- If cash flows increase, growth rates surge, risk free rates drop or macroeconomic risk subsides, stocks should go up, and sometimes steeply, and there is no bubble.

- At the other extreme, if stock prices go up as cash flows decrease, growth rates become more negative and risk free rates and equity risk increase, you have a bubble.

- It is far more likely, though, that you will be faced with a more ambiguous combination, where shifts in one or more fundamentals (higher growth, higher cash flows, a lower risk free rate or lower macroeconomic risk) may explain the increase in stock prices and you will have to make judgments on whether the increase is larger than warranted.

Detecting a Bubble

The benefits of being able to detect a bubble, when you are…in its midst, rather than after it bursts, is that you may be able to protect yourself from its consequences. [Below are possible] mechanisms to detect bubbles [and insights as to] how well they work:

a. PE and variants

The most widely used metric for detecting bubbles is the price earnings (PE) ratio, with variants thereof that claim to improve its predictive power.

Thus, while the conventional PE ratio is estimated by dividing the current price (or index level) by earnings in the last year or twelve months, you could consider at least three modifications.

- The first is to clean up earnings removing what you view as extraordinary or non-operating items to come up with a better measure of operating earnings. In 2002, in the aftermath of accounting scandals, S&P started computing core earnings for US companies which can differ from reported earnings significantly.

- The second is to average earnings over a longer period (say five to ten years) to remove the year-to-year volatility in earnings.

- The third is to adjust the earnings from prior periods for inflation to get a inflation-consistent or real PE ratio. In fact, Robert Shiller has a time series of PE ratios for US stocks stretching back to 1871, that uses normalized, inflation-adjusted earnings.

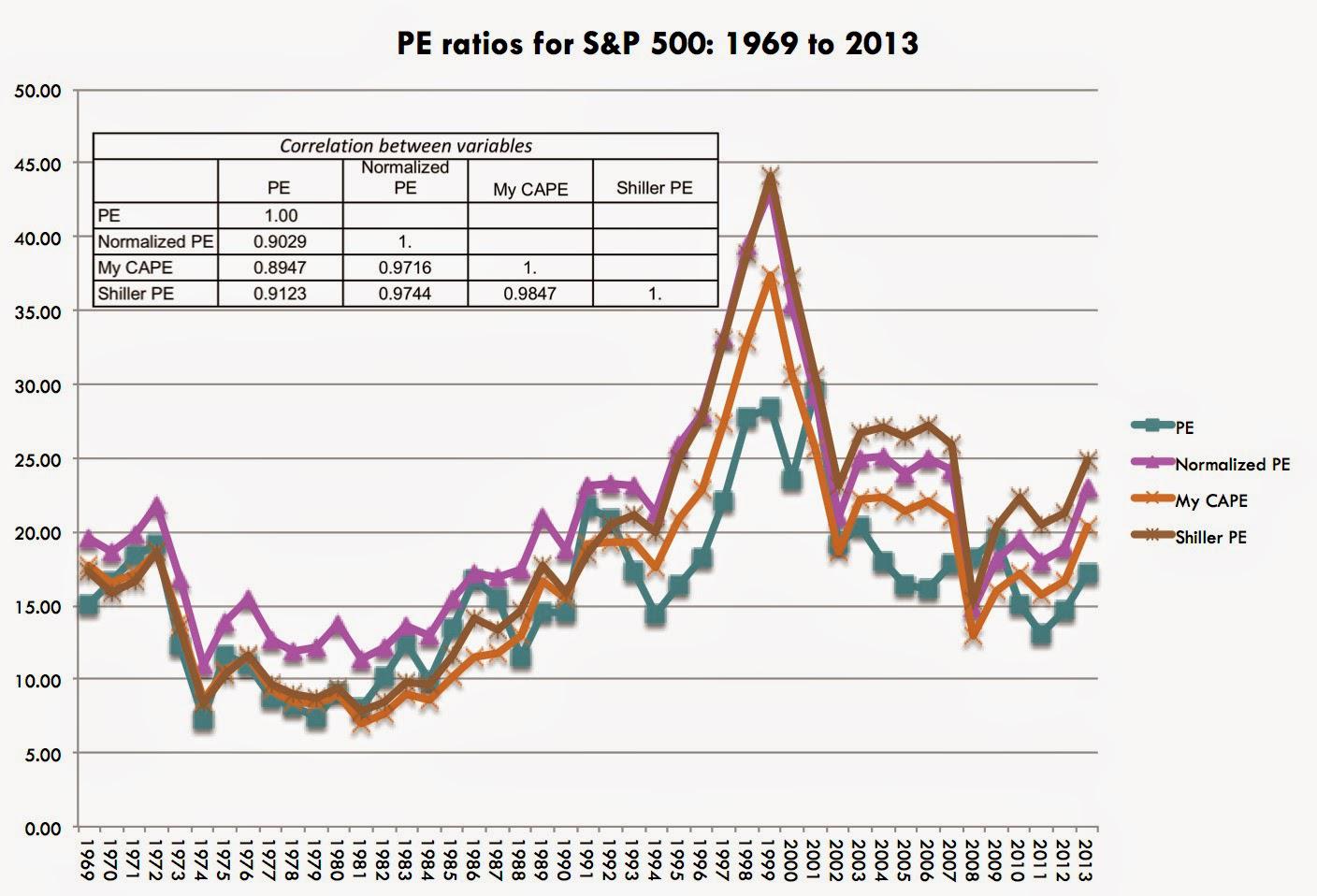

In the graph below, I report on the time trends between 1969 and 2013 in four variants of the PE ratios:

- a PE using trailing 12 month earnings (PE),

- a PE based upon the average earnings over the previous ten years (Normalized PE),

- a PE based upon my estimates of inflation-adjusted average earnings over the prior ten years (My CAPE) and

- the Shiller PE.

(click to enlarge) |

| Normalized PE used average earnings over last 10 years & My CAPE uses my inflation adjusted normalized earnings. Shiller PE is as reported in his datasets |

While the Shiller PE has become the primary weapon wielded by those who believe that we are in a bubble, perhaps because of the pedigree of its creator, the reality is that all four measures of PE move together much of the time, with a correlation of close to 90%. (If you are wondering why my time series starts in 1969, I use the S&P 500 and earnings on the index and I was unable to get reliable numbers for the latter prior to 1960. Since I need ten years of earnings to get my normalized values, my first estimates are therefore in 1969.)

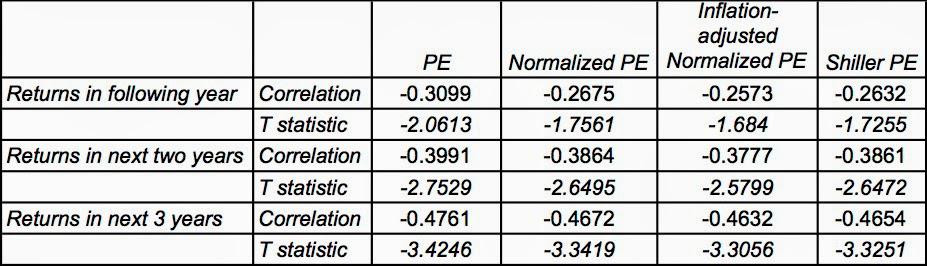

To examine whether any of these PE measures do a good job of predicting future stock returns and thus market crashes, I computed the correlation of each PE measure with annual returns on the S&P 500 over one-year, two-year and three-year periods following the computation.

(click to enlarge) |

| T statistics in italics below each correlation; numbers greater than 2.42 indicate significance at 2% level |

- The negative correlation values indicate that higher PE ratios today are predictive of lower stock returns in the future.

- That correlation is weak with one-year forward returns (notice that none of the t statistics are significant), become stronger with two-year returns and strongest with three-year returns.

- There is little in this table to indicate that normalizing or inflation adjusting the PE ratio does much in terms of improving its use in prediction, since the conventional PE ratio has the highest correlation with returns over time periods

Defenders of the PE or one its variants will undoubtedly argue that you don’t make money on correlations and that the use of PE is in detecting when stocks are over or under price. For instance, one rule of thumb suggests that a Shiller PE above 15 would indicate an over valued market, but that rule would have kept you out of US equities since 1988.

To create a rule that is more reflecting of the 1969-2013 time period, I computed the:

- 25th percentile,

- the median and

- the 75th percentile

of each of the PE ratio measures for this period.

(click to enlarge) |

| PE measures: 1969-2013 |

I then broke my sample down into four quartile classes with each PE ratio, from lowest to highest, and computed the annual stock market returns in the years following:

(click to enlarge) |

| One-year and Two-year stock returns |

The predictive power improves for PE ratios with this test, since returns in the years following high PE ratios are consistently lower than returns following low PE ratios.

- Normalizing the earnings does help, but more in detecting when stocks are cheap than when they are expensive.

- The inflation adjustment does nothing to improve predictive returns.

