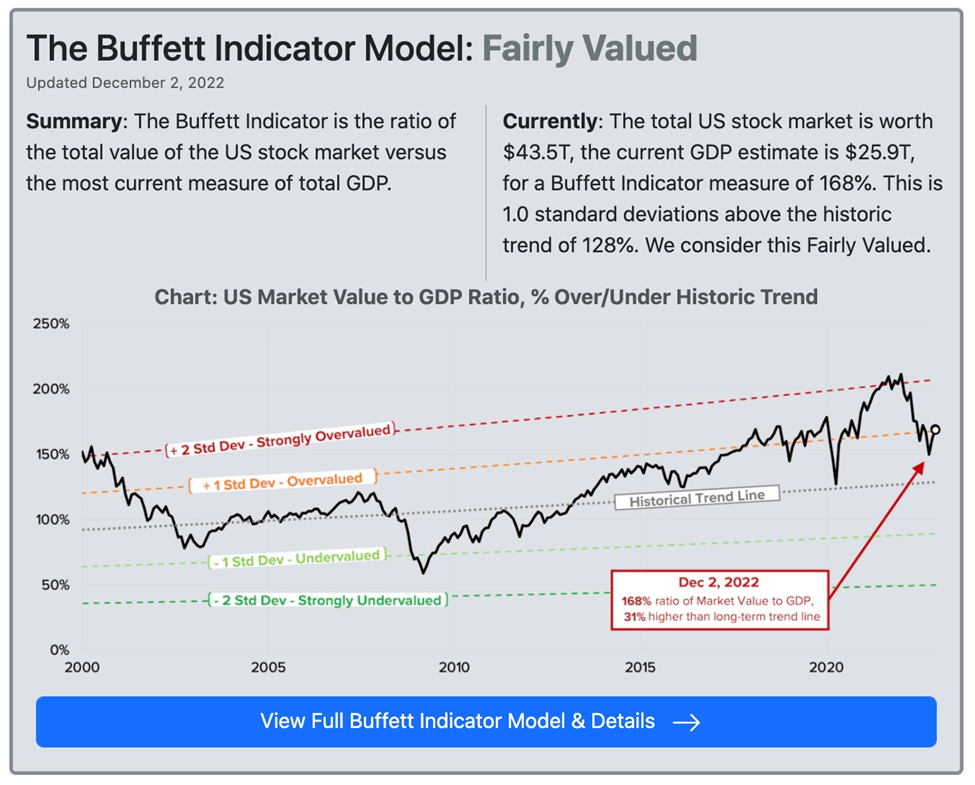

With the Buffett Indicator pointing to a “lost decade” of negative returns, and Nouriel Roubini…predicting in an interview with Bloomberg this past September that the S&P 500 could experience a severe (-40%), long and ugly recession the obvious question is how to batten down the hatches and survive the coming storm. The answer is “real assets”, including commodities, versus “financial assets”.

Source: currentmarketvaluation.com

Source: currentmarketvaluation.com

By* Lorimer Wilson, Managing Editor of munKNEE.com – Your KEY to Making Money. Here’s why.

Real vs financial assets

First we need to define our terms.

Investopedia defines real assets as physical assets that have an intrinsic worth due to their substance and properties. They include commodities, natural resources, equipment and real estate. Real assets provide portfolio diversification as they often move in the opposite direction as financial assets, which include stocks, bonds, mutual funds, savings and cash.

The two classes can overlap, for example commodity futures, exchange-traded funds (ETFs) and real estate investment trusts (REITs) are financial assets whose value depends on the underlying real assets.

The disadvantage of real assets is they are less liquid than financial assets. They take longer to sell and have higher transaction fees, carrying costs and storage costs. (e.g. bullion)

However, their main advantage over financial assets is they are more stable. Inflation, changes in currency values, and other macro-economic factors affect real assets less than financial assets. This makes them good investments during periods of high inflation. In addition, cash flow from real assets like real estate can provide predictable income streams for investors, states Investopedia.

