By Lance Roberts (This is an edited and abridged version by the Managing Editor of munKNEE.com – Your KEY To Making Money!)

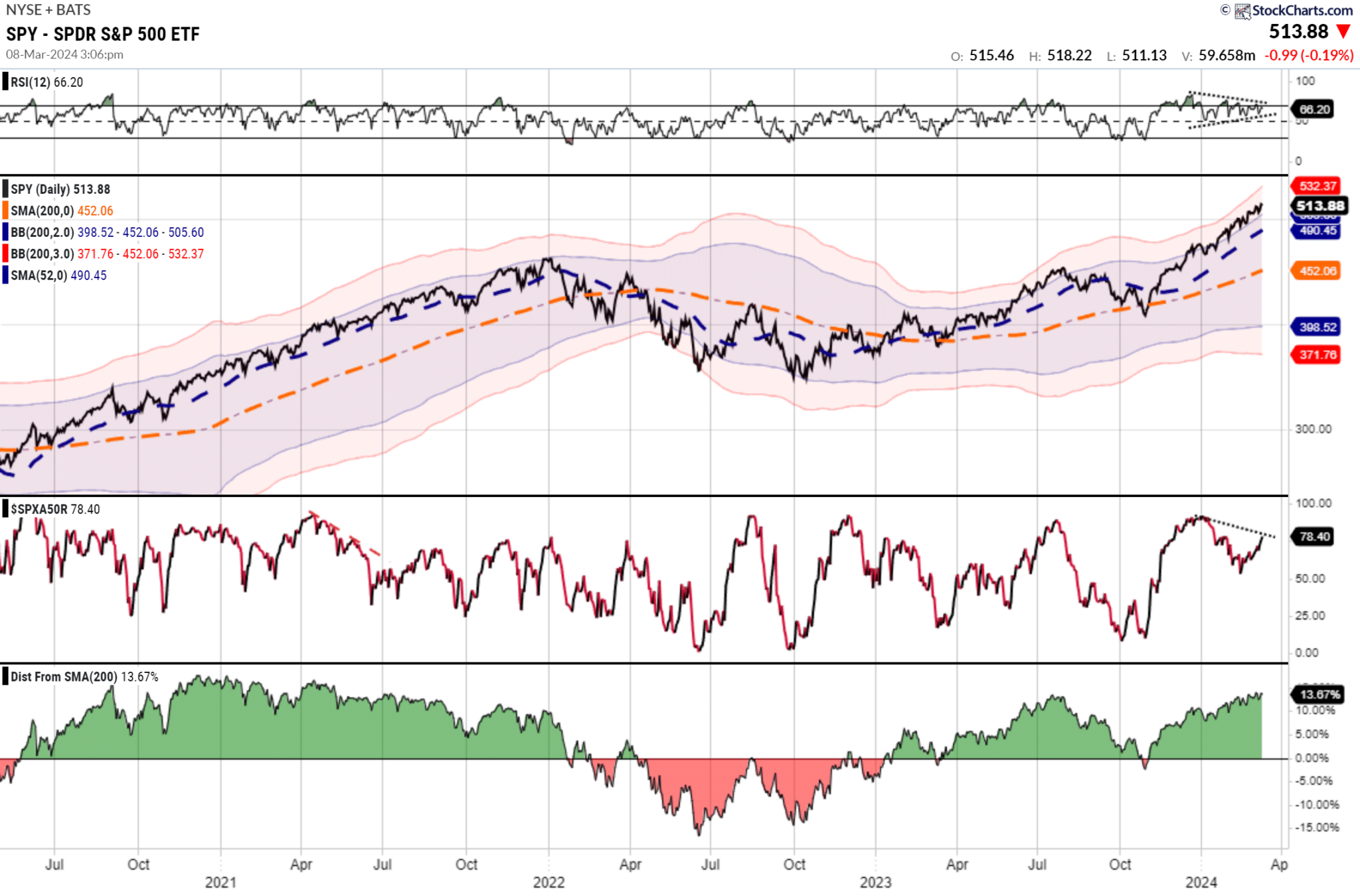

Last week, the ongoing “can’t stop, won’t stop” bullish trend remained firmly intact and that was the case again this week, as the market tested the 20-DMA, the bottom of the trend channel, early in the week, which sparked buyers to push the index to all-time highs by the week’s end. At the same time, volatility remains compressed, with the deviation from the 200-DMA growing. As shown, the breadth of the market and momentum are both negatively diverging from the rising market, which historically serves as a warning.

While we have become increasingly cautious over the last few weeks, as the market continues to rise, we have suggested taking profits and rebalancing portfolio risks. If you have not done so, such remains a recommended course of action. However, this does not mean to reduce equity allocations aggressively.

As noted, the market remains in a bullish trend. The 20-DMA, the bottom of the trend channel, will likely serve as an initial warning sign to reduce risk when it is violated. That level has repeatedly seen “buying programs” kick in and suggests that breaking that support will cause the algos to start selling. Such a switch in market dynamics would likely lead to a 5-10% correction over a few months. We will reduce equity positioning and aggressively implement hedging strategies at that point.

However, the question we have been asked most this week is, “Are we in a market bubble?” but, while we may not be in a full-fledged bubble yet, it doesn’t mean we aren’t on the way to that point. Investors are very exuberant, along with the media, and analysts are rapidly finding ways to justify excess valuations. In the near term, a market top is very likely.

- The market is currently up 17 of the past 19 weeks, the longest stretch since 1980.

- More importantly, the deviation of the market from the underlying 200-DMA is reaching rare extremes.

- Furthermore, the market trades 3 standard deviations above the 50-DMA concurrently with market momentum and breadth deteriorating. Historically, such a combination was a decent warning of a near-term market top.

- Critically, this rally has largely been a function of the most stimulative fiscal policy in the last 15 years. Notably, stimulative fiscal policy tends to reverse quickly from previous peaks. In other words, the supporting driver of the market rally since the October 2022 lows will likely end in 2024 for whatever reason. The reversal of that fiscal stimulus will coincide with a market top.

The above doesn’t mean a market top will occur next week. As John Maynard Keynes once said, “Markets can remain irrational longer than you can remain solvent“ and that is the problem with trying to “time” a market top, as they can last much longer than logic would predict.

Every bubble has two components:

- An underlying trend that prevails in reality and;

- A misconception relating to that trend;

and, In simplistic terms, once the bubble inflates, it will remain inflated until some unexpected, exogenous event causes a reversal in the underlying psychology from “exuberance” to “fear” – and what will cause that reversion in psychology no one knows. However, the important lesson is that market tops and bubbles are a function of “psychology.” The manifestation of that “psychology” manifests itself in asset prices and valuations.