Injecting massive amounts of liquidity into the banking system can spur dramatic economic growth if that liquidity is used. On the other hand, if public perception is negative and fearful, that liquidity remains untapped and no growth occurs. We are in a new earnings season and for the most part – based on lowered expectations – the numbers are looking OK so what should we expect based on these modestly improving numbers? Words: 2176

dramatic economic growth if that liquidity is used. On the other hand, if public perception is negative and fearful, that liquidity remains untapped and no growth occurs. We are in a new earnings season and for the most part – based on lowered expectations – the numbers are looking OK so what should we expect based on these modestly improving numbers? Words: 2176

So asks Joseph Stuber in edited excerpts from his original article as posted on Seeking Alpha under the title Can Perception Continue To Trump Fact?

Lorimer Wilson, editor of www.FinancialArticleSummariesToday.com (A site for sore eyes and inquisitive minds) and www.munKNEE.com (Your Key to Making Money!), has edited the article below for length and clarity – see Editor’s Note at the bottom of the page. This paragraph must be included in any article re-posting to avoid copyright infringement.

Stuber goes on to say, in part:

- sharp drop in unemployment a few weeks back,

- consumer spending has shown a modest jump,

- bank lending has shown a modest increase.

- The real estate market data is showing some signs of improvement and

- earnings have met or exceeded estimates. In fact, the more watched number – sales volume – is even beating expectations.

Perception drives stock prices and the perception may be shifting for the moment. As I see it 2 scenarios could develop:

- We finally break free from the liquidity trap that has stifled growth since the recession and fundamentally change the course of the economy.

- We shift focus in the 4th quarter back to the underlying fundamentals and away from QE euphoria.

