“Ben Bernanke is trying like mad to stimulate credit and lending but to no avail. It’s an uphill battle because of demographics, student debt, and lack of jobs. [Frankly however, given such an environment,] prospects for family formation are fundamentally very weak and overall economic fundamentals are very weak as well” [and that certainly does not bode well for housing coming back anytime soon. Let me explain.] >Michael “Mish” Shedlock< (http://globaleconomicanalysis.blogspot.com) Words: 650

avail. It’s an uphill battle because of demographics, student debt, and lack of jobs. [Frankly however, given such an environment,] prospects for family formation are fundamentally very weak and overall economic fundamentals are very weak as well” [and that certainly does not bode well for housing coming back anytime soon. Let me explain.] >Michael “Mish” Shedlock< (http://globaleconomicanalysis.blogspot.com) Words: 650

Lorimer Wilson, editor of www.munKNEE.com (Your Key to Making Money!), has edited the article below for length and clarity – see Editor’s Note at the bottom of the page. This paragraph must be included in any article re-posting to avoid copyright infringement.

Shedlock goes on to say, in edited excerpts from his original article*:

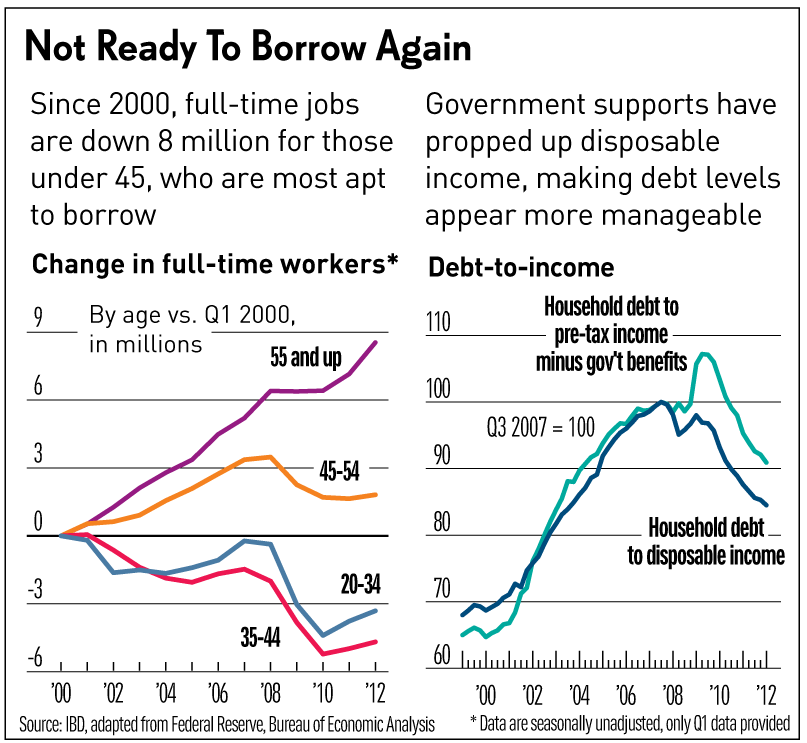

Consumers Not Ready to Borrow Again

Citing falling debt-service needs, some economists think consumers may be ready to go on a borrowing spree. They are badly mistaken. I agree with Jed Graham on Investor’s Business Daily who says falling debt-service needs is an illusion. Graham makes the case in Consumer Credit Impaired By Under-45 Job, Debt Woes that:

Nearly four years after a borrowing binge gave way to financial crisis, have households slashed enough debt to take on new credit and start spending again?

Yes, says a growing chorus of economists, with some evidence to back them up. The Federal Reserve’s ratio of debt service payments to disposable income is at its lowest level since 1994. That traditional measure is a poor guide today, however, as credit-hungry adults under 45 bear the brunt of the jobs, housing and student loan crises.

Considering where more of the income is coming from (government supports), who’s earning a bigger share of wages (baby boomers) and which type of debt has been on the rise (student loans), re-leveraging may be a long way off.

Not Ready to Borrow

Graham’s analysis is correct. Here are some points from the article that will explain why.

Demographics

- The number of full-time workers younger than 45 has fallen by 9 million, or more than one in seven, Labor Department data show.

- The number of full-time workers ages 55 and older has climbed by 8.5 million.

- The 35-44 population has shrunk by 4.5 million over the past 12 years.

- The huge baby boomer cohort has aged while Generation X is unusually small.

Student Debt

- Student debt has soared to nearly a trillion dollars. About two-thirds of it is held by those under 40.

- Among those age 30-39, 25% have student loan debt, with an average balance of $28,500.

- New York Fed research shows that of 37 million student loan borrowers last fall, only 39% were paying down their balances.

Jobs

To Graham’s analysis I would add the jobs picture is bleak.

- Unemployment insurance has expired for millions: 200,000 Lose Unemployment Benefits This Week, Nearly Half From California

- Self-Employment desperation: 100% of U.S. Jobs Added Since 2010 Have Been Self-Employment, Contractor, or Other Jobs Without Unemployment Insurance Benefits

- Last two jobs reports have been dismal: Another Payroll Disaster: Jobs +69,000, Employment Rate +.1 to 8.2%, April Jobs Revised Lower to +77,000; Long-term Unemployment +310,000

- The 4-week moving average of weekly unemployment claims is at the highest rate of the year, at 386,250.

