AMMO, Inc. is taking the bold step of splitting up its successful business of manufacturing, marketing and selling an array of small caliber bullets and online marketing of ammunition to increase sales, improve margins and expand its business platform and, in doing so, “significantly enhance shareholder value.” This article takes a looks at the ammunition industry, AMMO’s current place in the marketplace and its plans to take its business to the next level.

By Lorimer Wilson, Managing Editor of munKNEE.com, Your KEY To Making money!

The Global Ammunition Market

The global ammunition market size was valued at $22.35 billion in 2021 and is expected to expand at a compound annual growth rate (CAGR) of 3.2% from $22.30 billion in 2022 to $29.68 billion in 2030 due to:

- a rise in the number of terrorist activities and hostilities across the globe which is likely to increase the procurement of defense equipment by prominent militaries across the globe which accounted for a 75% share of the global revenue in 2021 and is expected to maintain its market share going forward, and

- a rising trend for sports and shooting that utilize rifles and pistols.

The small caliber segment led the market and accounted for over 50.0% share of the global revenue in 2021 attributed to a wide array of small-caliber ammunition applications including shotgun pistols, assault rifles, rifles, and revolvers. Additionally, the segment is likely to continue to witness the fastest growth of any caliber segment over the forecast period.

The rimfire segment is expected to register a CAGR of 3.1% in the forecast period owing to the increasing demand by beginners because such products have a limited recoil when they are being used and are cheaper as their thin casting with a flattened primer is easy to manufacture.

The centerfire segment led the market and accounted for over 65.0% share of the global revenue in 2021. Centerfire ammunition is usually used for rifles, shotguns, and handguns.

")

24 countries manufacture ammunition in Europe alone of which the top 5 are, in order: Germany (5 companies), the U.K. (1), France (1), Italy (2) and Belgium (1). (source)

The U.S. Ammunition Market

65 companies in the U.S. (source) manufacture ammunition – and 3 in Canada (source) – and they accounted for over 30.0% share of the global revenue in 2021 and this is expected to witness significant growth owing to high demand from the U.S.

")

The U.S. ammunition market is expected to expand at a compound annual growth rate (CAGR) of 2.8% from 2022 to 2030 due to:

- a significant increase in investments by the U.S. government for enhancements in the defense department and the homeland security department,

- a surge in sports and hunting activities with the resultant increase in the purchase of small-caliber ammunition by civilians and

- the enhancement of sales channels such as online sales

- lenient gun laws and

- an ammunition shortage caused by outsized demand, supply constraints and the war in Ukraine.

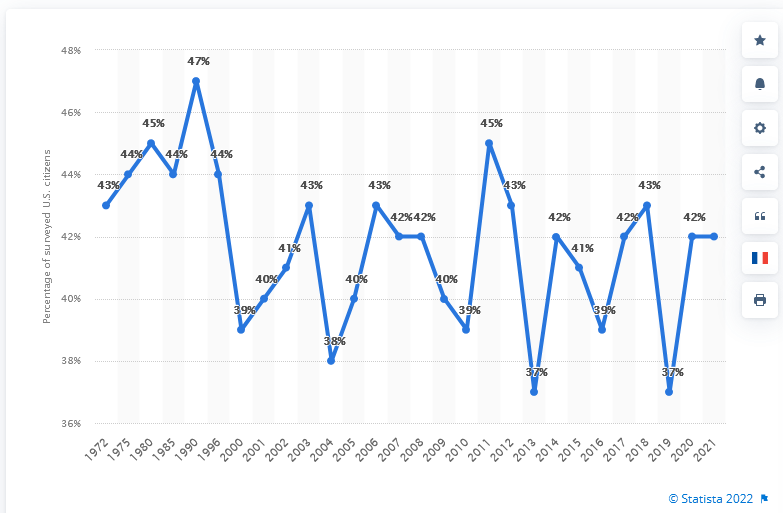

Industry Growth in the U.S.

The chart below shows that 42% of U.S. households own one or more guns

Statista

Of the major bullet manufacturers in the U.S.:

- Vista Outdoor Inc. (VSTO), with a market capitalization of $1.43B, also manufactures various other outdoor equipment,

- Olin Corporation (OLN), with a market capitalization of $6.80B, only generates 17% of revenue from its Winchester segment while

- AMMO, Inc. (POWW), with a market capitalization of only $352.1M, is more narrowly focused than its competition, with 26% of overall revenues, along with better margins, coming from its online marketplace segment and 74% from its manufacturing segment.

About AMMO, Inc.

AMMO designs and manufactures products for law enforcement, the military, sport shooting and self-defense and promotes its own branded munitions as well.

About GunBroker.com

gunbroker.com is the largest online marketplace dedicated to the buying and selling of firearms, ammunition, air guns, archery equipment, knives, swords, firearms accessories and hunting/shooting gear bearing its logo. It should be noted that it does not sell items listed by third-party sellers. The sale of such items are governed by Federal and state laws and ownership policies and regulations are followed using licensed firearms dealers as transfer agents

Company To Split Into Two Independent Public Companies

This past August 15th the company announced that it would split into two independent public companies with, upon completion of the separation, each current shareholder of AMMO owning one share of Outdoor Online, Inc., comprised of GunBroker.com and its related online businesses, and one share of Action Outdoor Sports, Inc. (AOS), the Company’s current ammunition and munition components business.