Note, though, that this test is biased by the fact that the quartiles were created using data from the period on which the test is run. Thus, the conclusion that you can draw from this table is that if you had known, in 1969, what the distribution of PE ratios for the S&P 500 would look like for the next 45 years (which would suggest amazing foresight on your part), you could have made money by buying when PE ratios were in the bottom quartile of the distribution and selling in the top quartile.

b. EP Ratios and Interest Rates

One of the biggest perils of using the level of PE ratios as an indicator of stock market pricing, as we have in the last section, is that it ignores the level of interest rates. If interest rates are lower, PE ratios should be higher and ignoring that relationship will lead us to conclude far too frequently (and erroneously) that stocks are over priced in low-interest rate environments.

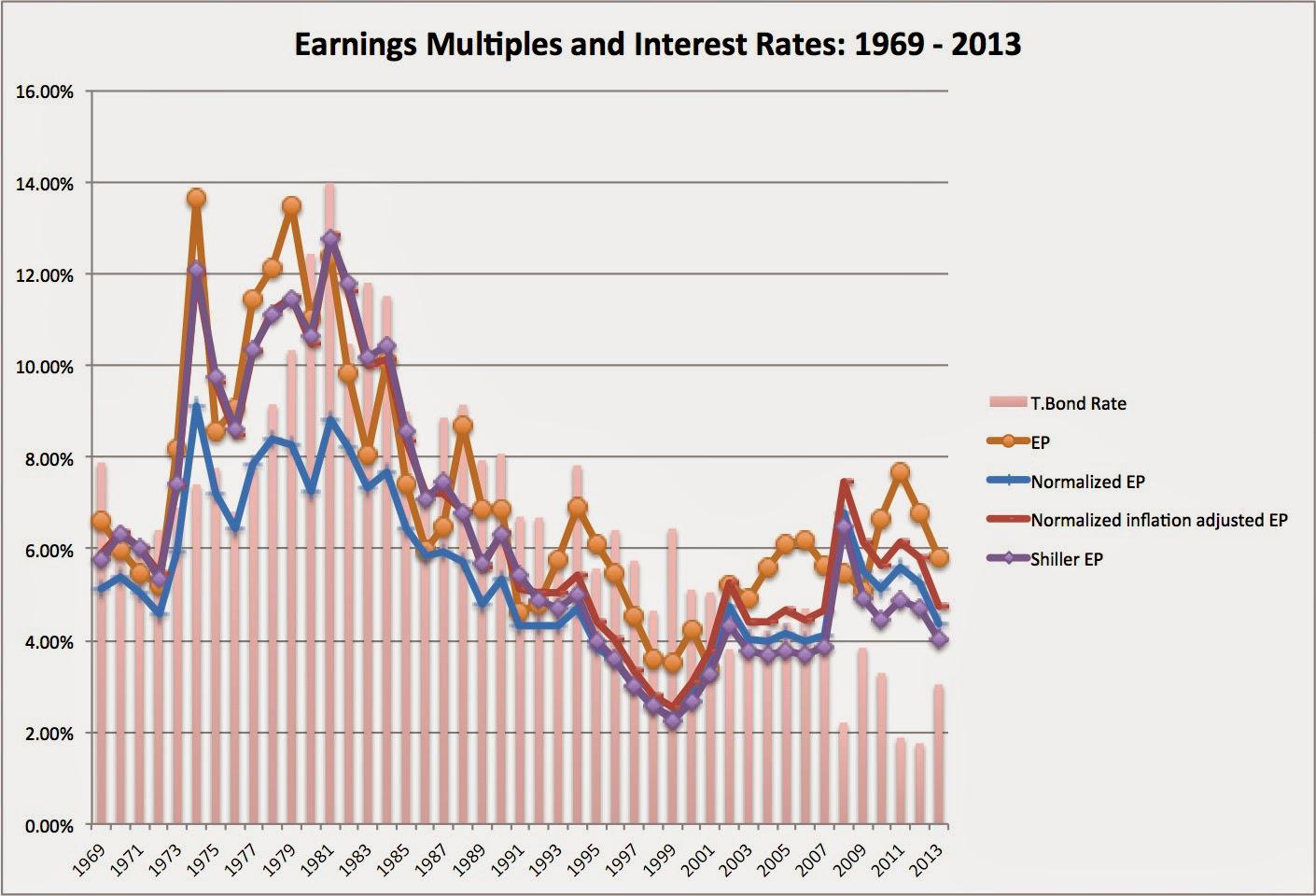

The link between PE ratios and interest rates is best illustrated by looking at how the EP ratio (the inverse of the PE ratio) moves with the T.Bond rate over time. In the figure below, I graph the movements of all four variants of EP ratios as the T.Bond rates changes between 1969 and 2013:

(click to enlarge)

It is clear that EP ratios are high when interest rates are high and low when interest rates are low. In fact, not controlling for the level of interest rates when comparing PE ratios for a market over time is an exercise in futility.

