It’s the shrunken tax base, not lower tax rates, which is responsible for today’s revenue shortfall. A healthier economy and faster jobs growth would do much more to close the deficit than any amount of higher tax rates on the rich. Raising tax rates might weaken the economy further, and that would make it much more difficult to generate higher tax revenues. [The truth of the matter is that] nobody’s taxes need to be raised, and nobody’s spending needs to be cut—the U.S. economy is already on a glide path to the restoration of fiscal sanity. Washington: are you listening? Words: 1190

So says Scott Grannis, the Calafia Beach Pundit (http://scottgrannis.blogspot.ca) in edited excerpts from his original article* entitled Higher Taxes On The Rich Would Barely Dent The Deficit.

Lorimer Wilson, editor of www.munKNEE.com (Your Key to Making Money!), may have edited the article below to some degree for length and clarity – see Editor’s Note at the bottom of the page for details. This paragraph must be included in any article re-posting to avoid copyright infringement.

Grannis goes on to say, in part:

Obama says it is critical that the rich pay higher taxes, and he has long argued that it was the Bush tax cuts which put us in this mess, since the rich aren’t paying their “fair share.” The Republicans say it is critical that we avoid raising tax rates on anyone, since higher tax rates would jeopardize the health of the economy. As the numbers show below, higher tax rates on the rich would make only a small difference to the projected deficit, since the health of the economy and the level of federal spending are by far the major determinants of the deficit.

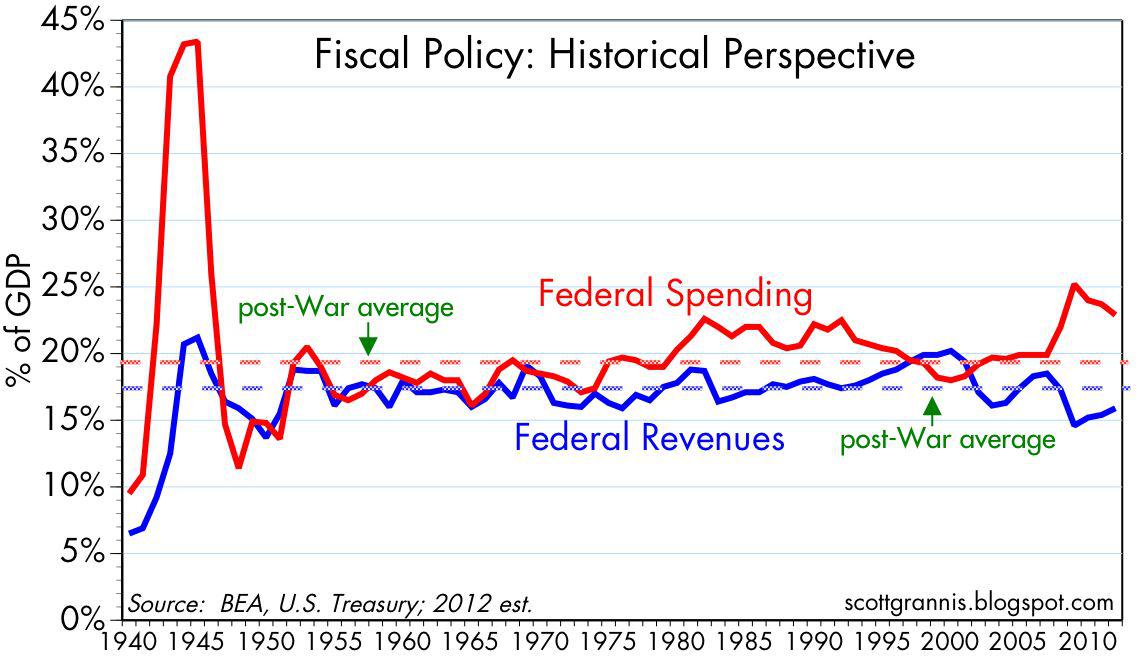

This first chart puts the federal budget in the proper long-term perspective, measuring spending and revenues as a percentage of GDP.

Spending is still well above its post-War average (22.9% vs. 19.3%), whereas revenues are only slightly below their post-War average (15.9% vs. 17.3%).

