“Follow the munKNEE” via twitter & Facebook or Register to receive our daily Intelligence Report (Recipients restricted to only 1000 active subscribers)

I view the current market weakness in gold, coupled with the pullback in trader positions, as a shorting opportunity which is strong in terms of reward vs. risk. I have come to that conclusion by questioning the assumptions that many make about it, isolating its fundamental drivers and providing a trading recommendation as to where I believe the price is headed in the future. Let me share my analyses with you. (Words: 1440; Charts: 4; Tables: 1)

positions, as a shorting opportunity which is strong in terms of reward vs. risk. I have come to that conclusion by questioning the assumptions that many make about it, isolating its fundamental drivers and providing a trading recommendation as to where I believe the price is headed in the future. Let me share my analyses with you. (Words: 1440; Charts: 4; Tables: 1)

So say edited excerpts (paraphrased) from an article* written by QuandaryFX and posted on Seeking Alpha under the title Prepare to Short Gold.

Lorimer Wilson, editor of www.munKNEE.com (Your Key to Making Money!), may have further edited ([ ]), abridged (…) and/or reformatted (some sub-titles and bold/italics emphases) the article below for the sake of clarity and brevity to ensure a fast and easy read. Please note that this paragraph must be included in any article re-posting to avoid copyright infringement.

The article goes on to say, in part:

Myth #1: Inflation

The first thing that comes to mind when individuals think of purchasing gold is inflation. For the majority of my life, gold has been advertised as the ultimate hedge against inflation in that as inflation increases, physical assets increase as well and by owning gold, individuals will preserve or increase their buying power. This relationship between gold and inflation simply isn’t true.

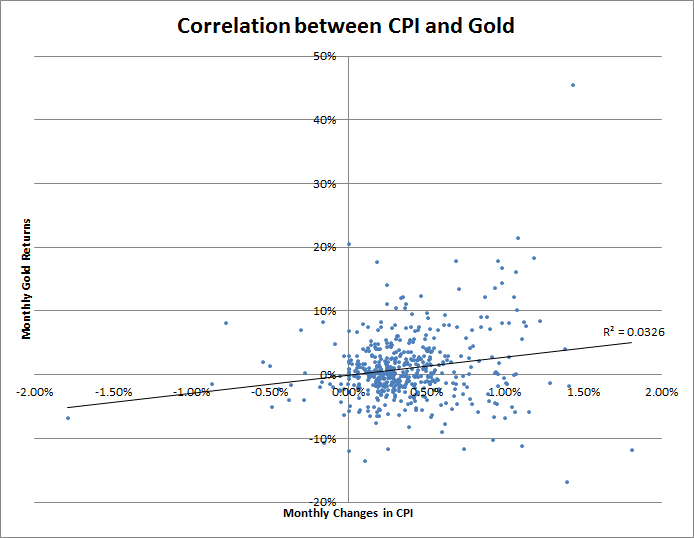

Inflation increases prices in that there are more dollars chasing the same amount of goods. For a good to actually increase in price due to inflation, there must be sufficient demand for the good such that individuals with dollars are willing to pay greater amounts of money for the same amount of the good or service. Let’s pose and test a basic question: does gold increase in price as inflation increases? In order to answer this question, I have correlated monthly changes in the Consumer Price Index (a popular measure of inflation) with monthly changes in spot gold prices. The chart below shows this correlation.

(click to enlarge)

The relationship between inflation and gold prices simply isn’t there. As inflation increases, gold moves in a direction entirely unrelated. Mathematically speaking, the correlation between inflation and the price of gold is only 0.18 which is considered to mean little to no correlation is present.

Myth #2: Financial Panic

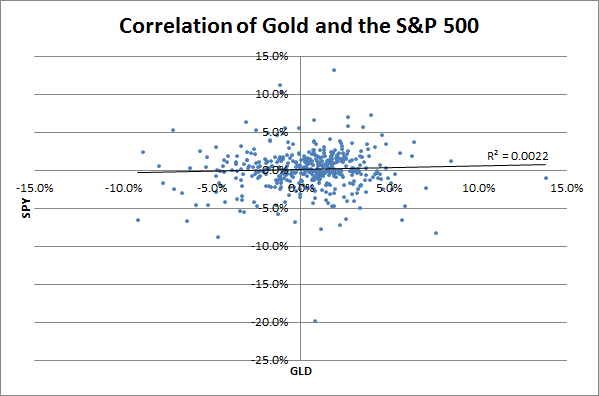

Well, if inflation doesn’t direct gold prices, what about the stock market? It makes sense that as the world markets tank, investors flock to “safe” assets which will “preserve” buying power, right? Wrong. The basic idea here is that in the event of market collapses, investors will flee to gold and preserve their purchasing power. Let’s test this belief by correlating weekly market returns with weekly gold returns.

