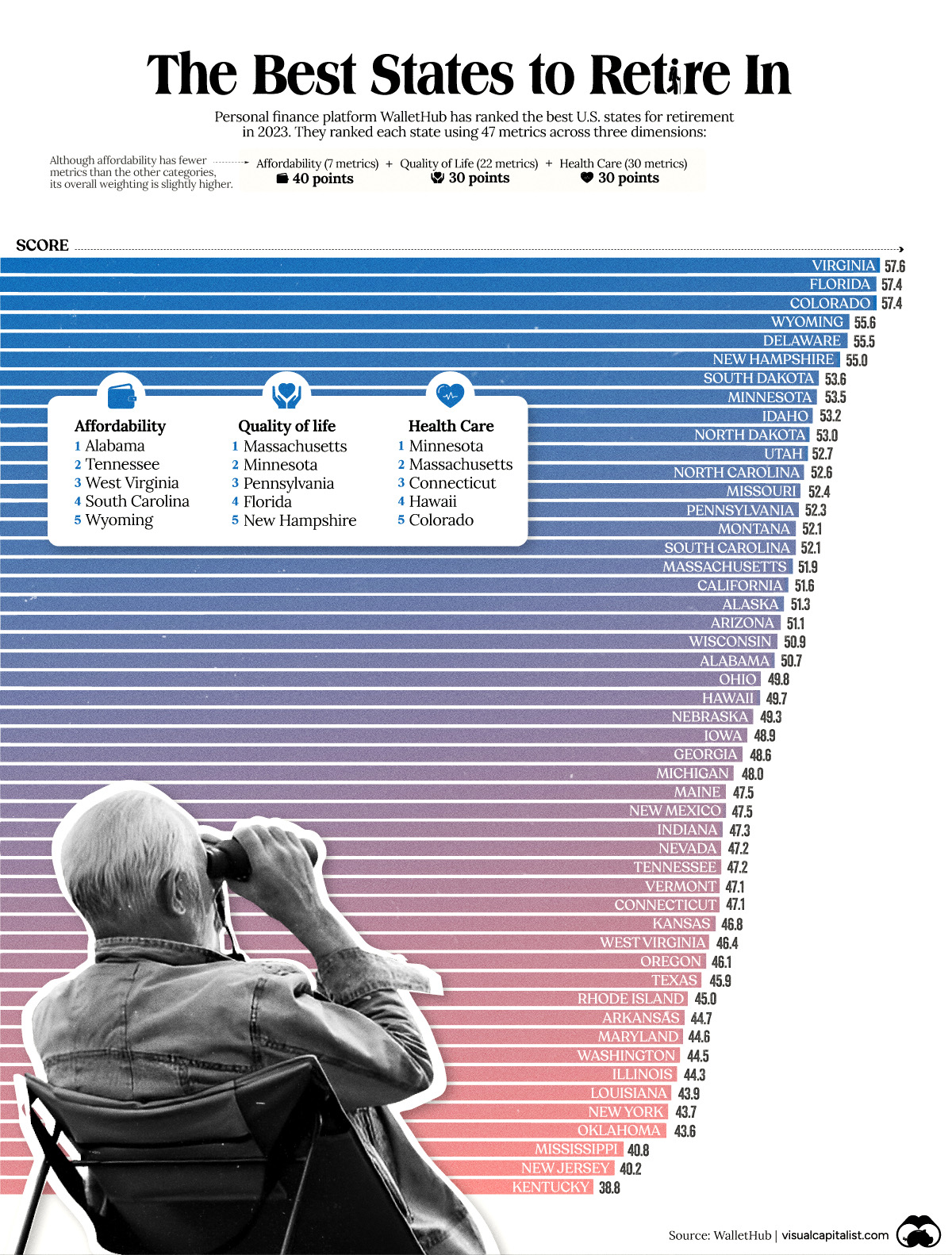

Have you ever thought about where the best place is to retire? Being strategic about location can make a big impact on your quality of life, and perhaps help your savings go just a bit further so, to help break it down, we’ve visualized data from personal finance platform, WalletHub, which ranked the best U.S. states for retirement as of 2023.

WalletHub ranked each state using 47 metrics across three dimensions.

- Affordability (7 metrics worth 40 points)

- Quality of Life (22 metrics worth 30 points)

- Health Care (18 metrics worth 30 points)

Here are some examples of what each dimension measures:

- Affordability: Cost of living and taxation

- Quality of Life: Quality of elder-abuse protections and crime rates

- Health Care: Number of health professionals per capita and life expectancy

According to this methodology, Virginia is currently the best state for retirement. Although the Southeastern state does not excel in any one dimension, it scores consistently well across all three to create a very balanced retirement profile. This gives it a slight advantage over second place Florida, which excels in quality of life and affordability, but falls further behind in terms of health care. Third-placed Colorado is a mirror of Florida, offering excellent health care but a lower quality of life in comparison.

Visit the source for the full list of metrics.

The final scores (visualized as the bars in the infographic below) represent each state’s weighted average across all metrics.

See below for more comprehensive results on the 10 best retirement states: