Economist Hyman Minsky argued that there is an inherent instability in financial markets…[and that] an abnormally long bullish cycle of bullish speculation spurs an asymmetric rise in market speculation that eventually results in market instability and collapse and that, the longer the speculation occurs, the more severe the problem will be. [To put it succinctly,] a “Minsky Moment” is the reversal of leverage following prolonged bullish speculation.

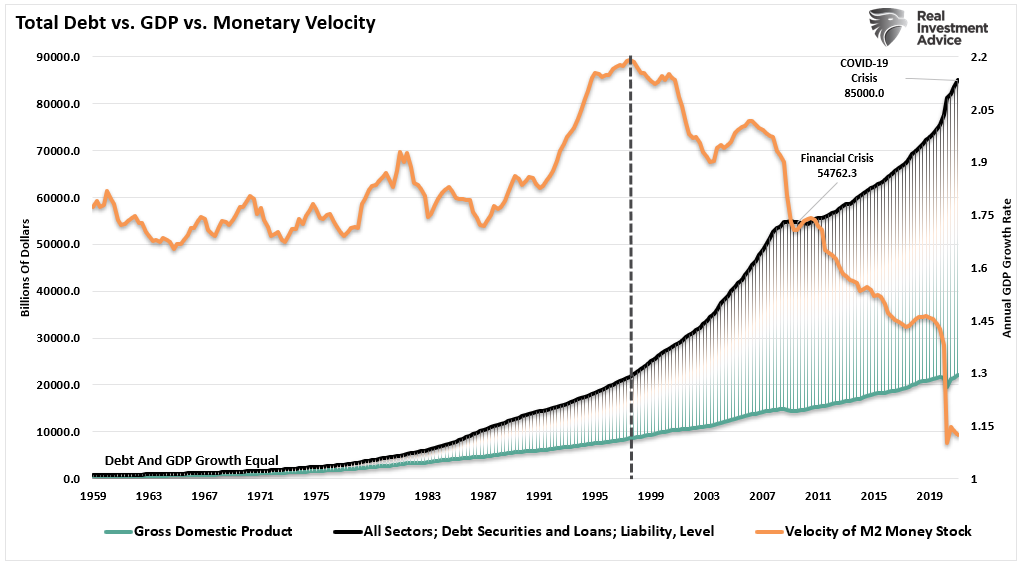

Minsky argued that the economic cycle is driven more by surges in the banking system and credit supply…[than the] relationship between companies and workers in the labor market and, since the Financial Crisis, the surge in debt across all sectors of the economy is unprecedented.