(click to enlarge)

It can clearly be seen that once again, popular theories don’t hold weight against data. If gold was a method of preserving value in the event of financial volatility, then there would be a negative correlation between the S&P 500 and gold or a clearly-defined relationship as points deviate from the mean. Neither of these factors is present. In fact, the correlation between the stock market and gold is .04, which basically means that there is no relationship present.

Myth #3: Supply and Demand

Another myth that individuals espouse is that there is some sort of supply shortage in which the natural demand for gold is driving up price. This is radically incorrect. According to the World Gold Council, the demand is currently being met and slightly exceeded by supply, on average. Additionally, there is over 44 times the average quarterly demand for gold sitting in stocks. In any other commodity, this type of supply, demand, and storage situation would lead to price collapse. Imagine if we had 44 times our quarterly consumption of wheat already sitting on the shelves in some form or fashion – wheat prices would be a fraction of what they are today! Simply said, a supply and demand relationship is not influencing the price of gold in any tangible way.

Sentiment

I’ve worked within the trading industry long enough to know that there are only three things which drive prices:

- supply,

- demand, and

- sentiment.

We’ve talked about supply and demand and found that these factors are ultimately irrelevant and powerless to influence gold’s price behavior. That leaves us with the only other possible factor: sentiment. It is my belief that the only factor which is driving gold right now is sentiment and the best way to determine sentiment is to monitor the Commitments of Traders (COT) reports.

The Commodity Futures Trading Commission requires large traders and commercial players to disclose their position on a weekly basis so as to prevent position limit infractions and potentially manipulative behavior. These charts make excellent timing tools in that they show us where the professionals are positioned. It is very important to understand that these positions are put on by people who literally must make money on their trader or search for a new line of work. In light of this reality, traders and investors should highly regard COT reports.

The chart below shows the past four years of COT data.

- The red squiggly line at the bottom of the chart shows the total position of large professional traders – people who are paid to be right.

- The green line shows commercial hedgers – people who intentionally pay to be wrong by hedging their production.

- The blue line shows small traders – people who, for the most part, are amateurs just having fun. In many markets, small trader positions act as a strong contrarian signal in that the amateurs are almost always wrong.

(click to enlarge)

During the first time period which represents the time period between 2009 and the middle of 2011 and labeled “1” in the chart above, professional traders, on average, maintained positions totaling around 180,000 contracts. The price of gold increased 100% (or $800 per ounce). The standard contract represents 100 Troy ounces which means that during this time professional traders earned around $14.4 billion in profits.

During the second time period, labeled “2”, professional traders cut back on their position. Between the middle of 2011 and 2012, traders booked profits on about 50,000 contracts. The selling by these large traders caused the market to stop its multi-year bull-run for several quarters. Commercial hedgers (the green line) also cut back on their positions due to the fact that decreasing prices allow a player who is naturally short to decrease its hedge exposure.

It gets really interesting at point “3”. The large leap in traders’ positions during the past quarter coincides with the speculation and announcement of QE3. QE3, as you probably know, is the Federal Reserve’s announcement that it will continue to essentially print money in order to stimulate business. Printing money eventually leads to inflation. The popular belief about inflation increasing the price of gold is simply incorrect, as we’ve discussed. Professional traders know this, but realistically they put these trades on hoping that the amateurs are unaware of the lack of relationship. Ultimately, trading is a zero-sum game and the only way these guys make money is through the systematic transfer of wealth from the uninformed to the informed. If you notice, immediately after traders put large positions on leading up to QE3, professionals cut back their positions by around 30,000 contracts. Let’s talk about why….