Secenario #1: Bernanke’s Release of Liquidity

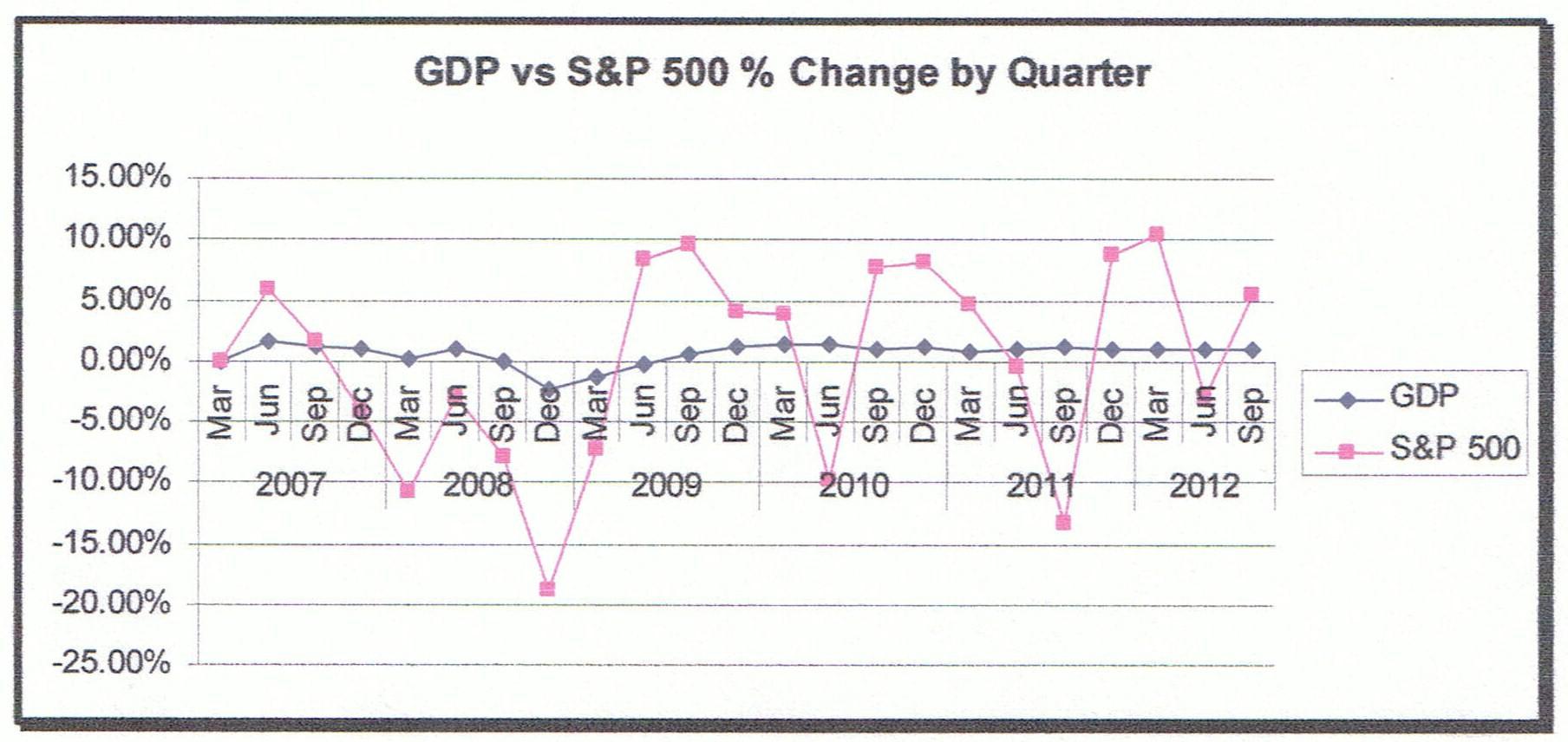

A look at the chart below is interesting in that it shows dramatic stock market shifts up and down even as GDP growth has remained virtually flat. In the last 5 years we have been range bound but that range has swung from plus 10% to minus 15% relative to the 1st quarter of 2007. There is little doubt we are going to move – the question is which way.

(click to enlarge)

Economic growth must come on the backs of the consumer. If the public refuses to buy into the premise that economic growth is occurring then it won’t occur. It is as simple as that. What is required is a public that feels positive about the future and willing to step out and buy that much needed car or that new living room furniture. If the prevailing sentiment is that things are not getting better and might very well get worse then the consumer holds off on these purchases.

Since the recession the consumer has been guarded at best, and not at all positive. Ben Bernanke has been vigilant in his efforts to shift that public perception. It is hard to argue that he has not succeeded in accomplishing that shift – at least as it applies to equity prices. Bernanke has argued that the “wealth effect” created by increasing stock prices will induce spending as the public becomes more comfortable with the trajectory of the economy.

