While the hot air was let out of the housing bubble in the U.S. between 2007 and 2011, in Canada, after a minor ripple between 2008 and 2009, home prices continued soaring – to this very day. In August, they rose another 0.8%. Over the last 14 years, prices have increased by 150%, twice as fast as in the U.S…[and] far outpacing household incomes. Any increase in interest rates would prick the bubble, and its implosion would trigger all sorts of mayhem. Indeed, the Canadian government is very concerned that such an event would be a significant risk to the “stability of the financial system”.

in Canada, after a minor ripple between 2008 and 2009, home prices continued soaring – to this very day. In August, they rose another 0.8%. Over the last 14 years, prices have increased by 150%, twice as fast as in the U.S…[and] far outpacing household incomes. Any increase in interest rates would prick the bubble, and its implosion would trigger all sorts of mayhem. Indeed, the Canadian government is very concerned that such an event would be a significant risk to the “stability of the financial system”.

The above introductory comments are edited excerpts from an article* by Wolf Richter (wolfstreet.com) entitled Is Canada Next? Housing Bubble Threatens ‘Financial Stability’.

Wolf goes on to say in further edited excerpts:

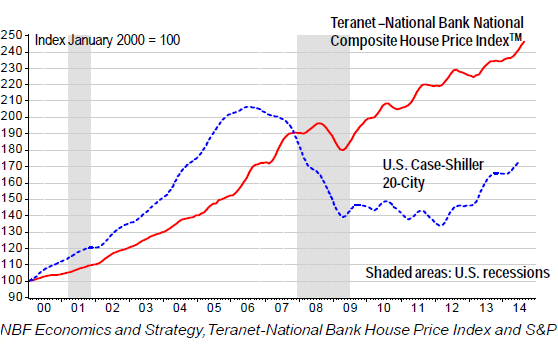

Home prices in Canada rose more moderately than in the U.S. during the crazy go-go years from 2000 until the financial crisis: in the U.S. they more than doubled in that period, according to the CaseShiller Index, while they rose “only” about 70% in Canada, based on the Teranet–National Bank National Composite House Price Index.

House Price Index UP Dramatically

While the hot air was let out of the housing bubble in the U.S. between 2007 and 2011, in Canada, after a minor ripple between 2008 and 2009, home prices continued soaring – to this very day [as can be seen in the chart below]. In August, they rose another 0.8%. Over the last 14 years, prices have increased by 150%, twice as fast as in the U.S..

…In a speech to the Chamber of Commerce and Industry of Saguenay, Quebec, Bank of Canada Deputy Governor Agathe Côté has weighed in on the housing bubble discussing. among other things, the four key responsibilities of the BOC – monetary policy, the financial system, the currency, and funds management.

The housing bubble falls under the key responsibility of managing the financial system, or more precisely under the objective of promoting its “stability and efficiency.” As part of its Financial System Review, the BOC “assesses vulnerabilities and risks.” Among the four “important risks” in her presentation:

- A sharp correction in house prices

- A sharp increase in long-term rates

If those two occurred, all heck would break lose.

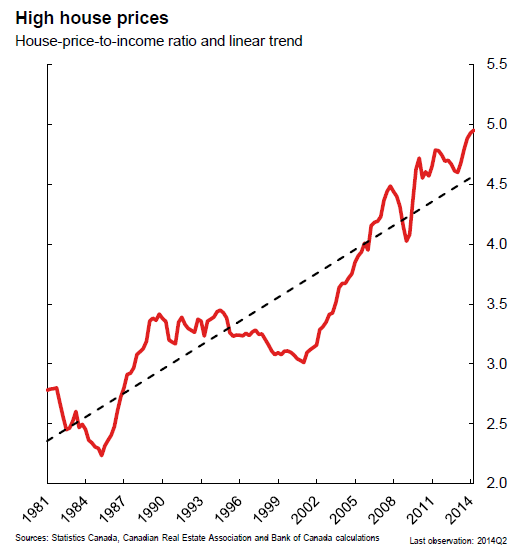

House Price-to-Income Ratio UP Dramatically

Home prices have skyrocketed, far outpacing household incomes. This chart from Côté’s presentation shows the very ugly growth of the house-price-to-disposable-income ratio. Since 2000, it has relentlessly soared, as home prices are placing an ever larger burden on household finances:

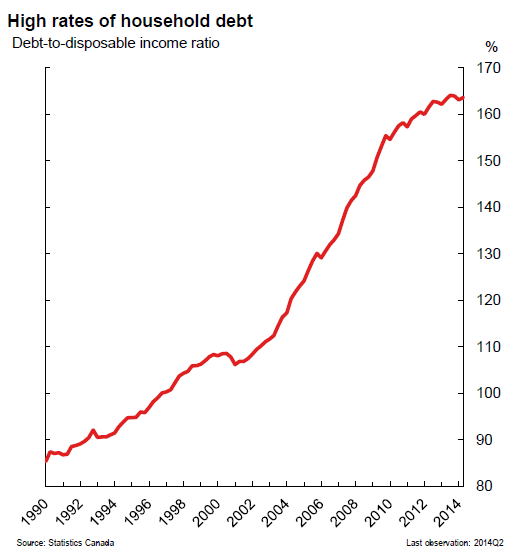

Household Debt-to-Disposable Income Ratio UP Dramatically

Given the lagging incomes, households have made up the difference with debt, and they’ve gone on a phenomenal borrowing binge, and their indebtedness in relation to their income has skyrocketed and is now hovering at near a record 164%..

The chart below shows the debt-to-disposable-income ratio, which doesn’t leave households, and by extension lenders and the entire housing industry, any room to breathe once home values begin to descend back to earth – and there’s no trace of deleveraging in sight:

Home-price bubbles are treacherous. High household debt relative to disposable income has made the market more susceptible to market stresses like unemployment or interest rate increases. Low interest rates have been heating up the market yet any raising of them would prick the bubble, and its implosion would trigger all sorts of mayhem.