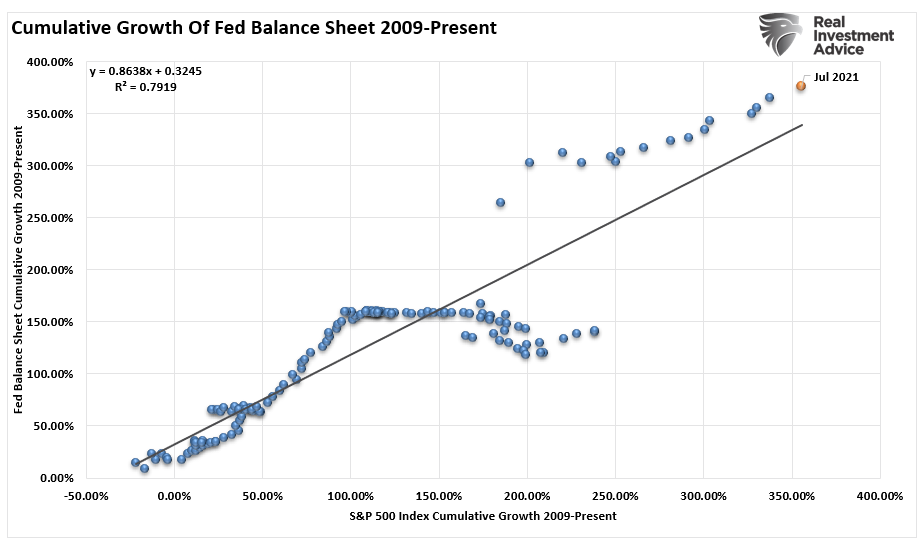

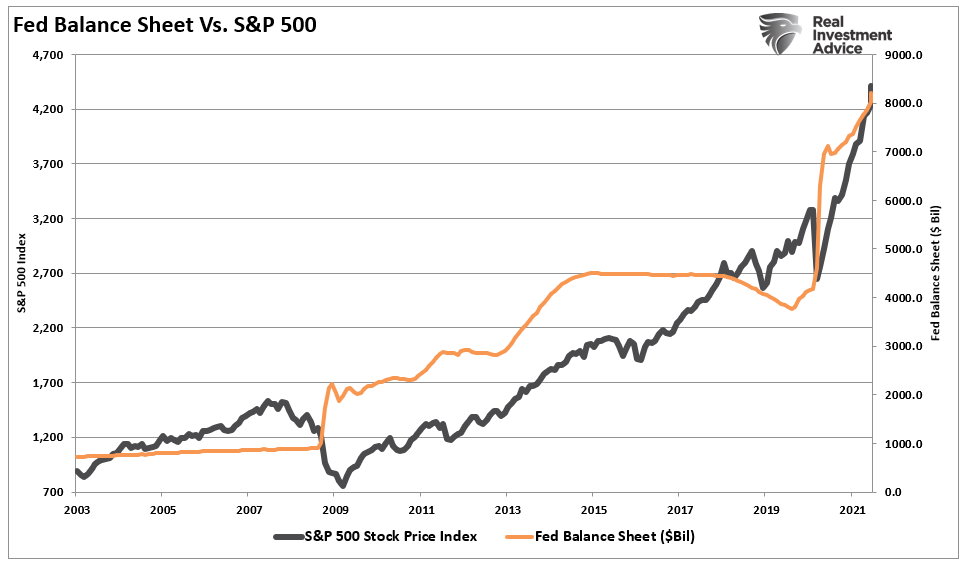

Importantly, much of the Treasury debt is being monetized, and leveraged, by the Fed to, in theory, create “economic stability.” Given the high correlation between the financial markets and the Federal Reserve interventions, there is credence to Minsky’s theory. With an R-Square of nearly 80%, the Fed is clearly impacting financial markets.

Those interventions, either direct or psychological, support the speculative excesses in the markets currently.

Bullish Speculation Is Evident

…Currently, we see clear evidence of “bullish speculation” due to:

- Commission-free trading and mobile apps that have exploded retail trading

- A surge in IPO’s

- A record increase in SPAC’s

- Investors paying record multiples and prices for money-losing companies

- Record increases in option contract speculation

- Margin debt at new highs and near-record annual increases

- A widely accepted belief “this time is different,” due to the “Fed Put”