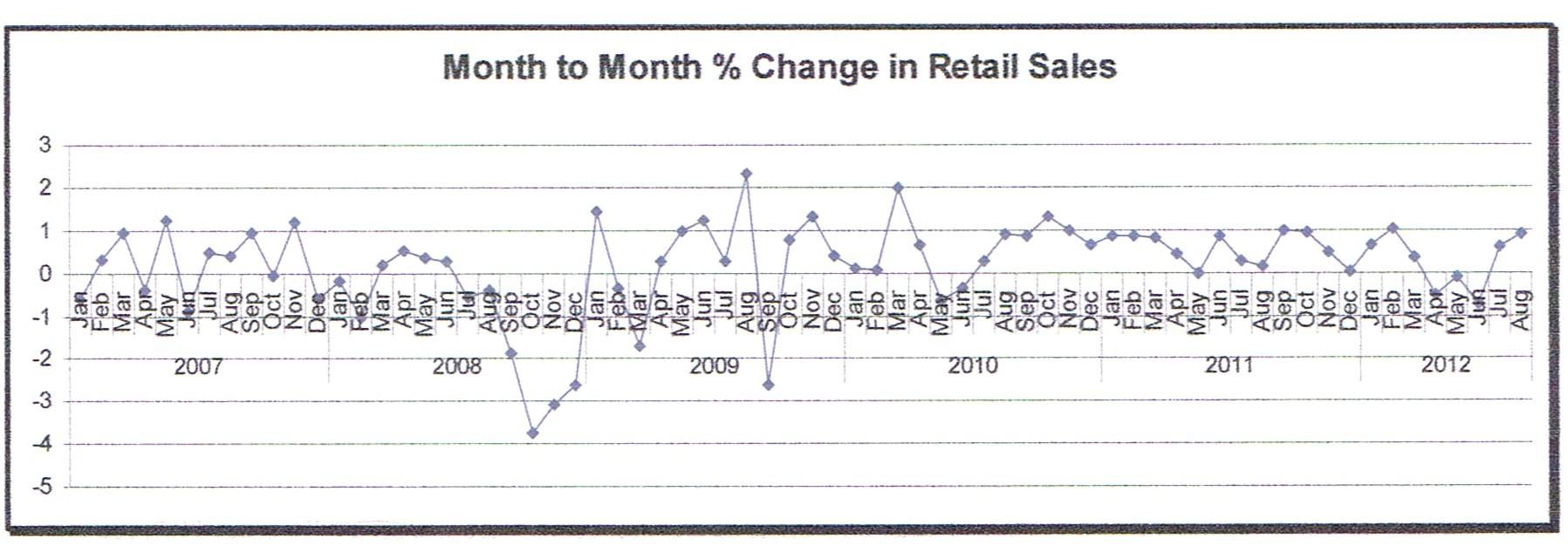

(click to enlarge)

The chart above is as good a metric as any to evaluate the impact Bernanke has had on public perception. After bottoming out in June, retail sales have indeed climbed along with the stock market.

Has Bernanke finally convinced the public that he knows what he is doing and everything will be alright? It is a little hard to say with any degree of conviction. Clearly retail sales have climbed in lock step with the stock market since the end of the 2nd quarter. The question has to be this – did retail sales lead stocks or did stocks lead retail sales?

Who in the world is currently reading this article along with you? Click here

Bernanke will tell you that it doesn’t matter as long as people are spending. That is his end goal as it will stimulate demand for goods and services and therefore induce hiring which will increase the consumer base. That increased consumer base then fuels additional demand for goods and services and we are off to the races.

I think it does matter though. If this recent improvement in spending is based on the “wealth effect” created by increased stock prices then it seems logical to conclude that stock prices must move higher still if public perception is to remain positive. It’s a tricky call and a dangerous game for the Fed to play here.

Don’t Delay!

– Go here to receive Your Daily Intelligence Report with links to the latest articles posted on munKNEE.com

– It’s FREE and includes an “easy unsubscribe feature” should you decide to do so at any time

– Join the informed! 100,000+ articles are read every month at munKNEE.com

– All articles are posted in edited form for the sake of clarity and brevity to ensure a fast and easy read

– Get newly posted articles delivered automatically to your inbox

– Sign up here

Another metric that doesn’t look as encouraging is the M2 money supply and the saving portion of M2. Since the most recent leg up in the stock market started in June, M2 has grown a modest $192 billion from $10.005 trillion to $10.197 trillion. At the same time the savings portion of this M2 increase has grown by $201 billion from $6.348 trillion to $6.549 trillion.

(click to enlarge)

The chart above shows the trend in savings relative to M2 growth since 2007. Since the recession savings has outpaced M2 growth by a significant margin. The most recent numbers – not included in the chart above – suggest that the rate of savings relative to M2 growth continues to be a problem.

Savings growth for the end of September are continuing to outpace M2 growth. There are two metrics that will produce the Fed’s desired effect:

a) A reduction in savings as the public gains confidence in the economic recovery.

A 30% reduction in savings would equal almost $2 trillion. That number is equal to 12.5% of current GDP. If these funds came out of savings and were used to purchase goods and services it would translate to a 12.5% jump in nominal GDP. If this were to occur then retail sales would clearly be taking the lead and stock prices would follow.

b) A release of liquidity that is currently “trapped” in the banking system. If the publics confidence is rejuvenated and they resume borrowing and banks resume lending then a rapid expansion of M2 will be the result.

Inflation will once again take the forefront in economic discussions and an explosion in equity prices will certainly occur as the public suddenly shifts focus and begins to borrow assuming that it makes sense to borrow at historically low rates in light of a rapid increase in the price of everything. That is the first scenario above – the one the Fed wants to see happen.

Scenario #2: Fundamentals

The fundamentals present a much more pessimistic picture. Keep in mind they don’t matter at all if scenario one above materializes as Bernanke and the Fed hope. The release of liquidity from the banking system and the reduction in savings to pre-recession levels will offset the fundamentals. The big question is again one of public perception.

As we all know, unemployment and GDP growth have been particularly troublesome problems for policy makers on the fiscal and monetary front. In an effort to stave off the terrible effects of record high unemployment the federal government has incurred massive debts.

