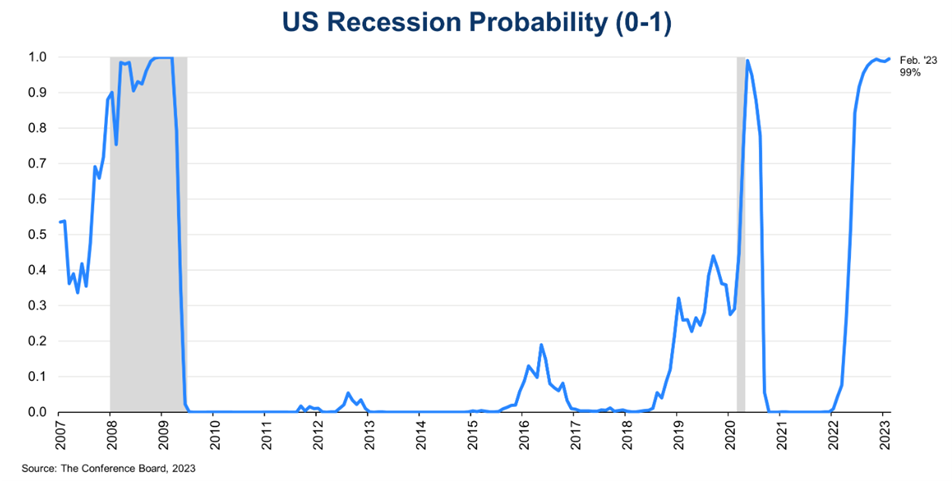

There’s a 99% chance of a recession within the next 12 months and this places gold, which is as heralded the best safeguard against economic turmoil, in the spotlight for at least this year and in 2024. In addition, this article highlights four further reasons why a bullish outlook for precious metals remains intact over a longer horizon.

This article is an edited and revised version of the original by Richard Mills and posted here by Lorimer Wilson, Managing Editor of munKNEE.com, Your KEY To Making Money!

- Central Bank Behaviour

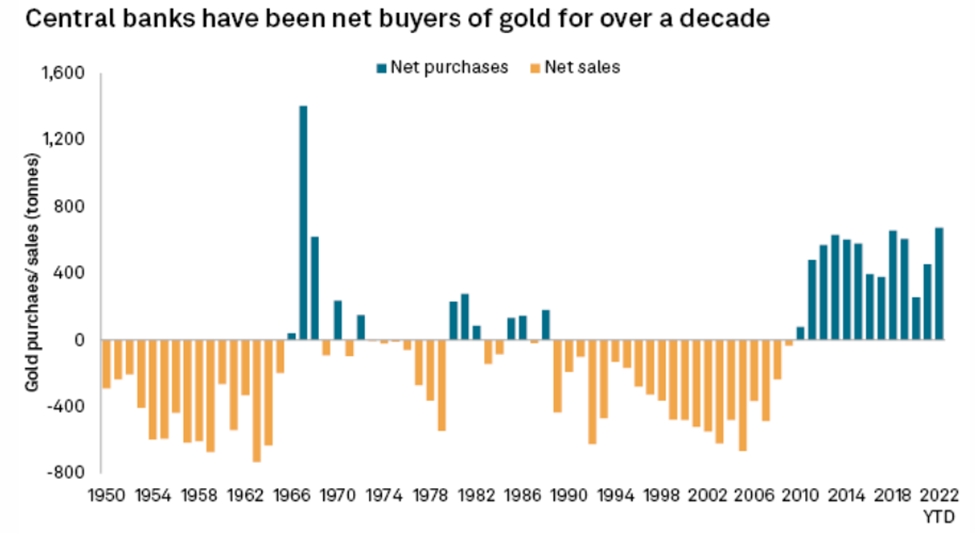

What’s keeping gold in a bull market is a robust demand for the metal, led by an unprecedented level of buying from central banks…Bloomberg previously reported that banks have been buying the most gold since the United States abandoned the gold standard in 1971 and, as of today, central banks are enjoying their longest period of gold buying, which represents a dramatic shift in attitude from the 1990s and early 2000s.