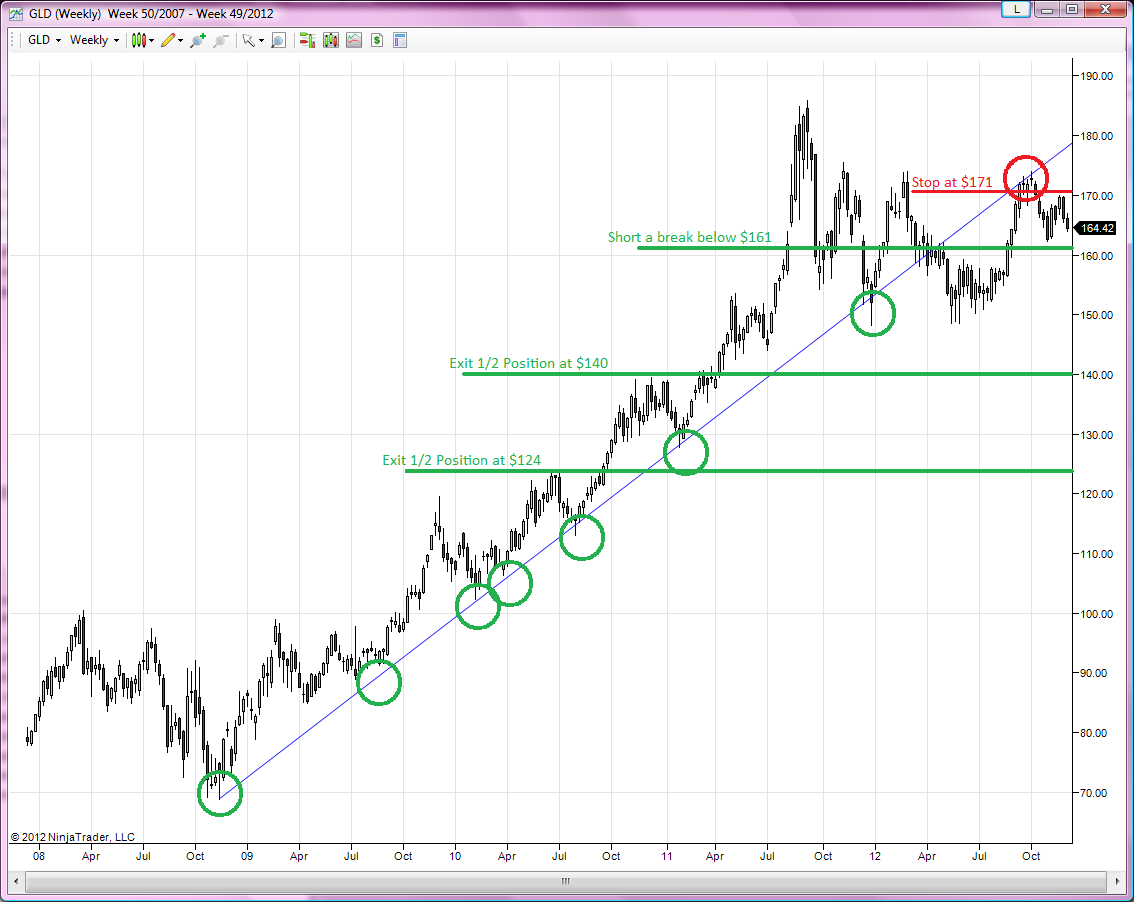

Something very significant happened which caused these traders to cut back on their positions by nearly 15%. For the most part, these professional traders are following the trend: as price increases, they are long and as price decreases they are out of the market or short. A very important shift in sentiment occurred during the first week of October, which was the failure of gold to resume its uptrend, technically established in 2008. What this tangibly means is that the trend is no longer increasing and traders are cutting back their positions to book profits or quickly cut losses. I have circled this rejection (in red) of the uptrend on the chart…[below].

Conclusion

I view this market weakness coupled with the pullback in trader positions as a shorting opportunity. The inability of gold to make new highs coupled with the fact that the recent highs correspond perfectly to technical resistance points makes a short thesis strong in terms of reward versus risk.

(click to enlarge)

Editor’s Note: The author’s views and conclusions are unaltered and no personal comments have been included to maintain the integrity of the original article. Furthermore, the views, conclusions and any recommendations offered in this article are not to be construed as an endorsement of such by the editor.