If you assume that post-War averages are the norm, then 72% of the current budget deficit of 7% of GDP is due to excess spending, and 28% is due to a revenue shortfall. It’s important to note here that federal revenues exceeded their post-War average from 2005 to 2008despite the Bush tax cuts.

Those same tax rates are delivering disappointing tax revenues today because of a shortfall of jobs and the fact that our economy is about 10-12% below its potential output.

It’s the shrunken tax base, not lower tax rates, which is responsible for today’s revenue shortfall. A healthier economy and faster jobs growth would do much more to close the deficit than any amount of higher tax rates on the rich.

(click to enlarge)

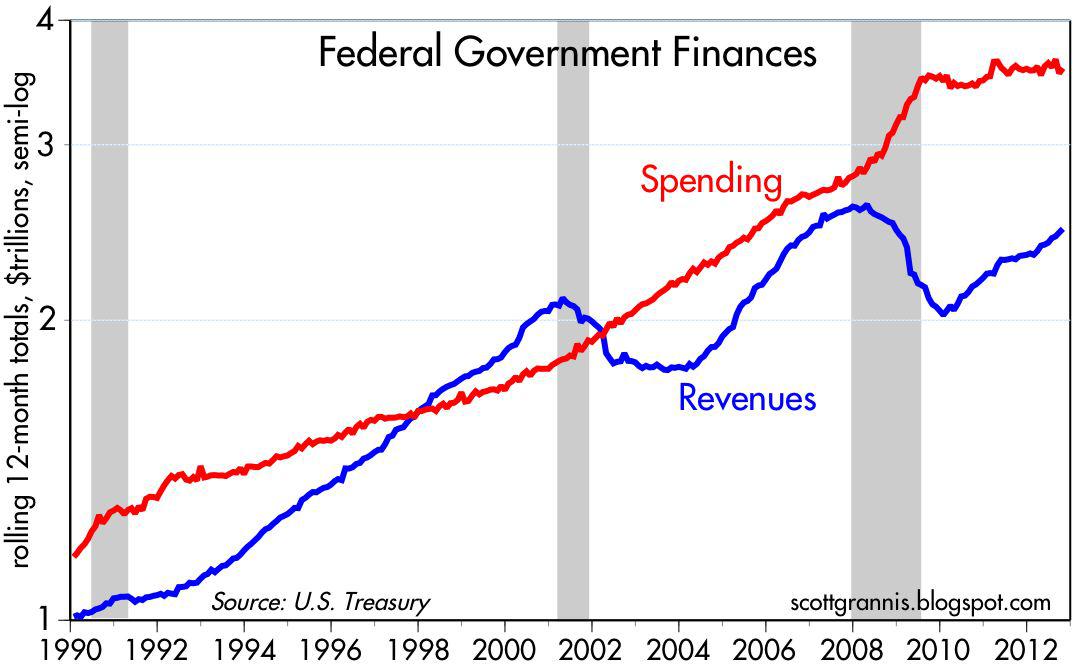

The chart below plots the running 12-month total of nominal federal spending and revenues. Two rather surprising revelations are apparent.

After surging in 2008 and 2009, federal spending growth has slowed to a crawl, thanks mainly to Congressional gridlock and the unwinding of automatic stabilizers (e.g., fewer people collecting unemployment insurance).

Revenues have surged by $446 billion since hitting a low in early 2010, without any increase in tax rates and despite a two-year payroll tax holiday, mainly because an expanding economy, rising corporate profits, and the addition of 5 million new jobs have expanded the tax base.

Who in the world is currently reading this article along with you? Click here

Even if the economy were to continue growing at a measly 2% rate, there is every reason to think that revenues would continue to rise without the need for higher tax rates. Raising tax rates, however, might weaken the economy further, and that would make it much more difficult to generate higher tax revenues.