This insight is not new and is the basis for the Fed Model, which looks at the spread between the EP ratio and the T.Bond rate. The premise of the model is that stocks are cheap when the EP ratio exceeds T.Bond rates and expensive when it is lower.

To evaluate the predictive power of this spread, I classified the years between 1969 and 2013 into four quartiles, based upon the level of the spread, and computed the returns in the years after (one and two-year horizons):

(click to enlarge)

The results are murkier, but for the most part, stock returns are higher when the EP ratio exceeds the T.Bond rate.

c. Intrinsic Value

Both PE ratios and EP ratio spreads (like the Fed Model) can be faulted for looking at only part of the value picture. A fuller analysis would require us to look at all of the drivers of value, and that can be done in an intrinsic value model. In the picture below, I attempt to do so on June 14, 2014:

(click to enlarge) |

| Intrinsic valuation of S&P 500: June 2014 |

It is true that this intrinsic value is a function of my assumptions, including the growth rate and the implied equity risk premium. You are welcome to download the spreadsheet and try your own variations.

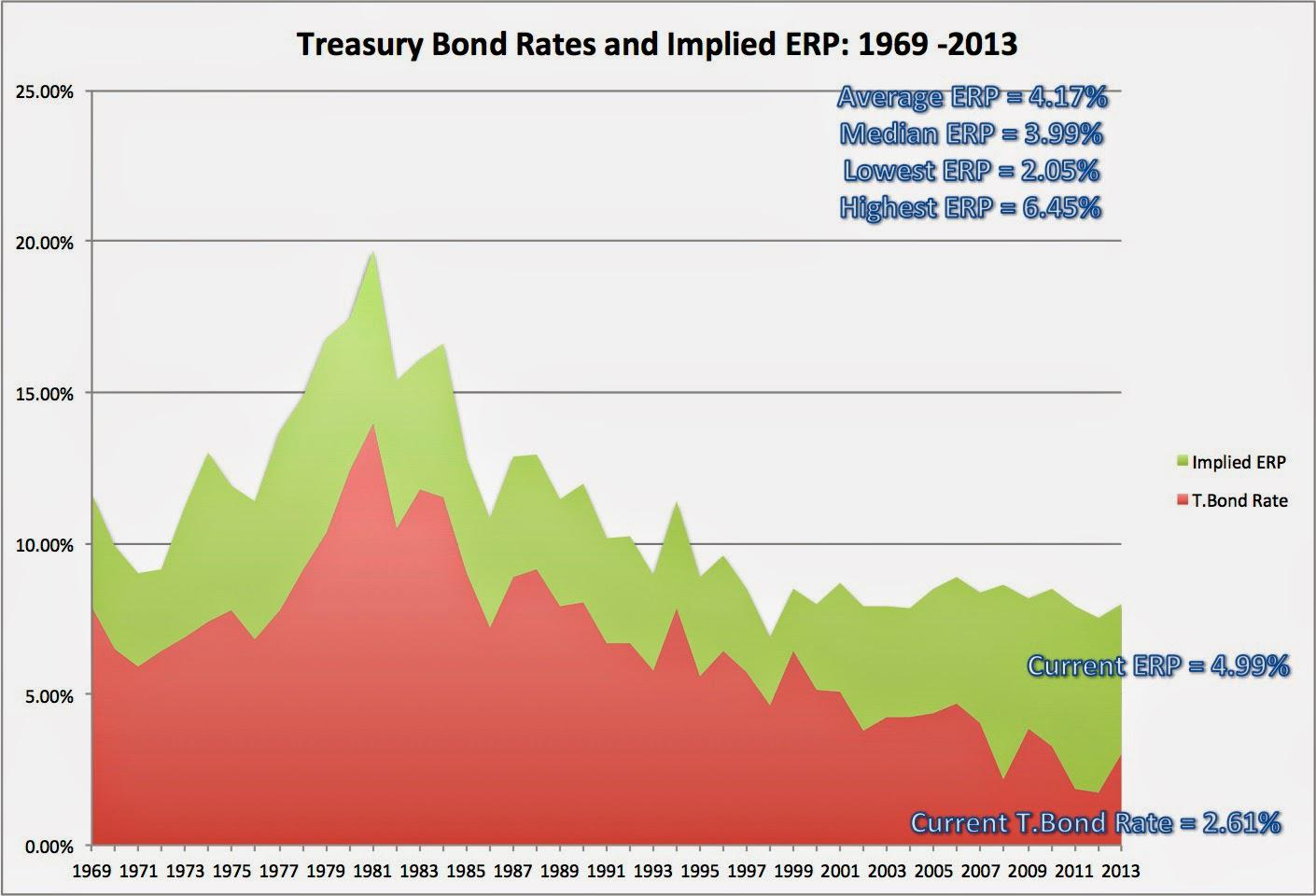

If your concern is that I have used too low an equity risk premium, you can solve, as I do at the start of each month, for an implied equity risk premium (by looking for that equity risk premium that will give you the current index level) and then comparing that value to historical values for that input:

(click to enlarge)

The current implied ERP of 4.99% is well above the historic average and median and it clearly is much higher than the 2.05% that prevailed at the end of 1999.

Are we in a bubble?

In the table below, I summarize where the market stands today on each of the metrics that I discussed in the last section:

(click to enlarge)

- If you focus on PE ratios, it is true the current levels in the market put it in the danger zone, given past history.

- However, bringing the level of interest rates into the measure (in the EP spreads) reverses the diagnosis, since stocks look under valued on these measures.

- Finally, expanding the assessment to look at growth and risk as well in the intrinsic value and ERP measures reinforces the prior suggestion that stocks are fairly valued.

While there are some who are adamant in their belief that the market is in a bubble, I remain unconvinced, especially given the level of rates today. To those who argue that earnings could drop, growth could turn negative, interest rates could go up or that there could be another global crisis lurking around the corner, has there ever been a point in time in stock market history where these concerns have not existed? And even if they do exist, the reason we demand an equity risk premium in the first place is for the uncertainty that we feel about macroeconomic variables driving value.

Bubble Belief to Bubble Action: The Trade Off