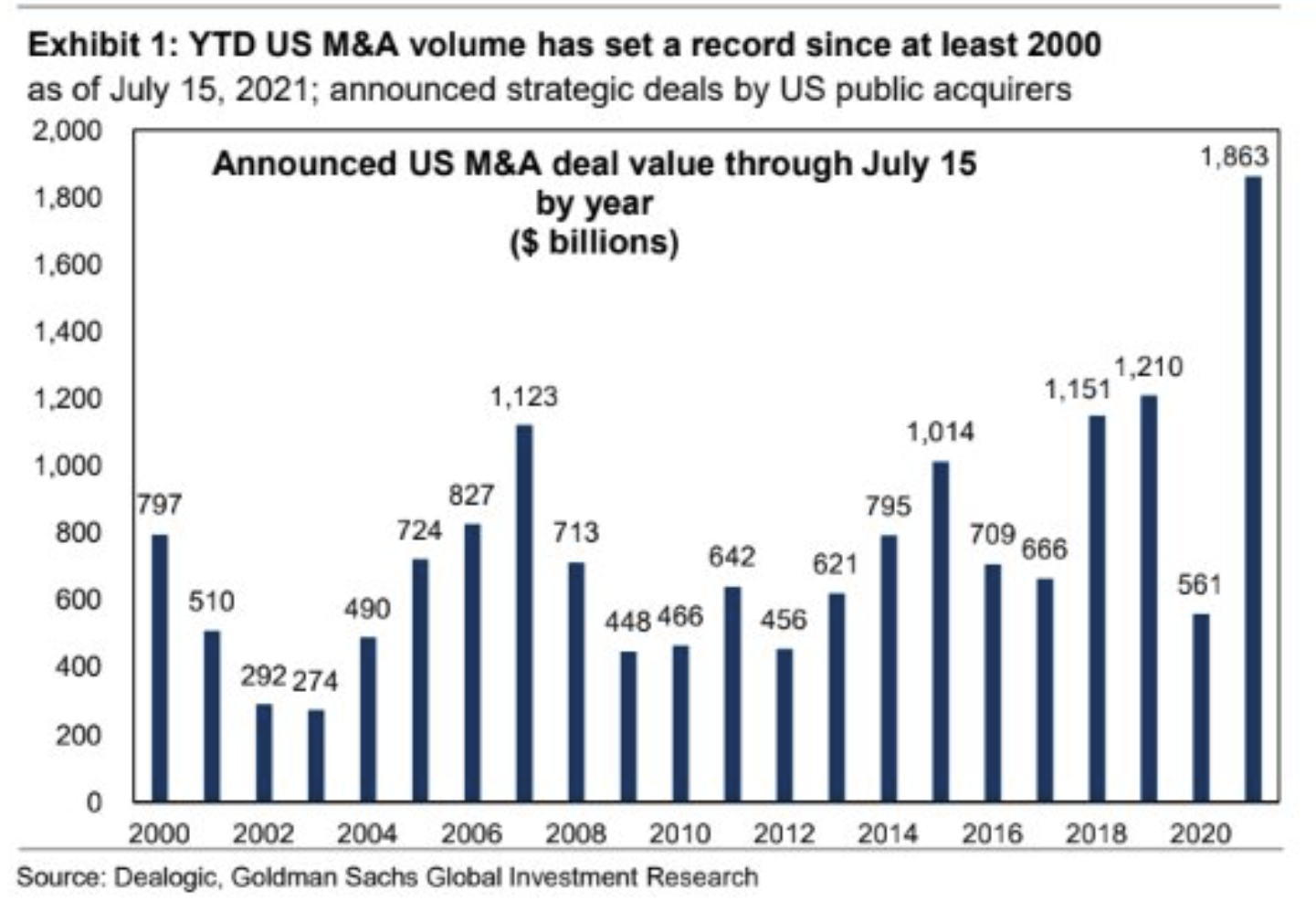

- Record M&A activity

These issues are not new as they have all been present, in one form or another, at every prominent market peak in history. Notably, what fosters these periods of exuberance in markets is “stability.” In other words, there are periods of exceptionally low volatility in markets, which breed overconfidence and speculative appetites. However, these periods of exceptionally low volatility are also a problem.

