Who is going to pull the global economy out of its funk? No one knows,  but it’s not going to be China – regardless of how many more times the central bank is going to tweak its policies and cut interest rates. That’s what China’s trade fiasco is saying.

but it’s not going to be China – regardless of how many more times the central bank is going to tweak its policies and cut interest rates. That’s what China’s trade fiasco is saying.

Soothsayers…[are] shocked…by just how far China’s imports and exports have deteriorated.

Exports dropped 6.9% in October from a year ago, to $192.41 billion, after a 3.7% drop in September, the fourth month in a row of year-over-year declines. Exports had peaked last December at $227.5 billion and have since dropped 15.4%.

Shipments to the U.S. edged down 0.9% year-over-year, to the EU 2.9%, and to Japan…[by] 7.7%. Is China’s economy getting the feverishly hoped-for boost from supplying the overseas holiday shopping season? Not yet.

China has been getting hit by two simultaneous forces:

- weak global demand and

- loss of competitiveness due to rising wages, land costs, and other expenses. It’s no longer the low-cost producer and, as it switches to robots for manufacturing, which it is doing at lightning speed, it has to confront a new reality: robots are the great equalizer; unlike labor, they cost the same everywhere.

Imports plunged 18.8% year-over-year to $130.8 billion, after a 20.4% cliff-dive in September, the 12th month in a row of declines. This isn’t weak global demand, but a swoon in demand in China. Part of the plunge is due to falling commodity prices and weak demand for commodities in China but even then: for the first three quarters of the year, import volume, which eliminates prices as a factor, was down 4%. Imports peaked in Mark 2013 at $183.1 billion and are now down 28.6%.

The dismal import picture is a sign that China’s economy is weakening, including in key sectors like the property sector that the government has been trying to reflate. No one can get a real handle on how weak the economy really is, perhaps not even the government but it wants the rest of the world to believe that the economy grew at a phenomenal 6.9% in the third quarter.

With imports plunging much faster than exports, China’s trade surplus rose to $61.64 billion, on track for a record year. For all sides concerned, that’s the worst possible way of growing a trade surplus.

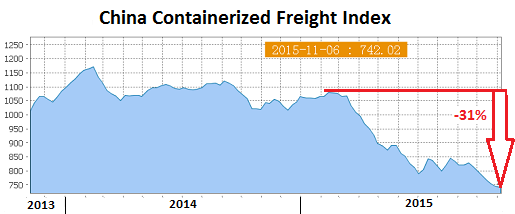

The China Containerized Freight Index At Record Low

The weakness in China’s economy and its exports to the rest of the world are showing up in the weekly China Containerized Freight Index: On Friday, it dropped to the worst level ever.

The index, operated by the Shanghai Shipping Exchange, tracks how much it costs, based on contractual and spot-market rates, to ship containers from China to 14 major destinations around the world. Unlike a lot of official data from China, the index is an unvarnished reflection of a relentless reality.

It has been cascading lower since February and has since dropped 31%. At 742 currently, it’s down 26% from its inception in 1998 when it was set at 1,000. This is what the collapse in shipping rates looks like:

The Shanghai Containerized Freight Index Has Plunged

The more volatile and immediate Shanghai Containerized Freight Index, which tracks only spot-market rates (not contractual rates) of shipping containers from Shanghai to 15 major destinations around the world, had surged over the two prior weeks from record lows. The spot rates it captures are seen as a harbinger of contractual rates, and that surge had given rise to hopes that the worst might be over but, last week, it re-plunged 15.6% to 641. Rates to the U.S. West Coast plummeted 19.1%, to the US East Coast 14.4%, and to Europe 31.8%…

Oversupply of Shipping Capacity

These shipping rates are a function not only of anemic demand from around the world for Chinese merchandise but also of oversupply of shipping capacity. “Overcapacity” is deadly for business. It has been hounding the commodities sectors as well, along with much of the industrial economy in China.

An outgrowth of cheap credit, mal-investment, and central-bank-infused over-optimism about future growth, the process of creating overcapacity heats up the economy, but it then represses prices and becomes a deflationary force that mauls businesses.

This process has trapped the container shipping industry that has invested billions of dollars every year to expand its fleet and add mega-container ships, without seeing the growth in global trade needed to support that expansion.

Maersk Line’s (the largest carrier in the world) shipping volume…rose a scant 1.1% in the third quarter…CEO Nils Smedegaard Andersen told Bloomberg recently that:

- “We believe that global growth is slowing down,” and is worse than forecast by the IMF and others, as trade is “significantly weaker than it normally would be under the growth forecasts we see.”

- The current slowdown “shouldn’t lead to an outright crisis. At this point in time, there are no grounds for seeing that happening.”

At this point in time. Very comforting…

[The original article* as written by Wolf Richter (wolfstreet.com), is presented above by the editorial team of munKNEE.com (Your Key to Making Money!) and the FREE Market Intelligence Report newsletter (see sample here – register here) in a slightly edited ([ ]) and abridged (…) format to provide a fast and easy read.]*http://wolfstreet.com/2015/11/09/china-trade-swoons-collapse-of-containerized-freight-index-hits-worst-level-ever-ccfi-scfi/