While I believe that the risk that we are in a bubble is over stated by PE ratio comparisons, you may come to a very different conclusion. Even if you do, though, should you act on that belief? The answer is not clear cut, since there are two ways you can respond to a bubble.

- The first, which I will term the passive defense, is to reduce the amount of your portfolio allocated to equity to a lower number than you would normally hold (given your age, liquidity needs and risk aversion).

- The second, which I term the active defense, is to try to profit off the market correction by selling short (or buying puts).

The trade off is then between the cost and the benefit of acting:

- The cost of acting: If you decide to act on a bubble, there is a cost. With the passive defense, the money that you take out of equities has to be invested somewhere safe (earning a risk free rate, or something close to it) and if the correction does not happen, you will lose the return premium you would have earned by investing stocks. With an active defense, the cost of being wrong about the correction is even greater since your losses will increase in direct proportion with how well stocks continue to do. (Note that using derivatives to protect yourself against market corrections or for speculation will deliver variants of these defenses.)

- The benefit of acting: If you are right about the bubble and a correction occurs, there is a payoff to acting. With the passive defense, you protect your investment (or at least that portion that you shift out of equities) from the drop. With the active defense, you profit from the drop, with the magnitude of your profits increasing with the size of the correction.

The trade off then becomes a function of three variables:

- how certain you feel about the existence of a bubble,

- how big a correction you see occurring as a result of the bubble bursting and

- how soon you see the correction coming.

To illustrate the trade off, consider a simple (perhaps simplistic) scenario, where you are fully invested in equities and believe that there is 20% probability of a market correction (which you expect to be 40%) occurring in 2 years. In addition, let’s assume that the expected return on stocks in a normal year (no bubble) is 7.51% annually and that the expected annual return if a bubble exists will be 9% annually, until the bubble bursts.

In the table below, I have listed the payoffs in:

- doing nothing (staying 100% in equities)…

- [undertaking] a passive defense (where you sell all your equity and…invest in a risk free asset earning .5%) and

- an active defense (where you sell short on equities and invest the proceeds in a risk free asset):

(click to enlarge) |

| Future value of portfolio in 2 years (when correction occurs) |

- If you remain invested in equities (do nothing), even allowing for the market correction of 40% at the end of year 2, your expected value is $1.0672 at the end of the period.

- With a passive defense, you earn the risk free rate of 0.5% a year, for two years, and the end value for your portfolio is just slightly in excess of $1.01.

