With wage growth suppressed and consumers still driving over 70% of the nation’s GDP, weak economic growth should not be a surprise.

GDP, weak economic growth should not be a surprise.

So say edited excerpts from an article* written by the editor of SoberLook.com entitled Wages in the US remain suppressed.

The following article is presented by Lorimer Wilson, editor of www.FinancialArticleSummariesToday.com and www.munKNEE.com and the FREE Market Intelligence Report newsletter (sample here – register here) and may have been edited ([ ]), abridged (…) and/or reformatted (some sub-titles and bold/italics emphases) for the sake of clarity and brevity to ensure a fast and easy read. This paragraph must be included in any article re-posting to avoid copyright infringement.]

The article goes on to say:

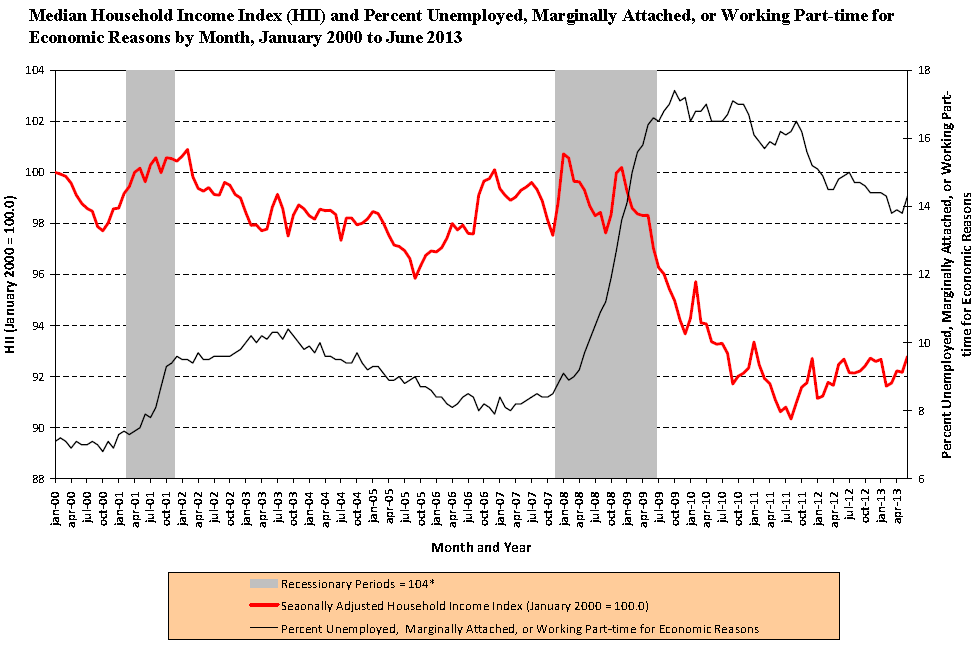

As the chart below shows, US median inflation-adjusted household income (red line) remains well below pre-recession levels (the chart also appropriately shows U6 unemployment).

|

| Source: Gordon Green and John Coder Sentier Research (click to enlarge) |

A large part of this wage dislocation can be explained by significantly higher use of part-time labor in the U.S.. The chart below shows the ratio of part-time to total payrolls which remains elevated.

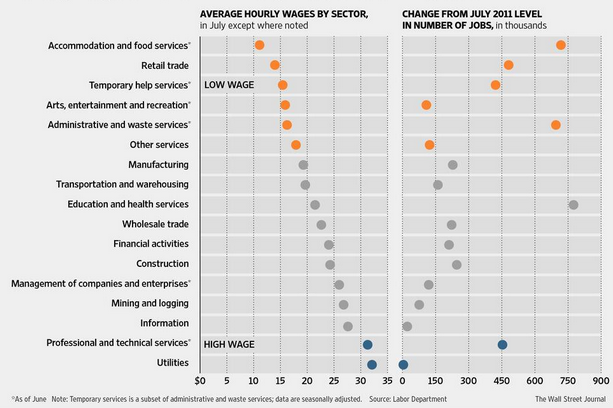

Furthermore, a good part of the U.S. job creation over the past couple of years has been in the low wage sectors. That, combined with the part-time employment trend (above) keeps household wages from rising substantially in spite of lower unemployment figures.

|

| Source: WSJ (see story) |

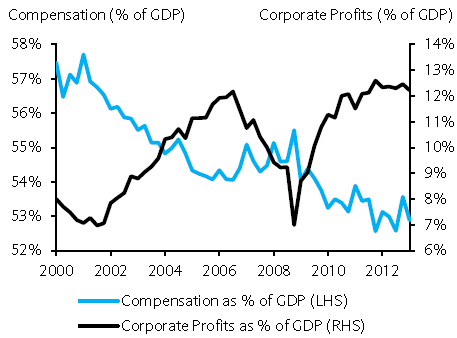

The cheaper labor costs in the U.S. and the recent increased use of part-time workers have significantly improved corporate bottom lines. Some US labor advocates argue that over the years corporations have been able to participate in the overall economic growth in part at the expense of lower wages (chart below). The counterargument of course is that this wage compression is critical for US-based firms to remain competitive globally and should ultimately result in more US-based business activity and hiring, particularly in manufacturing (see post). While we’ve seen more firms moving facilities to the U.S., it has not been the panacea some have been hoping for.

|

| Source: Barclays Capital |

Barclays Capital: – During the recession and the subsequent recovery with its weak growth, companies have been aggressively managing their bottom line. They’ve refrained from hiring, raising pay or otherwise investing in business expansion. Compensation as a percentage of GDP has been falling since the end of 2008 and now stands close to a 13-year low.

Moreover, some are suggesting that the Patient Protection and Affordable Care Act will ultimately result in even higher ratios of part-time employees – and therefore lower household incomes. While there is little evidence for this currently, longer term effects remain uncertain.

Conclusion

Whatever the case, with wage growth suppressed and consumers still driving over 70% of the nation’s GDP, weak economic growth should not be a surprise.

[Editor’s Note: The author’s views and conclusions in the above article are unaltered and no personal comments have been included to maintain the integrity of the original post. Furthermore, the views, conclusions and any recommendations offered in this article are not to be construed as an endorsement of such by the editor.]

*http://soberlook.com/2013/08/low-wages-in-us-holding-back-growth.html (Content copyright 2009-2013. SoberLook.com. All rights reserved.)

Related Articles:

1. Talk of Jobs Coming Back Courtesy of the Fed is Ridiculous! Here’s Why

Despite the preponderance of evidence that money printing doesn’t create jobs, Bernanke and his Central Bank colleagues continue to perpetuate the myth that the recovery is just around the corner, as long as we continue to print money. It’s complete and utter insanity as all it will accomplish is bankrupting the U.S. resulting in higher costs of living – and lower quality of life – for all of us. [Let me explain why I believe that is the case.] Read More »

2. This Gov’t Chart Shows That There Is NO Economic Recovery

5 years into the official economic “recovery” the labor participation rate is still lower than when the recession was declared over in June 2009 by almost a percentage point. It is still over 4 percentage points lower than when the recession officially began. The Federal Reserve chart of employment as a percentage of working age adults proves the point that sometimes a picture is worth a thousand words – sometimes much more. Words: 388; Charts: 1 Read More »

Congress is playing right into the hands of the Ultra Wealthy, (many feel on purpose) by enabling them to own ever more of the USA, thanks to the shift from good paying middle class jobs to part-time low paying jobs which only benefits Big Business and those that own them!