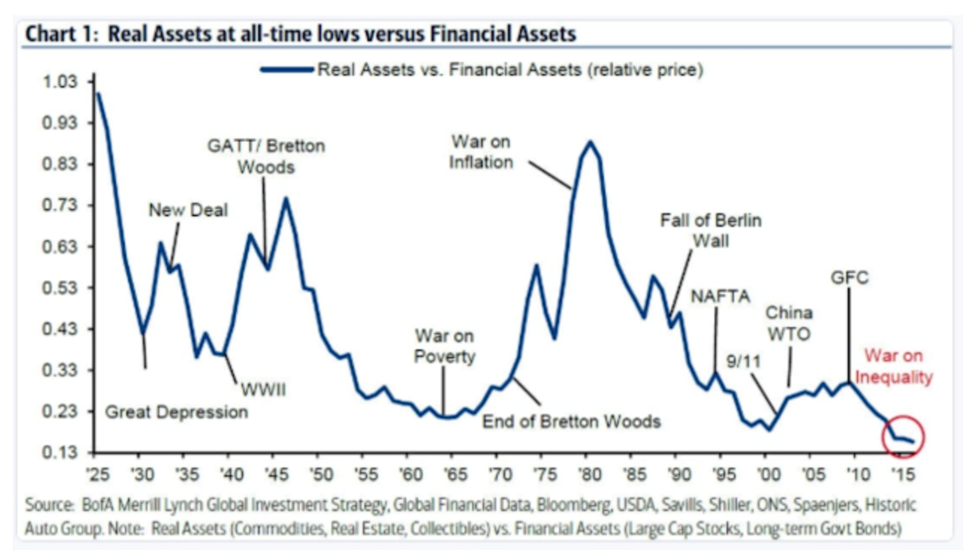

The chart below, via Harvest, graphs the price of real assets versus financial assets over time. We find that real assets explode in relative value during periods of inflation and war. This makes sense because more resources are needed, or commodities are scarce, relative to money. When the Harvest article was written in 2018, the author found that The flow of money has moved to financial assets especially those that are related to technologies that do not need capital.

The chart below shows a wide dispersion between asset price inflation and real economy inflation. While real economy prices barely moved from 2009-18, asset prices exploded. Harvest states: The capital gains, dividends, or carry has favored these assets over investing in the real economy. Excess cash has used financial assets as a store of value. This is the collateral used for a levered economy.

Undervalued commodities

Commodities protect investments from rising prices and currency debasement, making them a good place to park cash during inflationary periods…

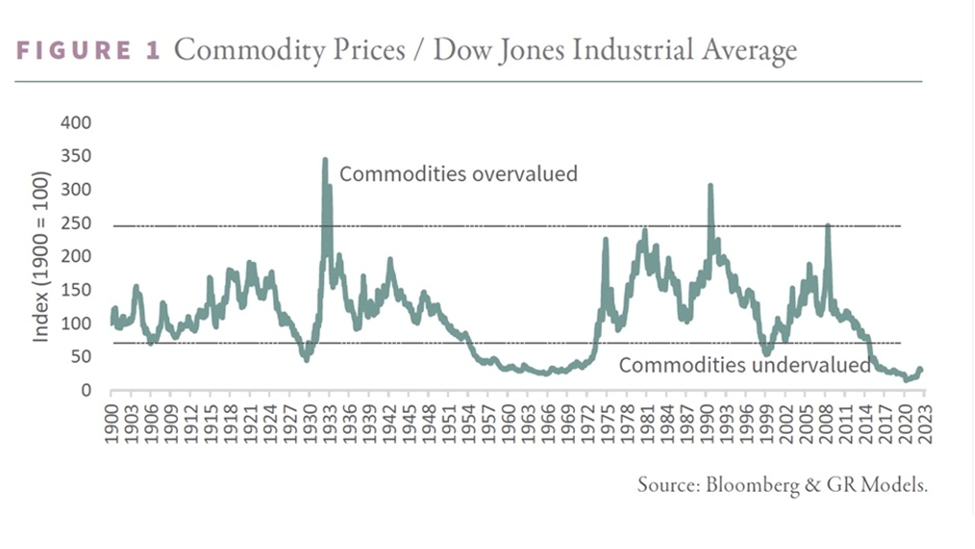

However, when investing in natural resource equities, the commodity capital cycle is more important than the broader economic cycle. I found the chart below in a recent report from Goehring & Rozencwajg, the Wall Street natural resource investment firm.