…Commenting on this recent trend, the WGC said it expects net central bank gold buying to remain robust through 2023 given the better-than-expected Q1 data, especially as emerging market banks remain relatively under-allocated to gold. The increased level of central bank buying, according to Wall Street research firm Goehring & Rozencwajg, brings gold towards a “new phase” of the bull market. “It probably started in the third and fourth quarter of last year, and it really revolves around central banks’ behavior as much as anything else. I think it’s going to propel gold much much higher in this leg of the bull market,” founding partner Adam Rozencwajg said in a recent interview with Investing News Network.

- Geopolitical Dynamics

Behind the central banks’ gold buying are likely the escalating geopolitical factors that prompted them to add gold bullion to their reserves. The most obvious one is Russia’s invasion of Ukraine and its recent political turmoil, which are lowering the overall risk appetite and igniting the safe-haven gold trade. In addition, the sanctions imposed on Russia could have a wider impact on international trade, in particular what it means for the status of the US dollar.

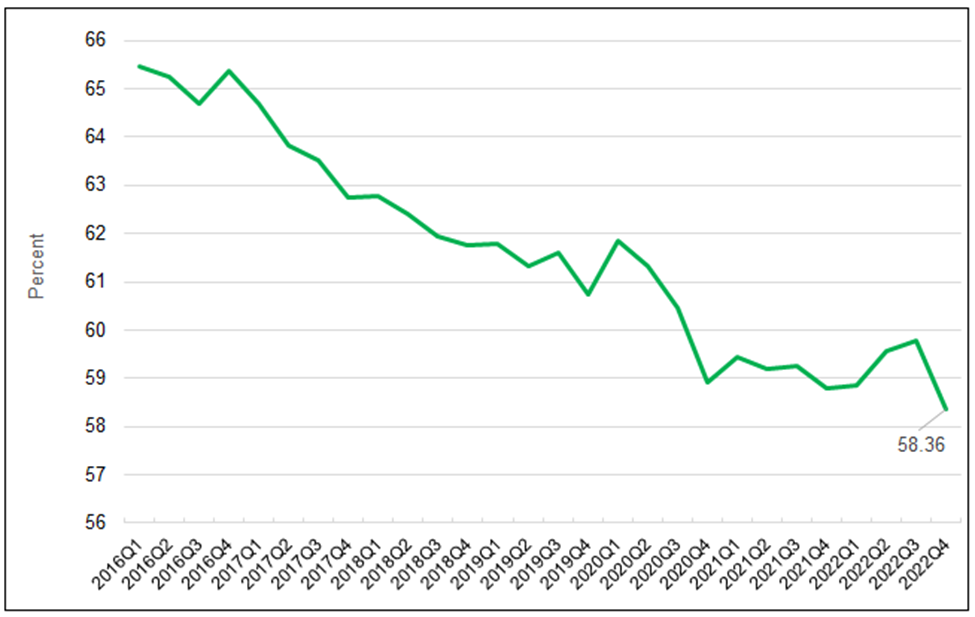

Paul Wong, market strategist at Sprott, recently stated in a report that central banks have ramped up purchases in preparation for a “de-dollarization”, considering gold’s emerging role as a neutral reserve asset. “Deglobalization is accelerating the transition to a more multipolar world, making the question of global reserve currency allocations more relevant,” Wong wrote. Since its peak in the late 1990s, the USD has slowly lost market share as a reserve currency (see figure below).

History has shown that currency predominance in international trade and reserves follows economic, cultural and military dominance. According to the Sprott strategist, “currency reallocations could move more quickly and significantly than anticipated if reserve managers increase allocations to other currencies or reserve-neutral assets.” Currently, the risk is minor and gradual, says Wong, but China has the potential to gain share as its reserve share. What’s interesting is that China has been one of the most prominent buyers of gold in recent times.

Counterparty risk — the potential for one party in a financial transaction to default on its contractual obligations — is also a major influence on central bank behaviour. As gold becomes increasingly involved in settling multicurrency energy and commodity trades — particularly in China-related trade with oil producers — the links between gold, other commodities and counterparty risks may intensify, Wong said.

Whilst on the topic of currencies, the greenback, an alternative safe-haven asset to bullion, is said to be entering a bear market. “Though there have been periods whereby both the dollar and gold appreciated or depreciated in tandem, generally, the latter’s performance is superior during periods of a weak US dollar,” Christopher Yates, equity analyst at Sunbird Portfolios, recently wrote.

Previously, we’ve theorized that central banks are stockpiling gold for this purpose, and more. One possibility is a “gold revaluation” to cover the massive amount of debt they have accrued over the years. Another, albeit more specific to the Eurozone region, is the idea of a new Gold Standard.