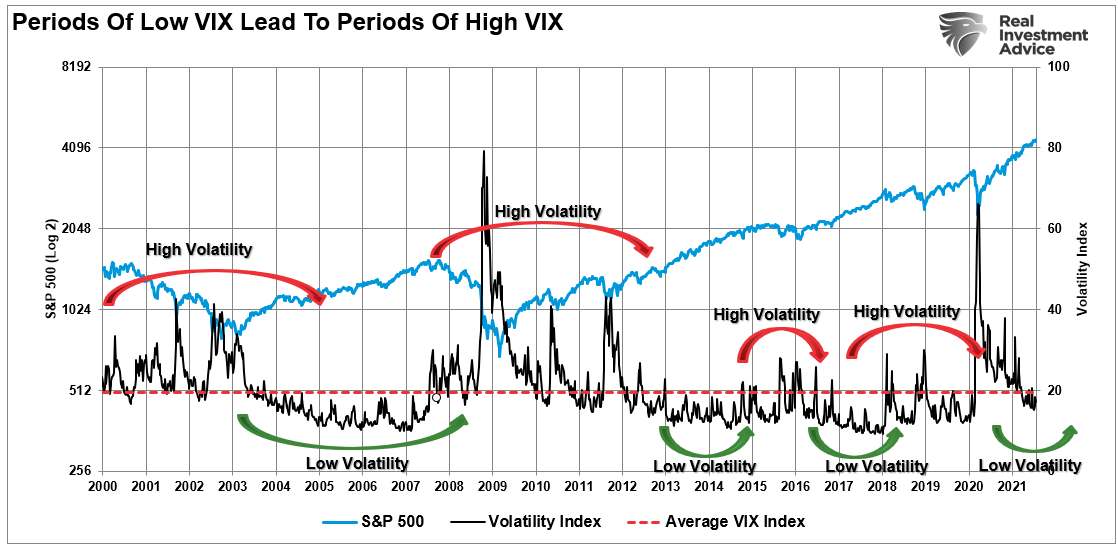

The Instability Of Stability

Note in the chart below that long periods of “stability” with regularity lead to periods of “instability.”

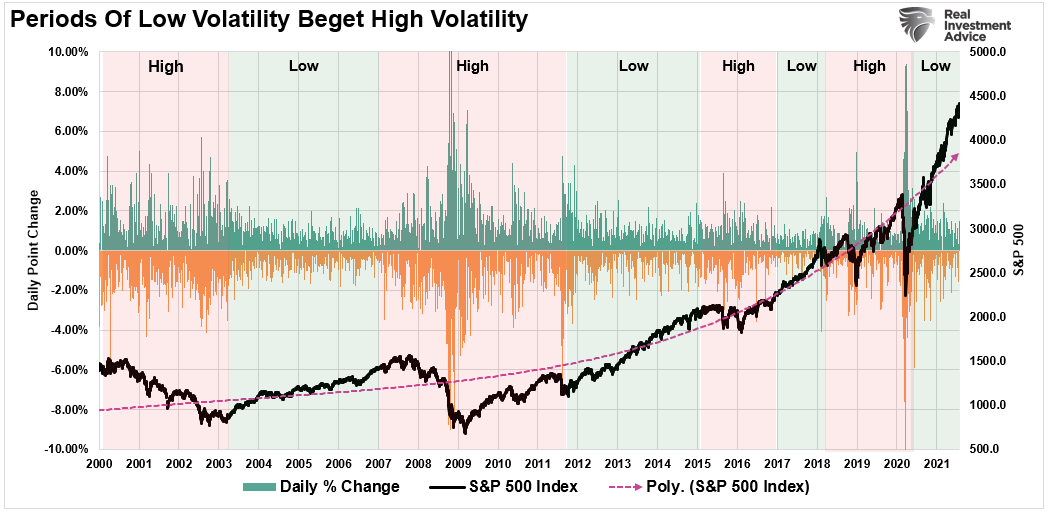

Given the volatility index is a function of the options market, we can also view these alternating periods of “stability/instability” by looking at the daily price changes of the index itself.

A “Minsky Moment” is the reversal of leverage following prolonged bullish speculation. The build-up of leverage is the direct result of the complacency occurring from low-volatility market regimes.