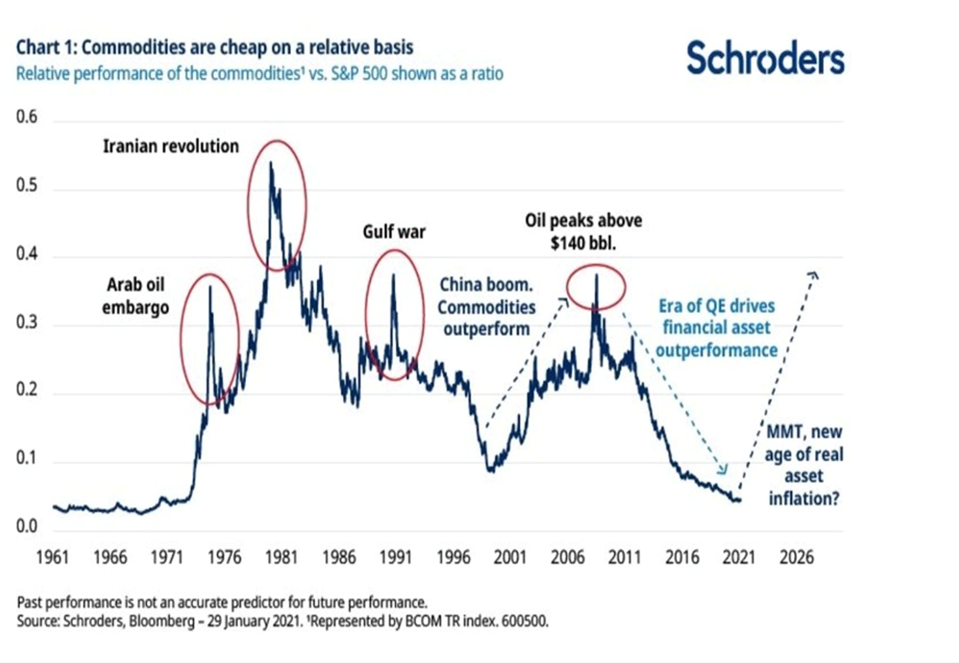

It shows the relationship between the Dow Jones Industrial Average and a commodity index going back several decades. It clearly indicates periods when commodities are extremely undervalued or overvalued — compared to the Dow. In places where the green line falls under 75, commodities are cheap relative to financial assets. These periods typically represent bear markets for commodities. The chart shows the most undervalued years for commodities were 1929, 1969, 1999 and 2020.

The following chart by Schroders is similar to G&R’s but tags key events at points in time when commodities have been overvalued.

What makes commodities cheap, relative to financial assets? According to G&R, it has to do with natural resource capital spending:

A commodity price cycle usually follows a typical path. The industry might enjoy a period of very high energy or metal prices. Given their fixed cost base, the higher commodity prices fall directly to the bottom line resulting in a period of super-normal profits. High returns attract new capital and before long the industry begins a new cycle of exploration and development. Over time, increased spending leads to new supply which eventually outpaces demand growth and ushers in a period of commodity surplus. Prices fall, causing projects that were underwritten at higher prices to become impaired and written off. Often, another industry or investment strategy falls into favor around this time and investors rush to reallocate capital towards hot new speculative areas, leaving the resource industry even more capital starved. As depletion takes hold, supply falters, demand grows, and inventory gluts eventually get worked off. The stage is set for the next bullish cycle to start.

G&R’s advice is to buy resource stocks when commodities are cheap, and during bottoms in the natural resource capital investment cycle.

The key point is that even if we were to go into another recession, it doesn’t mean that commodity prices will fall in lockstep, as they did in 2008. In fact, they (and resource equities) are likely to hold their own and do quite well, because unlike in 2008, commodities are undervalued, shown on the chart as the green line below 75. (in 2008 the Commodity Prices/ Dow Jones Industrial Average was about 300, well into the “Commodities overvalued” range).