- Tight Physical Market

There’s no denying that central bank action could help elevate gold demand, and prices, for at least the short term. Also contributing to the gold bull market is the tightness in the physical market.

Yates’ analysis of the shape (i.e. structure) of the gold futures curve reveals that there remains a small level of backwardation at the front end of the curve, which is not a common occurrence within the gold or silver markets. So long as this remains, one would suspect there is likely a solid price floor for precious metals, he added. We also need to consider whether an increased number of physical gold buyers (i.e. central banks) would cause market-wide supply shortages, and hence drive up prices.

The WGC estimates that global gold supply grew by 1% year-on-year to 1,174 tonnes in the first quarter of 2023, driven by a marginal 2% growth in mine production and a 5% uptick in recycling. However, demand is also likely to trend up through the rest of the year, and so it remains to be seen whether the supply growth would be sufficient to avoid a market deficit.

For silver, its sister metal, the market has already sunk into a prolonged supply shortage that could take years to recover from. Latest data from the Silver Institute reveals that annual silver demand also surged by 18% to a record high 1.24 billion ounces against a stagnant supply in 2022. This resulted in a second straight year of undersupply at 237.7 million ounces, which the Institute says is “possibly the most significant deficit on record.”

In 2023, we are most likely going to see a repeat of last year, according to the Institute, which expects the market deficit to remain high at 142.1 million ounces on the back of solid demand and a sustained supply shortage would keep the precious metals market in bull territory for much longer, and so long as demand doesn’t wane, that’s where gold and silver will end up.

- Market Risks

Also playing into gold bulls’ hands is a confluence of market factors that are causing further stress on the global economy, cementing the appeal of safe havens.

- First there is the well-documented high inflation, which is often hedged against by buying gold. While price level increases have begun to slow in some places, including the United States, the underlying inflation figures remain sticky…

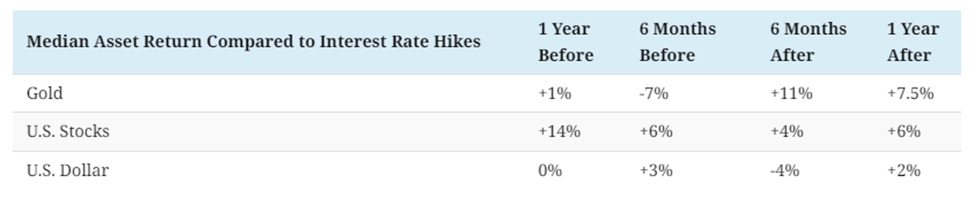

- …Interest rates are also offering more incentives to turn to gold. This is because as rates rise during tightening cycles, holding onto and lending out cash becomes more profitable, often resulting in investors de-risking by selling assets like stocks. During these times, investors also seek out uncorrelated assets that are uniquely connected to these macroeconomic factors, often turning to gold. While gold underperforms compared to stocks and the US dollar leading up to rate hikes, past tightening cycles saw gold hit new all-time highs in the 2000s (see graphic below).

What rising interest rates also can do is exacerbate the already problematic US fiscal deficit, which is expected to reach approximately $1.1 trillion in the second half of 2023.

An additional $400-$500 billion will be needed to rebuild the Treasury General Account (used to pay the country’s obligations), and $540 billion will be required for the Fed’s quantitative tightening program. This would result in a significant net US Treasury issuance of approximately $2 trillion during the second half of 2023, according to Sprott. However, the U.S. could be hard-pressed in finding sufficient global demand to absorb this level of issuance, given its already high debt level and budget deficits alongside insufficient foreign central bank buying. This could lead to a dysfunctional Treasury market, characterized by asset price declines, rising yields and, possibly, a credit/capital crunch. Significant liquidity tightening would increase yields and pressure on the US banking system and financial assets, and thus, higher credit risks.

These risk elements listed above (liquidity risk, credit stress, credit crunch, US Treasury market dysfunction, bond volatility, inflation and regional banking stress) have been historically bullish for gold prices, Sprott says.

- Recession Signs

…Recent downside surprises in U.S. economic data have lifted the chances of a recession over the next 12 months, with safe-haven flows providing somewhat of a cushion for gold, Yeap Jun Rong, a market analyst at IG, said in a recent CNBC interview.