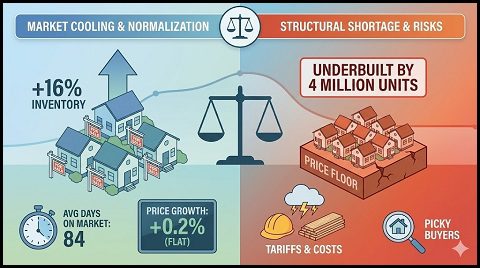

When looking at the numbers, you see something that feels a bit strange. For years, the story was always about how nothing was for sale. It was a desert out there. Now? Inventory is up over 16%. That is a massive jump for a single year.

The market is starting to cool down into something that looks like balance. Or at least something closer to it. People call it normalization. It is a word economists love because it sounds safe.

But for a buyer who has been sidelined for three years, it feels like a relief. Maybe even a shock. Homes are taking longer to sell now. The average is 84 days. That is up almost 10% from last year.

Buyers can actually walk through a house and think about it for a day or two without losing it to a cash offer five minutes later. Price growth has basically flattened out with just a 0.2% move in the median list price. That is basically a rounding error in the grand scheme of things.

Does this mean that the frenzy is over? Is the “bidding war” era a distant memory now? Almost like a dream you’d rather forget.

That Structural Shortage is Still Real

But here is the catch. Even with more homes on the market, the housing market is still structurally short. The U.S. remains underbuilt by about 4 million units. That is a big number.

Builders can’t just construct 4 million homes overnight. Utilization of the housing stock is at 90%. A decade ago, it was 87%.

That three-point shift illustrates why prices haven’t collapsed. The floor is very solid because there are still more people who need roofs than there are roofs available. It limits how far this “cooling” can actually go. It keeps things from breaking too hard.

The reality is that even as inventory rises, it isn’t enough to fill the hole left by a decade of under-construction. Builders are trying, but they are fighting uphill. There is a supply gap that won’t just vanish because a few more people decided to list their homes. It is a permanent fixture of the current economy.

Buyers are Getting Picky

Demand is still there, but it is much more selective. Buyers haven’t disappeared into thin air. They are just being choosier. They have to be.

Total sales hit 4 million against just 3 million new listings, a clear sign that buyers are drawing down the older inventory. People are still moving. It is just a patchwork market now.

Earlier this year, the Greenville and Manchester housing markets were “on fire” with Market Action Index scores over 70. Other cities are much colder. It is not one single national story anymore. It is a local one. Each city has its own mood.

In these “hot” pockets, there still might be competition. But elsewhere? Buyers are walking away from houses that need work. They want “turnkey” or they want a massive discount. The power has shifted, just a little bit, back to the person with the checkbook. It makes for a slower, more deliberate process.

The Tariff Wild Card and Other Risks

Then there is the macro wildcards. J.P. Morgan keeps talking about how policy is the new driver. Rates are still the big one, of course.

But the Trump administration and these new tariffs are changing things. They add a lot of volatility. If you are a builder, your costs are increasing as outlined by the National Association of Home Builders. Steel, lumber, and appliances all get hit by these trade moves. It makes the supply chain a mess again.

Then there is an immigration policy affecting how many new households are forming. It injects a lot of uncertainty into the supply and demand math. Uncertainty usually leads to hesitation. Or bad decisions.

These policy levers are essentially a new layer of risk that wasn’t there a few years ago. If construction costs spike because of tariffs, the “floor” under home prices gets even higher. It makes new builds more expensive, which pushes people back toward existing homes. It’s a messy cycle that doesn’t have a clear exit yet.

Prices are Softening but Don’t Expect a Crash

There are the price cuts, too. According to Housingwire, about 39% of listings saw a price reduction this year. That is almost four out of every ten houses.

The price per square foot even dropped a tiny bit, about 1%. This is not a crash. It is a market finding its level. It is softening. It is a search for equilibrium. It is what happens when you hit the limit of what people can pay.

Some banks are being a bit more helpful lately, too. The credit crunch of the past decade is mostly behind us. They still want the best credit scores, but they are easing some of those tight restrictions. They have to. Volume is low and they need the business.

But they won’t go back to the 2007 days. Those days are gone for good. There might be a slow shift where the Fed is cutting rates and banks are trying to find their footing in a world where 6% or lower is the new normal.

Final Thoughts for Buyers

If you are looking at this market, patience is your best friend. You don’t have to rush as you did in 2021. You have 84 days to make a move. Use them.

Watch the tariff news and see how it hits construction. If building costs go up, those new homes will get more expensive. But the existing ones might stay flat.

It is a weird time. A normalizing time. It is not perfect, but it is better than the madness there was before. Just keep an eye on your credit score and stay conservative. The floor is here. It’s just a bit lower than the ceiling used to be.