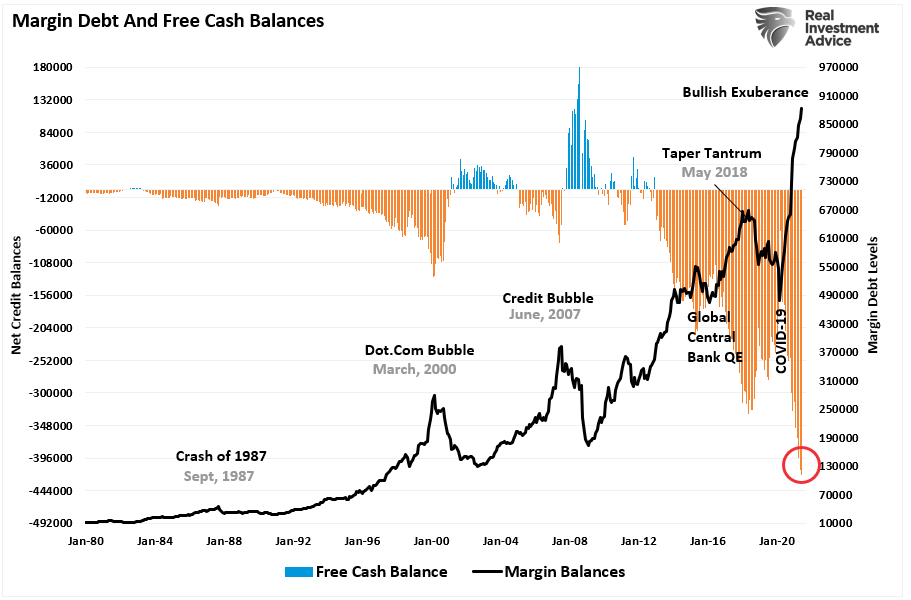

One way to look at “leverage,” as it relates to the financial markets, is through “margin debt,” and in particular, the level of “free cash” investors have to deploy. For example, in periods of “high speculation,” investors are likely to be levered (borrow money) to invest, which leaves them with “negative” cash balances.

Critically, while “margin debt” provides the fuel to support the bullish speculation, it is also the accelerant for “crisis” when it occurs.

The Dependency Of The Fed

The dependency on maintaining “stability” is the most significant problem facing the Fed.

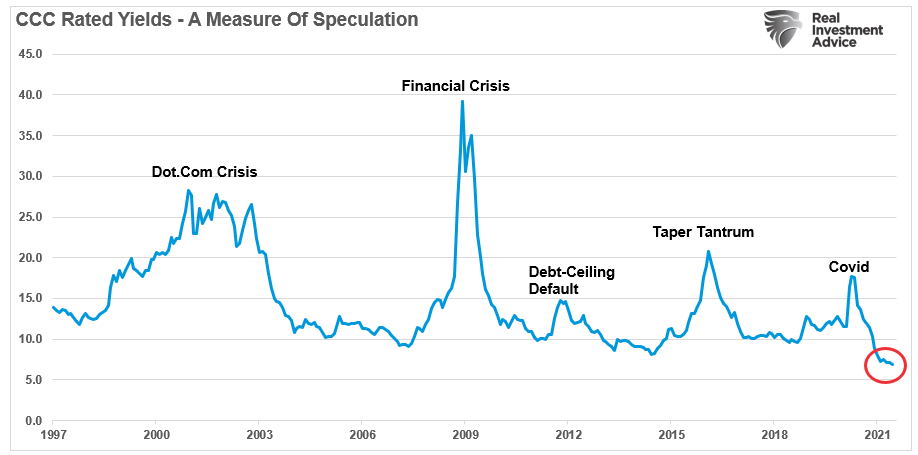

- Currently, the Fed has created a “moral hazard” in the markets by inducing investors to believe they have an “insurance policy” against loss. Therefore, investors are willing to take on increasing levels of financial risk.

- This level of speculative risk-taking gets shown in the current yields of CCC-rated bonds. These are corporate bonds just one notch above “default” and should carry very high yields to compensate for that default risk.

As noted, with the entirety of the financial ecosystem more heavily levered than ever, the “instability of stability” is now the most significant risk.

The Paradox

The “stability/instability paradox” assumes that all players are rational…[and] the Fed is highly dependent on this assumption as it provides the “room” needed, after more than 12-years of the most unprecedented monetary policy program in U.S. history, to try and navigate the risks that have built up in the system.