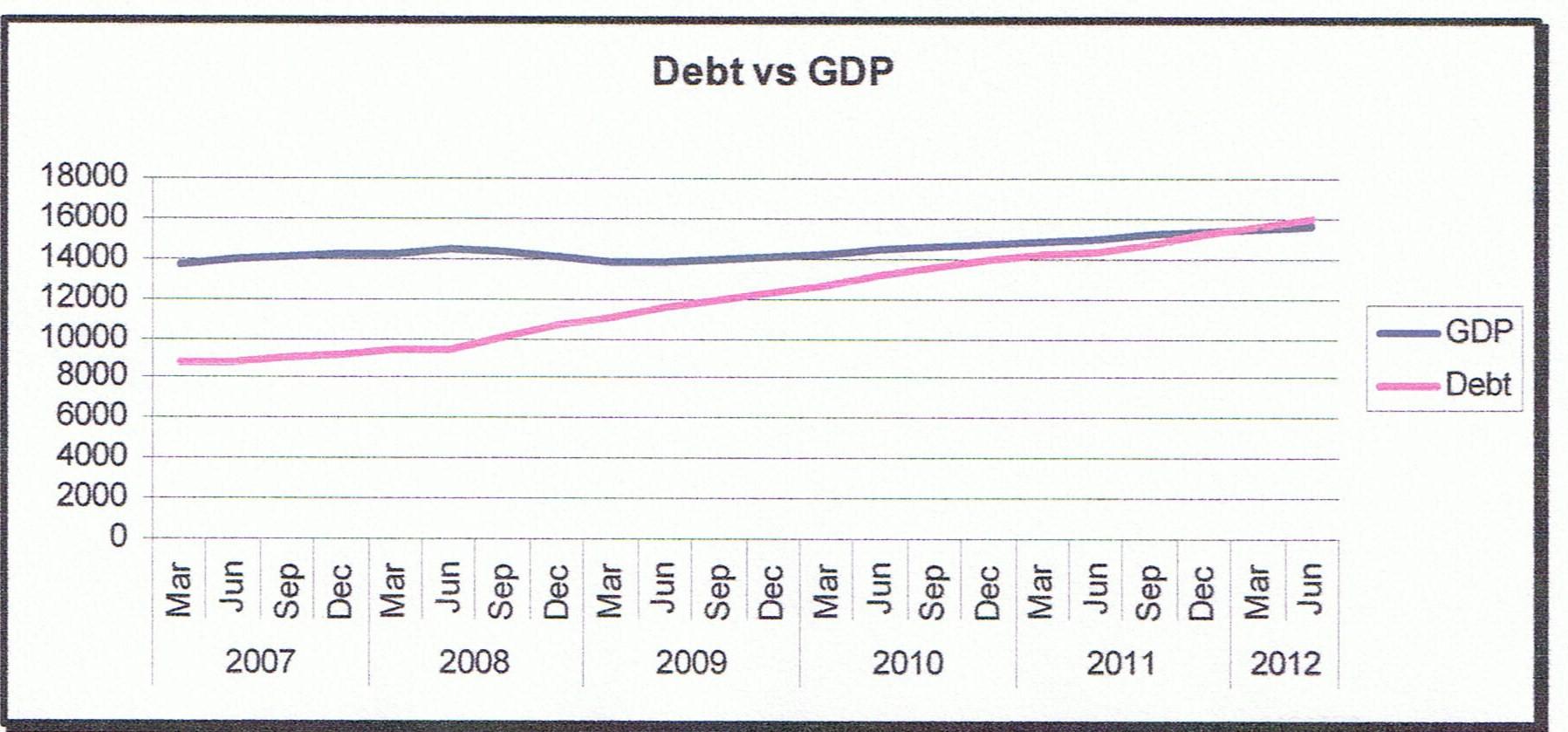

(click to enlarge)

Our national debt has risen by 80% from January of 2007 through September of 2012. Consider the magnitude of this massive increase in debt. In the last 5 years we have incurred new debt almost equal to the debt incurred by all other administrations combined.

Why have we chosen to undertake such massive borrowings? The answer is clear – someone had to spend money to support GDP and prevent an economic collapse that would have otherwise sent us into a depression. Since the public – including individuals and corporations – refused to spend the federal government reasoned that they must do so to support GDP.

Clearly the federal government has succeeded in preventing a depression as the massive infusion of cash into the economy has propped up GDP. On the other hand the public has refused to jump on board and join in the spending spree. This has to be disconcerting to those who define and implement fiscal and monetary policy.