In terms of G&R’s commodity capital cycle described above, we are currently in the stage of depletion, when supply falters, demand grows, and inventory gluts get worked off. The stage is, imo, set for the next bullish cycle to start.

In their report, G&R maintain that The radical undervaluation of commodities and commodity-related equities is greater now than it was back in 1929, and the level of capital starvation is just as great. History tells us that commodities could again be an excellent place to seek high returns, even if the 2020s experience a period of economic turmoil as severe as the Great Depression — a scenario we consider unlikely.

Under-investment

I’ll say more about this “capital starvation” because it’s key to understanding what is happening with commodities right now.

As a result of the bear market in commodities from 2010-20, capital spending for the extractive industries — mining and oil and gas — has been severely curtailed. For example in the energy sector, capital spending in the S&P 500 has plummeted from $320 billion per year to less than $100B currently.

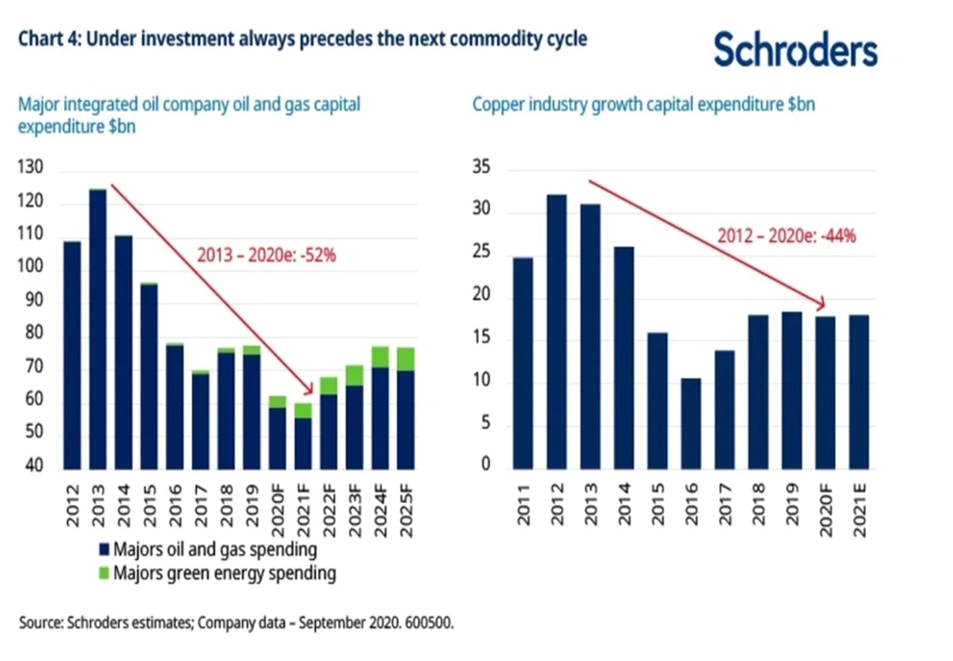

Another source found that capex in oil and gas and mining has fallen by about 40% since 2011. The 2021 article by Schroders notes that under-investment always precedes the next commodity cycle, with the chart below showing that capital investments in major integrated oil and gas companies declined by 52% between 2013 and 2020, and capex in the copper industry dropped by 44% between 2012 and 2020.

(The latter aligns with our research. As previously reported, global copper mine production will drop from the current 20Mt to below 12Mt by 2034, resulting in a supply shortfall of 15Mt. By then, over 200 copper mines are expected to run out of ore, with not enough new mines in the pipeline to take their place. S&P Global estimates that new copper discoveries have fallen by 80% since 2010.)

Conclusion

Inflation, changes in currency values, and other macro-economic factors affect real assets less than financial assets. This makes them good investments during periods of high inflation, like currently…[Indeed,] G&R’s Commodity Prices/ Dow Jones Industrial Average chart [Figure 1 above] shows there hasn’t been a better setup for commodities than now, over a time frame spanning 120 years…