*http://seekingalpha.com/article/1050481-prepare-to-short-gold

Register HERE for Your Daily Intelligence Report Newsletter

It’s FREE

Only the “best-of-the-best” financial, economic and investment articles posted

Edited excerpts format provides brevity & clarity for a fast & easy read

Don’t waste time searching for informative articles. We do it for you!

Register HERE to automatically receive every article posted

Recipients restricted to only 1,000 active subscribers!

or

“Follow Us” on twitter & “Like Us” on Facebook

Related Articles:

1. The Preferred Way to Explain Gold Price Behaviour + 13 Alternatives

1. The Preferred Way to Explain Gold Price Behaviour + 13 Alternatives

There is a substantial debate about what asset, if any, gold price relates to or responds to….We think the most logical factor in its price as a form of money would be the ratio of the currency in circulation versus the amount of gold that could be associated with that currency…We have heard some strong opinions to the contrary…that perhaps some other assets other than currency in circulation could be used to explain gold price behavior, and therefore provide some gauge of over and under valuation in the market price. [We look at 14 different assets below.] Words: 586

2. Sell Some of Your Gold If and When Any 1 of These 10 Events Occur

Most of us will sell our gold sometime between now and never so what events will probably indicate that the time has come to sell at least some of your gold? Words: 910

3. Why Is the Price of Gold So Very Weak? Here’s Why

As I see it, worsening financial crises lead initially to lower gold prices which are followed by some form of government intervention to alleviate the crises and that action, in turn, eventually results in renewed appreciation in the price of gold. The basic steps in such a transition are really quite straightforward. (Words: 477; Charts: 2)

4. Dr. Nu Yu’s Latest Analysis Shows Why Current Gold, Silver and HUI Levels Are No Surprise

5. Who Is Responsible for Current Weakness in Gold?

Just as US investors are advised not to fight the Federal Reserve, gold investors worldwide would be well advised not to fight the Government of India. India is the world’s largest gold consumer [and their intent on curbing gold imports by any means necessary could have a negative effect] on world gold demand [and, as such, most likely, on gold prices. IMO,] at best, we will see a sideways market in the price of gold in 2013, and at worst, this will be the year when gold prices start the inexorable drop.

6. I Will Not Turn Bullish On Gold Until 1 of 2 Things Happen

My forecast — despite all the hate mail and pressure I get to change it — has not changed. Based on my systems and models, I will not turn bullish on gold until either spot gold has closed above $1,823 an ounce on a weekly and monthly basis – or gold cracks the $1,527 level and plunges to the $1,400 level or a tad lower. I know that’s not what you want to hear. I know that you are as eager as I am to see the next leg of gold’s bull market begin….[but its] time to shine is not here yet. It will come again so stay the course, build up your ammo, and be ready to pull the trigger when I issue a headline like “Back Up the Truck, NOW!”

7. Bull Markets Always End With a Bang, Not a Whimper, So Gold’s Run Should Have More Legs

8. 5 Compelling Reasons Why It’s Now Time to Sell Gold

I recently explained my thesis for why gold’s 12-year winning streak will come to an end in 2013…[and] nearly a month into 2013, the case for selling gold is gaining strength. [This article puts forth 5 compelling reasons why it is now time to sell gold.] Words: 690 ; Charts: 2

9. Rising Deflation Concerns Could Cause Gold to Plummet Dramatically – Here’s Why

9. Rising Deflation Concerns Could Cause Gold to Plummet Dramatically – Here’s Why

The arguments for gold to rise dramatically are well known and highly publicized. The arguments for gold to remain flat or to decline are minimally discussed and generally attacked vigorously when raised. [I do just that in this article and the conclusions will not be liked by the goldbugs.] Words: 285

10. My Case Against the Case Against The Case Against Gold

All thing considered, it seems clear that the long-term real returns of gold have been poor (compared to stocks and bonds), and I see no reason to expect long-term price appreciation for gold to be above inflation. In fact, as with any non-income producing asset, it would be unreasonable to expect gold to provide significant positive real returns over an indefinite period of time…I would argue that buying gold is a short-term gamble that is completely dependent on the unpredictable vagaries of perception, market psychology and the “greater fool” theory…While it is true that gold can be a good short-term trade and offer superior returns over shorter periods (as has been the case in recent years) I believe that stocks will continue to substantially outperform gold over time. [Let me explain these less than popular conclusions further.] Words: 1258