(click to enlarge)

A look at the chart above and we can see the problem we have created. To date we have managed to remain relatively flat on key metrics. GDP stabilized following the Fed’s QE 1 initiative. Unemployment has also stabilized and actually improved slightly but not much. Without an increase in employment GDP is likely to remain flat at best.

The Fiscal Cliff Issue

The two charts above set up the “fiscal cliff” issue. The problem is a simple one – we have reached the tipping point where any further stimulus fueled solely by public debt is unsustainable. The question one must ask is this – will our short term cure for the patient end up killing the patient in the end?

In the “Ben Bernanke” scenario above I outlined how public confidence can fuel an economic recovery that will make our “fiscal cliff” issue irrelevant. A reduction in savings of 30% to pre-recession levels will fuel a massive explosion in GDP if that money is spent purchasing goods and services. The impact of that spending would be a $2 trillion infusion into the economy and a GDP increase of 12.5%.

The result would be an increase in the tax payer base as companies scrambled to hire workers to meet this renewed demand. In other words the “receipts” side of the deficit spending equation would improve dramatically. At the same time the employment picture would benefit the spending side of the equation and the overall result would be a dramatic shift back toward a balanced budget.

Time is running out though and there is no question we cannot continue to prop up an otherwise flat economy with additional debt. The next administration must take the initiative to reduce deficit spending. That means that we will reverse course in 2013. Rather than inject public money into the economy we will begin to pull it back out of the economy.

The problem is that the proposed spending cuts and tax increases that will go into effect without congressional action will result in a reduction of $600 billion in the deficit but that also equates to a contraction in GDP roughly equal to the same amount. Again, that is not a significant economic impact at all if the public buys into the economic recovery argument and assumes their role in the economic recovery. On the other hand, it will contract GDP growth – which is currently at 1.3% – by about 3%. A 3% contraction in GDP takes GDP into the minus column and a recession.

Predicting the public response going forward

So there you have it in simplistic terms. In the end, “we the people” control our own destiny. We are always quick to condemn our fiscal and monetary leaders but the truth is we drive the economy. If we choose to remain fearful and hoard cash then scenario two will be the result. If we do an about face and begin to spend with renewed abandon then scenario one will be the result.

We of course, cannot be expected to drop our guard and start spending absent leadership that we have confidence in and that is probably going to be the deciding factor here. Personally, I am not going to be inclined to go on a spending binge until I am convinced that we are on the right path.

There can be no question that the “wealth effect” has played a role in the recent climb to post recession highs in the stock market. My guess is that this trend in stocks must continue to keep the free spending attitude that has prevailed through the summer months intact.

We have a – “which come first, the chicken or the egg” – dilemma here. The question is can the “Bernanke bulls” add to the impressive gains that we have seen in the stock market in the last year? Consider we are up 30% or more from 2011 lows and that move is predicated entirely on the Fed’s QE programs.

QE has not worked to date. We have gone through 2 rounds of QE and are now embarking on a third. So far the public has failed to bite on the Fed’s bait. Inflation has not occurred and in fact disinflation has been the reality for the last 12 months. GDP growth has remained flat. Unemployment numbers have improved slightly but some argue that the demographic make-up has shifted and the real unemployment situation is unchanged.

Additionally – and perhaps most telling – is the fact that the rather modest growth in M2 has been outpaced by the dramatic growth in savings. We are still a nation of people who are hesitant to spend. We also know that the “fiscal cliff” issues must be dealt with. Furthermore, we are aware of the dependency we have on the other major economies around the world and the picture doesn’t look to rosy on that front…

Conclusion

The truth is that the market will move in the direction that corresponds with the public’s perception. If the public believes we are on the verge of economic recovery and begins to spend we will we go higher. If the public remains fearful and continues to save we move lower. It is just that simple.

My thinking is that a collective shift in the thinking of the masses is not an easy thing to accomplish. We do tend to prefer the status quo even if the status quo is not so good. We have taken some comfort in our prudent nature since the recession and I suspect we will continue with that course. That suggests a market that is on the verge of moving lower….