- With an active defense, where you sell short and invest int he risk free rate, your portfolio will increase to $1.3072, if a correction occurs, but the expected value of your portfolio is only $0.9528, which is $0.1144 less than your do-nothing strategy.

If you have absolute conviction about the existence of a bubble and see a large correction coming immediately or very soon, it clearly pays to act on bubbles and to do so with an active defense. However, that trade off tilts towards inaction as uncertainty about the existence of the bubble increases, its expected magnitude decreases and the longer you will have to wait for the correction to occur.

I know that I am pushing my luck here but I tried to assess the trade off in a spreadsheet, where based upon your inputs on these variables, I estimate the net benefit of acting on a bubble for the passive act of moving all of your equity investment into a risk free alternative:

(click to enlarge) |

| Payoff to Passive Defense against Bubble (Correction of 40% in 2 years) |

The net payoff to acting on a bubble generates positive returns only if your conviction that a bubble exists is high (with a 20% probability, it almost never pays to act) and even with strong convictions, only if the market correction is expected to be large and occur quickly.(On a personal note, I have never found a metric or metrics that allow me to have the combination of conviction that a bubble exists, that the correction will be large enough and/or that the correction will happen within a reasonable time frame, to be a market timer. Hence, I don’t try! You may have a better metric than I do and if it yields more conclusive results than mine, you should be a market timer.)

Bubblenomics: My perspective

It is extremely dangerous to disagree with a Nobel prize winner, and even more so, to disagree with two in the same post, but I am going to risk it in this closing section:

- There will always be bubbles: Disagreeing with Gene Fama, I believe that bubbles are part and parcel of financial markets, because investors are human. More data and computerized trading will not make bubbles a thing of the past because data is just as often an instrument for our behavioral foibles as it is an antidote to them and computer algorithms are created by human programmers.

- Bubbles are not as common as we think they are: Parting ways with Robert Shiller, I would propose that bubbles occur infrequently and that they are not always irrational. Most market corrections are rational adjustments to real world shifts and not bubbles bursting and even the most egregious bubbles have rational cores.

- Bubbles are more clearly visible in the rear view mirror: While bubbles always look obvious in hindsight, it is far less obvious when you are in the midst of a bubble.

- Bubbles are not all bad: Bubbles do create damage but they do create change, often for the better. I do know that the much maligned dot-com bubble changed the way we live and do business. In fact, I agree with David Landes, an economic historian, when he asserts that “in this world, the optimists have it, not because they are always right, but because they are positive. Even when wrong, they are positive, and that is the way of achievement, correction, improvement, and success. Educated, eyes-open optimism pays; pessimism can only offer the empty consolation of being right.” In market terms, I would rather have a market that is dominated by irrationally exuberant investors than one where prices are set by actuaries. Thus, while I would not invest in Tesla, Twitter or Uber at their existing prices, I am grateful that companies like these exist.

- Doing nothing is often the best response to a bubble: The most rational response to a bubble is to often not change the way you invest.

If you believe, as I do, that it is difficult to diagnose when you are in a bubble and if you are in one, to figure when and how it will dissipate, the most sensible response to the fear of a bubble is to not change your asset allocation or investment philosophy. Conversely, if you feel certain about both the existence of a bubble and how it will burst, you may want to see if your certitude is warranted given your metric.

Attachments:

Raw Data used to estimate PE and EP ratios

PE, EP and other ratios by year: 1969-2013

Intrinsic value for S&P 500: June 14, 2014

Trade off on acting on bubbles

Editor’s Note: The author’s views and conclusions in the above article are unaltered and no personal comments have been included to maintain the integrity of the original post. Furthermore, the views, conclusions and any recommendations offered in this article are not to be construed as an endorsement of such by the editor.

*http://seekingalpha.com/article/2271053-bubble-bubble-toil-and-trouble-the-costs-and-benefits-of-market-timing?ifp=0 (© 2014 Seeking Alpha )

Related Articles:

1. These Indicators Should Scare the Hell Out of Anyone With A Stock Portfolio

…For US stocks — and by implication most other equity markets — the danger signals are piling up to the point where a case can be made that the end is, at last, near. Take a look at these examples of indicators that should scare the hell out of anyone with a big stock portfolio. Read More »

2. Is Now the Calm Before the Storm?

I’d argue that the record low volume shows investors aren’t looking ahead as much as looking behind and reminiscing at how good things have been over the past five years or so. They’re expecting more of the same even though it’s mathematically impossible people. Read More »