All thing considered, it seems clear that the long-term real returns of gold have been poor (compared to stocks and bonds), and I see no reason to expect long-term price appreciation for gold to be above inflation. In fact, as with any non-income producing asset, it would be unreasonable to expect gold to provide significant positive real returns over an indefinite period of time…I would argue that buying gold is a short-term gamble that is completely dependent on the unpredictable vagaries of perception, market psychology and the “greater fool” theory…While it is true that gold can be a good short-term trade and offer superior returns over shorter periods (as has been the case in recent years) I believe that stocks will continue to substantially outperform gold over time. [Let me explain these less than popular conclusions further.] Words: 1258

11. Goldrunner: These Fundamental Charts Say “Gold Is Getting Ready to Run!”

The U.S. Dollar is being very aggressively devalued in a parabolic…[manner] as we enter the final stage in the paper currency cycle. The government needs Gold to go vastly higher so the budget can be balanced after all of the paper promise debts are added to the balance sheet. Interestingly, Michael Belkin, arguably one of the best analysts in the world, expects earnings for companies to plunge this year causing the DJIA to crater about 30%. This fits with the kind of correction in the now high flying DJIA that we have discussed per the late 70’s charts where Gold and the Dow would meet between 10,000 and 12.000. Words: 1022

When are Gold and Silver going to start a huge parabolic move up? I, personally, think that we are sitting at the cusp [of such happening] as we speak on an intermediate-term basis….Below are… the fundamentals and technical set-up [to that end].

13. Goldrunner: What We ‘Know’ & ‘Don’t Know’ About Where Gold, Silver and PM Stocks Are Going

One never knows exactly where Precious Metals are going so I always try to keep in mind a list of items that are probable based on the facts that are evident. I call this “what we know” and “what we don’t know” so let’s take a look what we “know” and “don’t know” at this point in time. Words: 871

14. A Plea From Jim Sinclair: You Are Being Played – Do NOT Give Up Your Gold!

The paper gold market is being used to shake the bullish tree harder this time than any time before because of what is to come. Fear is the most powerful emotion in markets and it is being used perfectly to enrich the grand names of finance at your expense. We are right in front of that time when the market performs a classic bottom both in shares and physical. From this point gold is going to and through $3500 [so] if you are unable to buy at this time there is one thing you can do – to get into the fight and out of the stands. That act is do nothing, and do not capitulate. Let them play the price game, but give them nothing whatsoever of yours. Words: 758

There is a nasty game taking place which relies entirely on scaring you out of your wits. Yes, out of your mind, so you sell something of great value for peanuts to the exact party playing with your head via price. When you must look at the action, remember there is a buyer for every seller. That buyer is not scared out of his/her wits if you sell to stop the pain you are in. This period is, in my opinion, the last and largest attack you will see perpetrated on us before gold closes over $3500. This period of pain will not be measured in months, but counted in history as days. Stand firm and stay the course! Words: 787

16. Gold Projected to Reach $4,000/ozt. Sometime Between Late 2015 & Mid 2017! Here’s My Rationale

I am not predicting a future price of gold or the date that gold will trade at $4,000, but I am making a projection based on rational analysis that indicates a likely time period for gold to trade at $4,000 per troy ounce. Yes, $4,000 gold is completely plausible if you assume the following:

I am not predicting a future price of gold or the date that gold will trade at $4,000, but I am making a projection based on rational analysis that indicates a likely time period for gold to trade at $4,000 per troy ounce. Yes, $4,000 gold is completely plausible if you assume the following:

17. Alf Field: Gold STILL Targeted to Reach $4,500 – Preceded By Violent Upside Action

We now have a really strong probability that the correction which started at $1913 on 23 August 2011 has been completed both in terms of Elliott waves and also in terms of time elapsed. If this is correct, the gold price should soon be expressing itself in violent upside action as it moves into the third of third wave which is still targeted to reach $4,500. [Let me explain in detail (with charts) how and why my most recent analyses confirm my earlier target of $4,500.] Words: 1085