(click to enlarge)

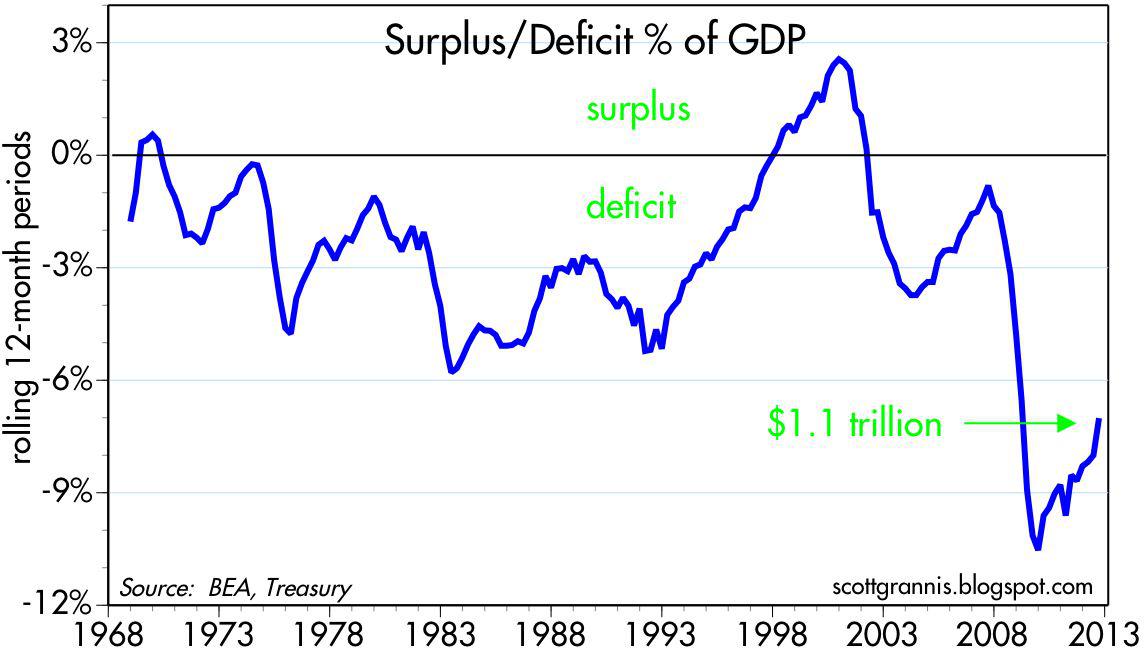

The chart below shows the impressive reduction in the federal deficit as a percent of GDP that has occurred over the past three years—from a high of 10.5% in late 2009 to the current 7%.

If nothing changes and current trends were to continue (spending growth of 3% per year, revenue growth of 7% per year, and nominal GDP growth of 4% per year), the deficit would decline to approximately 6% of GDP by the end of next year, and return to its long-term historic average of 2% of GDP in seven years.

Nobody’s taxes need to be raised, and nobody’s spending needs to be cut—the U.S. economy is already on a glide path to the restoration of fiscal sanity. Washington: are you listening?

(click to enlarge)

If anything is likely to change in a big way in coming years, however, it is increased entitlement spending, particularly under ObamaCare and Social Security. This is what should be getting the priority these days, not tax rates.

A Bloomberg News article…reinforces my point that the shortfall in revenue today is not due to tax rates that are too low, but rather due to a weak economy:

… boosting taxes for the wealthiest 2 percent would bring in $58.1 billion in fiscal year 2013, according to Bloomberg calculations based on data from the [left-leaning] Tax Policy Center. The CBO estimates the government’s finances will show a shortfall of $1.04 trillion, assuming almost all the tax increases and automatic spending cuts that are slated to take effect next year are totally averted.

“It’s not very much, but it is a step in the right direction,” Roberton Williams, a senior fellow at the nonpartisan Tax Policy Center in Washington, said in a telephone interview. “In order to close half the budget deficit by raising taxes on the rich, you would have to raise their tax rate up to about 90 percent. That’s not going to happen.”

According to some estimates I’ve seen, if Obama gets his request for higher income, dividend, capital gains and estate tax rates rise for those making more than $250K per year, that could raise up to $120 billion to federal revenues next year, assuming no adverse consequences for economic growth. That’s not an assumption I’m comfortable making, but nevertheless the revenue gains that might result from boosting tax rates for the rich are still a relatively small fraction of the total projected deficit.

Sign up HERE to receive munKNEE.com’s unique newsletter, Your Daily Intelligence Report

It’s FREE

It contains the “best of the best” financial, economic and investment articles to be found on the internet

It’s presented in an “edited excerpts” format to provide brevity & clarity of content to ensure a fast & easy read

Don’t waste time searching for articles worth reading. We do it for you and bring them to you each day!