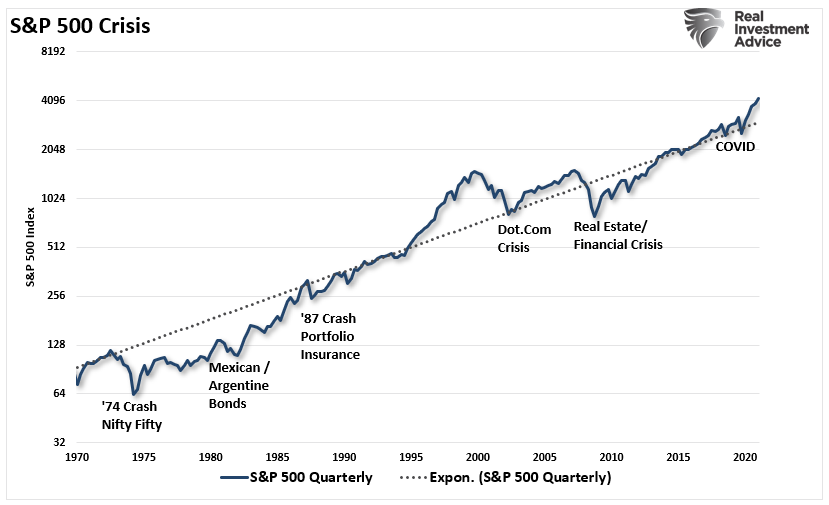

The Fed is dependent on “everyone acting rationally” but, unfortunately, that has never been the case as, throughout history, the Fed’s actions have repeatedly led to adverse outcomes despite the best of intentions.

- In the early 70’s it was the “Nifty Fifty” stocks,

- Then Mexican and Argentine bonds a few years after that

- “Portfolio Insurance” was the “thing” in the mid -80’s

- Dot.com anything was a great investment in 1999

- Real estate has been a boom/bust cycle roughly every other decade, but 2006 was a doozy

- Today, it’s ETF’s and “Passive Investing,” and levered credit.

Another measure of “exuberance” is the deviation from the long-term moving averages. As shown below, the market is pushing an extreme deviation from the 4-year moving average, with the 12-month relative strength index (RSI) in very overbought territory, and the current period of exuberance could last another 12-18 months, potentially even longer. The extended period of “stability” will lead investors to “dismiss” the warning as “wrong” given it did not immediately result in a correction.

As Howard Marks once quipped:

“Being early is the same as being wrong.”

Therefore, while investors must manage portfolios in the near term to generate returns, it is undoubtedly a warning you should not dismiss entirely.