Take Note: If you like what this site has to offer go here to receive Your Daily Intelligence Report with links to the latest articles posted on munKNEE.com. It’s FREE! An easy “unsubscribe” feature is provided should you decide to cancel at any time.

Housing

Let’s put it all together and look at the picture from the point of view of housing.

- Kids are graduating from college deep in debt with poor job prospects.

- Those with too much debt and too little income are sharing apartments or moving back home, not buying homes and starting families.

- Boomers are looking to downsize, not buy more toys and larger houses.

- Shadow inventory of sellers waiting for higher prices is immense, yet generation X and Generation Y represent small pools of potential buyers

Factor in the rapidly slowing Chinese economy (China Manufacturing PMI 7-Month Low, Sharpest Decline in New Export Orders Since March 2009) coupled with Europe in the midst of a severe recession, and it’s difficult if not impossible to see just where US growth will come from.

Conclusion

Nonetheless, I believe housing is bottoming…. but even “if” housing is bottoming, don’t expect either housing or the economy to go anywhere fast. Prospects for family formation are fundamentally very weak and overall economic fundamentals are very weak as well.

*http://globaleconomicanalysis.blogspot.ca/2012/06/three-key-reasons-housing-not-coming.html (To access the above article please copy the URL and paste it into your browser.)

Editor’s Note: The above article may have been edited ([ ]), abridged (…), and reformatted (including the title, some sub-titles and bold/italics emphases) for the sake of clarity and brevity to ensure a fast and easy read. The article’s views and conclusions are unaltered and no personal comments have been included to maintain the integrity of the original article.

Related Articles:

1. Housing Prices Expected to Rebound in 2013 – 2014 – Here’s Why

We are currently seeing bullish indicators regarding housing demand coupled with bearish indicators regarding housing prices. Let’s take a look at the past relationship between house demand and house prices and see what it suggests for the future in real estate prices. Words: 450

2. This Hard Data Clearly Says: Real Estate is in Recovery Mode!

Auto sales, consumer confidence, manufacturing, retail sales, exports – you name it – over the last six months, nearly every facet of the U.S. economy has shown improvement and the real estate market is no exception. [Here are 11 irrefutable signs that such is the case.] Words: 800

3. What Does the Latest Rent vs. Buy Index Have to Say?

If you have been on the fence trying to decide if you should rent or buy, the market may be in your favor. According to Trulia’s Winter 2012 Rent vs. Buy Index it is now cheaper to buy a home rather than rent in 98 of the 100 largest U.S. metropolitan areas. How can that be? Take a look!

4. Your House: A Home, An Investment or a Ponzi Scheme?

In the past few decades, the concept of home ownership has been completely turned on its head. Previously, homes were considered a very long-term consumption good…[No one] ever considered tripling the value of their homes by retirement time and selling them to move beachside yet, somehow along the way, this became a reasonable investment expectation. Even today, home buyers still make their purchases with the hopes of escalating prices. [It begs answers to these questions: Is a house just a home? Should a house be expected to behave like an investment? Is the housing game nothing more than a Ponzi scheme where the end buyer before the market corrects becomes the “greater fool”? Let’s try and answer those questions.] Words: 935

5. Price:Rent Ratio Suggests House Prices Have Further to Fall

The rat-through-the-snake process of working down existing and prospective distressed properties is likely far from over, and how that process plays out will no doubt have an impact on how much housing prices will ultimately adjust. [Let’s take a look at some differing points of view in that regard.] Words: 497

6. U.S. House Prices Have MUCH Further To Fall! Here’s Why

There has been a deluge of articles recently about the upticks in the housing data…[yet, while] I do not dispute the improvement in the data regarding home starts, permits, pending sales, etc.,… [see graph below] these data points are still mired at very depressed levels so the assumption is that if home building is stabilizing then it is only a function of time until home prices began to rise as well. Right? Not so fast.. [Let me explain.] Words: 1100

7. A Housing Boom is Coming! A Housing Boom is Coming! Here’s Why

Yes, you read that right; get ready for the next housing boom. You’re probably thinking, “How could that be with all the mortgage delinquencies and foreclosures going on, and the record levels of housing inventory? Well, it’s not going to happen soon – [probably] not for several more years – but it’s coming. [Let me explain to you why it is inevitable.] Words: 589

Our Gov’t. has given low to zero interest loans to our Big Banks and they instead of loaning money to US citizens, have chosen to invest in Foreign Banks…

Now as US jobs become Part time jobs the ability of folks to borrow has been reduced to the point that almost nobody can get a loan, which is driving the price (value) of housing ever downward…

Wall Street wants to insure that US citizens will never again be able to use real estate to make money again…

Europe’s Economic Implosion In One Chart

http://is.gd/8pSdZz

In short, the Bankers have taken over…

The Political Leaders are just figureheads, (just like in Japan) and serve to insulate those that are really calling the shots!

I call it the Japanese-ing of the USA (and Europe)!