Sign up HERE and begin receiving your newsletter starting tomorrow

Greg Mankiw uses data from the Tax Policy Center to make the point that putting a cap on total deductions could raise significant revenue from the rich without increasing their marginal tax rates, and that is important since it avoids creating a disincentive to additional work and investment: According to the Tax Policy Center, if we cap itemized deductions at $50,000 and keep tax rates as they are today, we would raise $749 billion in tax revenue over ten years. Moreover, according to the TPC’s distribution table, 96.2 percent of the extra revenue would come from the top quintile, with 79.9 percent from the top one percent.

Conclusion

Given today’s political realities, the best outcome of the “fiscal cliff” negotiations, from my perspective, would be:

an agreement to meaningfully reduce future spending on entitlements,

extend the current tax structure for at least another year or two, and

put a cap on total deductions.

This would reinforce the fiscal sanity glide path (i.e., slow growth in spending coupled with continued expansion of the tax base), and give politicians and markets plenty of time to notice that the U.S. federal budget outlook is not nearly as bad as most seem to believe.

If the “fiscal cliff” negotiations end up being driven by political considerations rather than economic realities, higher tax rates on the rich would only increase the odds that the economy is likely to continue growing at a sub-par pace…for the foreseeable future. That would be a very unfortunate conclusion to such an important policy debate.

Editor’s Note: The above post may have been edited ([ ]), abridged (…), and reformatted (including the title, some sub-titles and bold/italics emphases) for the sake of clarity and brevity to ensure a fast and easy read. The article’s views and conclusions are unaltered and no personal comments have been included to maintain the integrity of the original article.

Many articles are being written these days that more or less scope the dire financial circumstances the U.S. is in. That being said, I had not been able to find one “analyst” – even one – who had the guts to outline the probable outcome and general hopelessness of the situation and to offer any meaningful prescription for investors to survive this coming catastrophe – until now. Words: 710

Screams about how these top-bracket income tax and capital-gains tax increases will ruin the economy by hammering spending and eliminating the incentive to work can be seen for what they are – the whining of people who don’t want their taxes to go up [BUT, when it comes to the possible increase in the top tax on dividends they have a point – a BIG point – a VERY big point. Let me explain.] Words: 450

Financial repression occurs when governments channel funds into their own sovereign bonds in order to reduce debt levels through mechanisms such as directed lending, caps on interest rates, capital controls, debt monetization, or by other means. The promise of financial repression is that it will hold down government borrowing costs and reduce government debt levels, but critics argue that financial repression merely targets the producers of society, i.e., the middle class, and therefore harms the economy. Let’s take a look at financial repression ands its supposed pros and cons. Words: 1486

People riding a runaway train can party and remain oblivious to the fact that the train is about to crash into a huge obstacle. Our runaway financial train is about to destroy the status quo as it crashes into the obstacle of mathematical consequences – the inevitable financial train wreck. “If something cannot go on forever, it will stop.” [Let me explain.] Words: 974

It’s easy to find analysts and investors who are certain that a deal [to avoid the fiscal cliff] will be reached, or at least that the can will be kicked down the road to buy more time. It’s also easy to find more pessimistic views that are based on the lack of cooperation in the past, and a deeply polarized country and political system. However, I think many are missing the point, which is that austerity is coming to America – taxes are going up and government spending will be reduced – [and. as such,] the United States is likely to face a recession and market correction in 2013, regardless of whether or not a compromise is reached over the Fiscal Cliff. Words: 970

This short video – on the sustainability of government spending – should be watched by everyone, including those not yet old enough to vote. It should be shown in every high school and college classroom.

The level of debt has surpassed the possibilities of being serviced. Mathematically, the debt problem cannot be solved, regardless of economic policies. That, unfortunately, is written. For it to be serviceable would be to violate the laws of mathematics and that cannot happen. [As such, America is quickly approaching a catastrophic economic collapse. As repelling as that sounds, it’s in your own best interest to learn just how bad the situation is. This article is an attempt to do just that.] Words: 310

The corrosive nature of politics and government has destroyed the economy and the moral fiber of citizens. These issues are not insurmountable, but they are very close to being so. Their ramifications are potentially existential in nature: the average length of life, the very time span or cycle of a nation has been proven in history to be approximately 250 years. Since the USA was born in 1776 this says we have about 14 years of life remaining for America. The way things are going we don’t doubt it. [Let me explain.] Words: 768