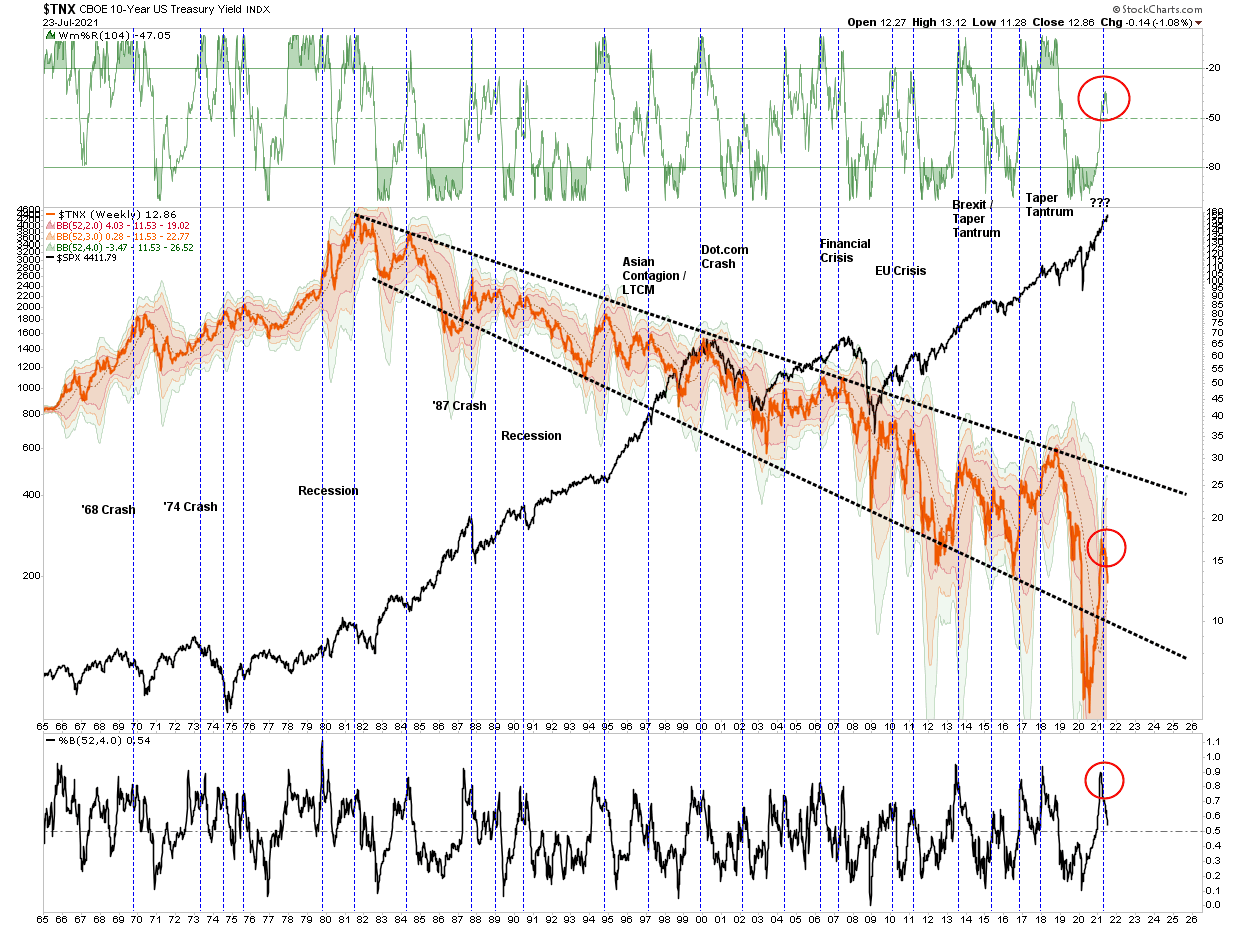

Rates Are Also Sending A Warning

The risk to this entire market remains a credit-related event. Risk concentration always seems rational at the beginning, and the initial successes of the trends it creates can be self-reinforcing. That is, until suddenly, and often without warning, it all goes “pear-shaped.”…

With risk elevated, the Fed continues to supply liquidity at the rate of $120 billion a month. The sole goal, of course, is to maintain “stability.” Importantly, with inflation pushing 5%, and economic growth expected to surpass 4%, interest rates should be at a corresponding level. However, interest rates are warning that “something is not quite right” in the financial system. Previously, when rates have risen from lows and peaked, such has preceded periods of “market instability.”

Will this time be different – maybe – but history suggests it won’t be and all of this underscores the single most significant risk to your investment portfolio. In extremely long bull market cycles, investors become “willfully blind” to the underlying inherent risks or, rather, it is the “hubris” of investors that they are now “smarter than the market” yet the list of concerns remains despite being completely ignored by investors and the mainstream media.

- Growing economic ambiguities in the U.S. and abroad: peak autos, peak housing, peak GDP,

- excessive valuations that exceed earnings growth expectations,

- the failure of fiscal policy to ‘trickle down,’

- geopolitical risks,

- flattening of yield curves amid surging economic growth,

- record levels of private and public debt, and

- exceptionally low junk bond yields.

For now, none of that matters as the Fed seems to have everything under control.

Conclusion

The more the market rises, the more reinforced the belief “this time is different” becomes. Yes, our investment portfolios remain invested on the long side for now. (Although we continue to carry slightly higher levels of cash and hedges. However, that will change, and rapidly so, at the first sign of the “instability of stability.”

When will the next “Minsky Moment” arrive? We don’t know. What we do know is that by the time the Fed realizes what they have done, as always, it will be too late.

Editor’s Note: The above version of the original article by Lance Roberts, has been edited ([ ]) and abridged (…) for the sake of clarity and brevity to ensure a fast and easy read. The author’s views and conclusions are unaltered and no personal comments have been included to maintain the integrity of the original article. Furthermore, the views, conclusions and any recommendations offered in this article are not to be construed as an endorsement of such by the editor. Also note that this complete paragraph must be included in any re-posting to avoid copyright infringement.

A Few Last Words:

- Click the “Like” button at the top of the page if you found this article a worthwhile read as this will help us build a bigger audience.

- Comment below if you want to share your opinion or perspective with other readers and possibly exchange views with them.

- Register to receive our free Market Intelligence Report newsletter (sample here) in the top right hand corner of this page.

- Join us on Facebook to be automatically advised of the latest articles posted and to comment on any of them.