18. New Analysis Suggests a Parabolic Rise in Price of Gold to $4,380/ozt.

19. Egon von Greyerz: Gold & Silver Off to the Races – to $4,500+ & $100+ Each – Here’s Why

The closing of the gold window back in August 1971 has led governments worldwide to create endless amounts of worthless paper money and the resulting credit bubble has created a world debt exposure of over US$ 1 quadrillion (including derivatives). It has also created perceived wealth for big parts of the world’s population – a wealth which is only backed by promises to pay and by grossly inflated assets. Few people realise that this wealth is totally illusory and will implode considerably faster than the time it took to create it. [Let me explain.] Words: 890

The closing of the gold window back in August 1971 has led governments worldwide to create endless amounts of worthless paper money and the resulting credit bubble has created a world debt exposure of over US$ 1 quadrillion (including derivatives). It has also created perceived wealth for big parts of the world’s population – a wealth which is only backed by promises to pay and by grossly inflated assets. Few people realise that this wealth is totally illusory and will implode considerably faster than the time it took to create it. [Let me explain.] Words: 890

20. Goldrunner: Price Target of $10,000 to $12,000 for Gold Still Holds

21. Nick Barisheff: $10,000 Gold is Coming! Here’s Why

22. Gold’s Recent Price Action Suggests Ultimate Top of $5,000/ozt.

The correlation between the gold price from 1968 until 1979 and from early 2000 until today is an amazing 89.65%! More specifically, the correlation from 1975 until April 1979 and from January 2008 until today is an astonishing 97.83% suggesting that gold will reach an ultimate top of $5,000 per troy ounce before the bubble bursts. Words: 330

The correlation between the gold price from 1968 until 1979 and from early 2000 until today is an amazing 89.65%! More specifically, the correlation from 1975 until April 1979 and from January 2008 until today is an astonishing 97.83% suggesting that gold will reach an ultimate top of $5,000 per troy ounce before the bubble bursts. Words: 330

23. Update: 51 Analysts Now Maintain that Gold is Going to $5,500 – $6,500/ozt. in 2015!

Lately analyst after analyst (161 at last count) has been climbing on board the golden wagon with prognostications as to what the parabolic peak price for gold will eventually be. That being said, however, only 51 have been bold enough to include the year in which they think their peak price estimate will occur and they are listed below. Take a look at who is projecting what, by when and why. Words: 644

Lately analyst after analyst (161 at last count) has been climbing on board the golden wagon with prognostications as to what the parabolic peak price for gold will eventually be. That being said, however, only 51 have been bold enough to include the year in which they think their peak price estimate will occur and they are listed below. Take a look at who is projecting what, by when and why. Words: 644

24. Gold Should Be At $4,666 These Days – Here’s Why

Since the Financial Crisis erupted in 2007, the US Federal Reserve has engaged in dozens of interventions/ bailouts to try and prop up the financial system…and the amount of money printed is absolutely staggering. As a result of this, inflation hedges, particularly Gold, have been soaring…[but] for gold, for example, to hit a new all time high adjusted for inflation, it would have to clear at least $2,193 per ounce. If you go by 1970 dollars (when gold started its last bull market) it would have to hit $4,666 per ounce. Words: 581

Since the Financial Crisis erupted in 2007, the US Federal Reserve has engaged in dozens of interventions/ bailouts to try and prop up the financial system…and the amount of money printed is absolutely staggering. As a result of this, inflation hedges, particularly Gold, have been soaring…[but] for gold, for example, to hit a new all time high adjusted for inflation, it would have to clear at least $2,193 per ounce. If you go by 1970 dollars (when gold started its last bull market) it would have to hit $4,666 per ounce. Words: 581

25. Here’s An Easy Way to Identify Gold & Gold Miner Market Tops and Bottoms

It’s amazing! Every day I learn something new. I have just come across a very powerful tool that identifies market tops and bottoms in both the gold price and the gold mining industry valuation. Let me share it with you. Words: 352; Charts: 4

The fact that nobody really knows with absolute certainty where gold will really go from today onward makes people try to make their own guesses about what can happen with the yellow metal. One of the methods to do that is to look back into past situations and try to estimate if what is happening now is somehow similar to those past events. The situation in the gold market today is different than the one in 1980 in a few important areas. Even if past patterns don’t give you any certainty, though, sometimes they can limit the uncertainty. Let us analyze that in more detail. Words: 1260; Charts: 2