* Source of original article: http://seekingalpha.com/article/928771-can-perception-continue-to-trump-fact

Editor’s Note: The above post may have been edited ([ ]), abridged (…), and reformatted (including the title, some sub-titles and bold/italics emphases) for the sake of clarity and brevity to ensure a fast and easy read. The article’s views and conclusions are unaltered and no personal comments have been included to maintain the integrity of the original article.

Related Articles:

1. QEunlimited is NOT Going to Save the U.S. Economy – Period!

With the pop from the USFed’s latest attempt at financial shock and awe already seeping from lackluster markets, and the teleprompter news networks losing steam over their promotion of the same, it is time to take a look back at the decisions made on 9/13/2012 and set the record straight on some things.

2. QE 3 Will Actually SUPPRESS the Economy! Here’s Why

The Fed professes that QE 3 or as I call it, QE Infinity (QEI), will create jobs but I am not sure how they can expect anybody to buy their rationale. As we know, QE 1 and QE 2 did very little in the way of creating jobs. Might the Fed realize that QE Infinity could actually be counter-productive to economic growth?

3. QE3 Will Be More Effective Than Previous Versions – Here’s Why

The analysis of current Fed policy has included the usual parade of mistaken pundits [whose views have] been obscured by… an agenda based upon their politics or their business models [and then there]…are the correct answers which are pretty obvious to anyone with any training in economics. Here is that reality. Words: 734

4. How Quantitative Easing Supposedly Works in 1 Simple Chart

A recent short Wall Street Journal article included a chart that simplistically shows what is said to be the essence of the economic thrust of quantitative easing. The chart, reproduced here, is worth studying and thinking about.

5. This Is What “Falling Off The Fiscal Cliff” Really Means – and It is DIRE!

We all know that high debt is a growth killer and, at the moment, the U.S. has a budget deficit of about $1 trillion. That’s a very big number…The question is, at what point do countries have to deal with high debt levels? How high do debt levels have to be before one has to deal with the problem by lowering budget deficits? Also, what are the consequences of such debt and budget reductions? Words: 500

The outcome of the election of 2012 will [only] determine the rate of speed at which we approach the [financial] cliff [because] neither political alternative is willing to change course, to steer away from the cliff. The cliff is so high that whether we go over it at 200 mph (Obama) or whether we merely slip over the edge (Romney), the end result is the same — fatal for the economy and perhaps our entire political system. It is the fall that will kill us. [This article explains why that is going to be the case.] Words: 1135

7. Fiscal Tightening in 2013 and Its Economic Consequences

Under current law, a sharp reduction in the federal budget deficit between 2012 and 2013 will cause the economy to contract but, the Congressional Budget Off ice projects, will also put federal debt on a path more likely to be sustainable over time. To illustrate the eff ects of fiscal tightening, CBO compared its projections under current law (the “baseline” projections) with projections under an alternative set of policies — two scenarios in a broad spectrum of choices – in the infographic below.

8. The Fiscal Cliff: Everything You Need To Know About It & Its Implications

The U.S. federal government is scheduled to implement a fiscal tightening of unprecedented severity (approx. 5% of GDP) at the start of 2013. The last time a tightening of such proportions occurred (3% of GDP in 1969) it presaged a recession. Thus, unless mitigated by an act of Congress, we expect the fiscal cliff would lead the U.S. into a recession in 2013. Below, in 26 charts, we examine all aspects of the impending crisis to gauge its potential impact on the credit markets and, by extension, our strategic investment recommendations.

This post shows JPMorgan’s estimated probabilities on four different fiscal cliff outcomes, conditional on who wins the presidential election in November.

10. The Fiscal Cliff: What We Think Will Happen and What Investors Should Do

Unless the government acts quickly, it is probable that the term “fiscal cliff” will become a household phrase over the next few months. Unfortunately, this is reminiscent of the budget ceiling crisis about a year ago. In this report we will explain what the cliff is, discuss the worst case scenario, and determine what, if anything, you should do about it. Words: 1436

11. What’s Coming: A “Fiscal Meat Grinder,” A “Fiscal Cliff” and a Potential “Major Market Meltdown”!

The International Monetary Fund, the U.S. Congressional Budget Office, the National Association of Manufacturers and many other authorities are now warning that with the largest tax increase in U.S. history — plus the largest government spending cuts our nation has ever seen – one of the deadliest financial crises in U.S. history is set to strike the U.S. economy beginning this coming New Year’s Day. Barring a miracle in Washington….. Words: 1028