Fred Wagenhals, AMMO’s Chairman & CEO, had the following to say on the decision to split up the companies into separate entities:

- “With the supportive analysis of our trusted advisory teams, we determined that a spin-off of our ammunition/munition components business would best serve to unlock significant shareholder value.

- With the opening of AMMO’s new state-of-the-art manufacturing plant in Manitowoc, WI, and the enhancement of the integrated GunBroker.com marketplace operations following the 2021 acquisition, the management team, Board and our advisors believe the time is right to deploy this exciting strategy.”

The AOS corporate operations will remain headquartered in Scottsdale, Ariz., with manufacturing operations based in Manitowoc, Wisc.

AMMO expects the transaction will be completed in the 2023 calendar year, subject to final approval by the Company’s Board of Directors, a Form 10 registration statement being declared effective by the U.S. Securities and Exchange Commission, regulatory approvals and satisfaction of other standard and necessary terms and conditions but gives no assurance that the transaction will be consummated or as concerns the ultimate timing of the proposed transaction.

Strategic Benefits to Spin-Off

As management sees it there are a number of compelling reasons supporting the separation of these two business units. Each company:

- Will be better situated to be appropriately valued by the market, i.e. better positioned to enhance shareholder value.

- Will be better able to facilitate the enhancement and expansion of the brand strengths developed in both separate operational units, thus further supporting increased enterprise and therefore shareholder value.

- Will be better positioned to refine and focus capital allocation strategies moving forward.

- AOS will be able to build upon AMMO’s well-established track record as an attractive acquirer through enhanced M&A work in the outdoor recreation marketplace, allowing it to secure best-in-class partnerships with other manufacturers.

- Outdoor Online will be better positioned to focus on continuing the work designed to leverage its leading marketplace, while focusing on potential accretive M&A opportunities specific to its space and market.

- Will be better able to attract and retain the top industry talent best situated for each operation’s separate operational and financial objectives.

- Will be in a better position to support the specific operational needs and growth drivers of each separate company.

- Will enable financial and human capital resources to be deployed in a more focused manner to better support the specific operational needs and growth drivers of each separate company.

- Will be able to enhance support of AMMO’s growing base of international customers (commercial and governmental).

Q1, 2023, Financial Results vs. Q4, 2022

Based on AMMO, Inc.’s latest quarterly financial results the company is clearly in growth mode with positive net operating cash flow, and positive net income after extraordinary expenditures.

Q1 of 2023 saw the following changes to its financial metrics as compared to Q4 of 2022:

- Net Revenue Growth: -13.3% to $60.8M in Q1; +285% in FY2022

- Net Income Margin Growth: +5.35% in Q1; +14% in FY2022

- EBITDA Growth: +29.07% in Q1; +6579% in FY2022

- EBITDA Margin Growth: +15.75% in Q1; +23% in FY2022

- Net Operating Cash Flow Growth: -18.2% to $5.42M in Q1; +126% in FY2022

- Net Operating Cash Flow Growth as a % of Revenue: +8.93% in Q1; +1.5% in FY202

Compare the annual Income statements of POWW over the past 5 years here, the company’s annual Cash Flows over the same period here and POWW’s Balance Sheet information here.

AMMO’s analysis of the separation of these distinct business units on a go-forward pro forma basis results in projected 2023 AOS Fiscal Year guidance of revenue at $230 -$240 million and Adjusted EBITDA at $57 – $60 million.

Valuation

(The following information was provided by Chris Thompson, President & Director of Research of eResearch Corporation (eresearch.com).

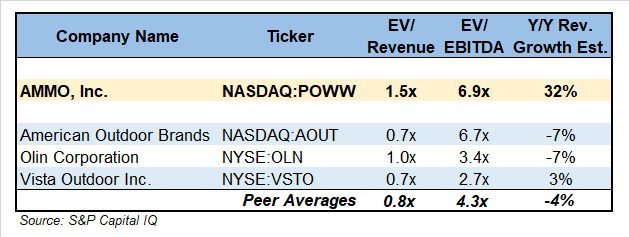

AMMO is currently trading at 1.5 times (x) Enterprise Value to Revenue (EV/Rev) and 6.9x Enterprise Value to EBITDA (EV/EBITDA), with EV defined as Market Capitalization plus Net Debt and Preferred Equity. Peers currently trade at a mean of 0.8x EV/Rev and 4.3x EV/EBITDA, so AMMO is currently trading above its peers.

Currently, three analysts cover the company with an average target price of $8.00, representing more than a 150% price appreciation. The analysts’ consolidated revenue estimate shows an average 12-month growth rate of 32%, with 23% in F2023 and 20% in F2024, which is greater than its peers and can justify a higher valuation metric.

AMMO’s recent stock price decline was due to the market’s reaction to a month-over-month decrease in quarterly revenue, lower gross margin, and missing analysts’ consolidated revenue estimates.

With the upcoming company split, the investor needs to understand if they want to invest in both segments of the business or wait until the split is completed and focus on either the manufacturing side or the online marketplace, as each segment will have a different growth and profitability profile.

Conclusion

With robust consumer demand at home, production capacity running at full tilt, supply chain issues creating scarcity, input costs going up, and import restrictions that will further inflame inventory problems, the ammo market is suddenly a high-profit center for manufacturers, and AMMO, Inc. stands to be a key beneficiary with its new state-of-the-art production facility and the splitting of its operation into separate manufacturing and sales (online) publicly traded companies to better focus on the major opportunities at hand.