Impact of Higher Interest Rates on House Prices Would Be Dramatic

Now imagine what even just slightly higher interest rates would do to households barely able to shoulder this mountain of debt, and what they would do to home prices as demand would be systematically strangled.

The federal government…[has tried to] cool down the market…[by] shortening amortization periods to 25 years from 40 years and tightening the eligibility for government-backed mortgage insurance… [in an effort to] “engineer a soft landing” [but to no avail].

Conclusion

Bubbles don’t land softly, they implode, and it’s a brutal process. The longer bubbles are maintained, the more brutal their implosion and housing bubbles are particularly vicious: they’re accompanied by a construction boom, which contributes enormously to the economy in myriad direct and indirect ways – from well-paid construction jobs to pickup truck sales.

[Canada’s federal government has good reason to be very concerned about the negative impact any pricking of the housing bubble would have on the financial stability of the country!]

Editor’s Note: The author’s views and conclusions in the above article are unaltered and no personal comments have been included to maintain the integrity of the original post. Furthermore, the views, conclusions and any recommendations offered in this article are not to be construed as an endorsement of such by the editor.

*http://wolfstreet.com/2014/10/01/is-canadas-truly-magnificent-housing-bubble-next/(Copyright © 2014 Wolf Street Corp. All Rights Reserved)

If you liked this article then “Follow the munKNEE” & get each new post via

- Our Newsletter (sample here)

- Twitter (#munknee)

Related Articles:

1. Canada’s Housing World’s Most OverValued – Where Does Your Country Rank?

Canada’s housing market is the most expensive in the world – 60% overvalued by historical standards – and one simple reason explains it. Read More »

2. Is a Real Estate Bust Coming to Canada – Finally?

The Canadian housing market is headed for a significant bust, in my view. It’s going to be a repeat of the 2008 mortgage bubble deflation. Only it’s happening to the north. People will lose a lot of money but those who understand and are properly positioned may gain fortunes. Read More »

3. Home Price Appreciation Highest In New Zealand, Canada & Australia. Where Do U.S. & U.K. Rank?

This post takes a look at the appreciation (or in some cases, depreciation) of home prices in 11 developed markets. New Zealand, Canada and Australia are in a league of their own at the top, while Germany, Ireland and Japan are at the bottom. Where are the U.S. and the U.K.? Read on! Read More »

4. Canadian Debt-to-Income Ratio Has Entered the Danger Zone! Is a Housing Crash Imminent?

The Canadian ratio of debt to income hit 163.4% in the second quarter, up from 161.7% at the end of last year, according to figures released Monday by Statistics Canada. That’s the highest ratio of debt to income ever recorded in Canada, and more inflated than the levels witnessed in the U.S. and Britain before their housing market collapses in the mid-2000s. Words: 625 Read More »

5. Canada Could Be Developing a Minsky Moment In Real Estate – Here’s Why

According to the Case-Shiller 10-City index Canadian house prices only appreciated by 84% between 1990 and 2006 compared to 181% in the U.S.. However, as U.S. prices plunged by almost 33% between the peak in April 2006 and the trough in May 2009, the chart below shows that Canadian home prices continued to rise, driven by very low interest rates and relatively benign unemployment. By July 2012, they had reached similar heights as U.S. prices before their decline and fall. I believe that house prices and consumer debt levels are overextended in Canada and that a “Minsky-moment” may be developing in Canadian credit markets. [Let me explain why I have come to that conclusion.] Words: 1892 Read More »

6. Still NO Housing Bubble in Canada – So What Will Cause Prices to Finally Correct?

Canada’s housing prices continue to escalate [there has been no housing collapse as there has been in the U.S., Spain, U.K., Australia and elsewhere over the past 4-6 years] but concern is rising as to whether they are now, finally, ‘in a bubble’ and about to correct either modestly or severely. This article discusses what would cause a change in direction in Canadian housing prices. Words: 500 Read More »

7. Are Surging Home Prices in Canada Finally Due For a Major Correction?

Given the global economic backdrop, and in particular the sharp correction in energy prices to which Canada is highly exposed, the risks of a Canadian housing correction are rising. Home prices, which corrected about 10% during the recession, have surged again, making household balance sheets look increasingly fragile. Economists are becoming concerned. [Should Canadians be worried too? Let’s review the situation.] Words: 280 Read More »

8. Will Canada Soon See a 20-30% Correction in House Prices?

Canadians are becoming increasingly vulnerable to a housing correction, exposing them to a perfect storm of high debt and falling assets, the Bank of Canada warns…suggesting that many Canadians have constructed their finances on a house of cards, with ever rising home values the key and vulnerable support. [Sound familiar?] Words: 770 Read More »

9. Housing Collapse Coming to Canada? House Price-to-Rent Ratios vs. America’s At Peak Suggest So

The ownership premium in Canada’s largest cities is unprecedented, dangerous to new buyers, and unlikely to persist – and if analogies to the U.S. situation at its peak back in 2005 are at all valid, this is bad news. [Let me explain.] Words: 430 Read More »

10. Unlike the U.S and U.K, Canada’s Home Prices Are STILL Rising!

Canada, France and Switzerland stood alone among nine markets measured in recording annual price gains, based on second-quarter data, with inflation-adjusted price increases of 5%, 5% and 4%, respectively, compared to declines of 6% in the U.S., the U.K. and Australia, 10% in Spain and 14% in Ireland. In fact, Canada’s home prices have escalated 44% since 2005 – with a high of 68% in Vancouver – and they are up 7.7% in the past 12 months! Words: 1244 Read More »