9. If You Are Not Preparing For a US Debt Collapse, NOW Is the Time to Do So! Here’s Why

Timing the U.S. debt implosion in advance is virtually impossible. Thus far, we’ve managed to [avoid such an event], however, this will not always be the case. If the U.S. does not deal with its debt problems now, we’re guaranteed to go the way of the PIIGS, along with an episode of hyperinflation. That is THE issue for the U.S., as this situation would affect every man woman and child living in this country. [Let me explain further.] Words: 495

What is the “Fiscal Cliff”? What would its ramifications be? Will it tip the U.S. into a recession? What are the critical economic building blocks that would be adversely affected? How best should you position your portfolio for such an eventuality.

We all know that high debt is a growth killer and, at the moment, the U.S. has a budget deficit of about $1 trillion. That’s a very big number…The question is, at what point do countries have to deal with high debt levels? How high do debt levels have to be before one has to deal with the problem by lowering budget deficits? Also, what are the consequences of such debt and budget reductions? Words: 500

“Portfolio managers have been swayed by hope over experience” when it comes to anticipating the effects the fiscal cliff will have on markets. Investors aren’t giving as much attention to the fiscal cliff as they should be, and that may be helping to set the markets up for a repeat of last year, when the debt ceiling negotiations sent stocks plummeting.

The outcome of the election of 2012 will [only] determine the rate of speed at which we approach the [financial] cliff [because] neither political alternative is willing to change course, to steer away from the cliff. The cliff is so high that whether we go over it at 200 mph (Obama) or whether we merely slip over the edge (Romney), the end result is the same — fatal for the economy and perhaps our entire political system. It is the fall that will kill us. [This article explains why that is going to be the case.] Words: 1135

Under current law, a sharp reduction in the federal budget deficit between 2012 and 2013 will cause the economy to contract but, the Congressional Budget Off ice projects, will also put federal debt on a path more likely to be sustainable over time. To illustrate the eff ects of fiscal tightening, CBO compared its projections under current law (the “baseline” projections) with projections under an alternative set of policies — two scenarios in a broad spectrum of choices – in the infographic below.

The U.S. federal government is scheduled to implement a fiscal tightening of unprecedented severity (approx. 5% of GDP) at the start of 2013. The last time a tightening of such proportions occurred (3% of GDP in 1969) it presaged a recession. Thus, unless mitigated by an act of Congress, we expect the fiscal cliff would lead the U.S. into a recession in 2013. Below, in 26 charts, we examine all aspects of the impending crisis to gauge its potential impact on the credit markets and, by extension, our strategic investment recommendations.

This post shows JPMorgan’s estimated probabilities on four different fiscal cliff outcomes, conditional on who wins the presidential election in November.

Unless the government acts quickly, it is probable that the term “fiscal cliff” will become a household phrase over the next few months. Unfortunately, this is reminiscent of the budget ceiling crisis about a year ago. In this report we will explain what the cliff is, discuss the worst case scenario, and determine what, if anything, you should do about it. Words: 1436

If Congress addresses the issue by maintaining the current tax and spending policies we will get more of the same economy we have experienced for the past three years (all else being equal). [That being said,] what if Congress goes over the fiscal cliff hit? This blog post is designed to asses the impact. Words: 1362

revenue shortfall. A healthier economy and faster jobs growth would do much more to close the deficit than any amount of higher tax rates on the rich. Raising tax rates might weaken the economy further, and that would make it much more difficult to generate higher tax revenues. [The truth of the matter is that] nobody’s taxes need to be raised, and nobody’s spending needs to be cut—the U.S. economy is already on a glide path to the restoration of fiscal sanity. Washington: are you listening? Words: 1190

revenue shortfall. A healthier economy and faster jobs growth would do much more to close the deficit than any amount of higher tax rates on the rich. Raising tax rates might weaken the economy further, and that would make it much more difficult to generate higher tax revenues. [The truth of the matter is that] nobody’s taxes need to be raised, and nobody’s spending needs to be cut—the U.S. economy is already on a glide path to the restoration of fiscal sanity. Washington: are you listening? Words: 1190